Key Takeaways

- Private issuer Corporate default risks are expected to rise in every country due to powerful common macro factors: slower global growth and tight funding.

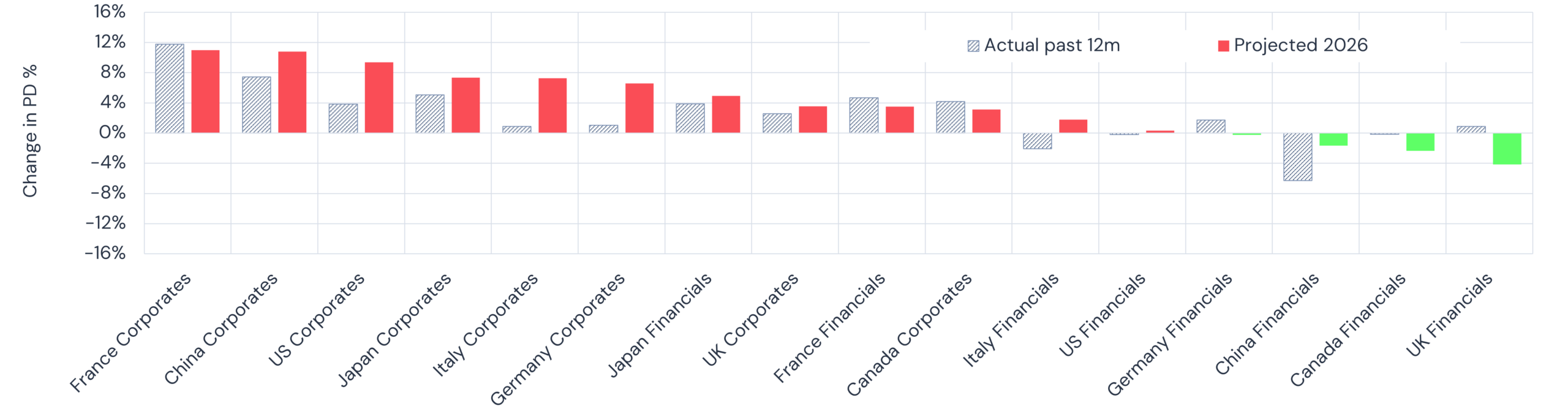

- France projected to show largest default rate increase of 11% with slow growth and structural challenges.

- China, US and Japan Private Corporates projected to rise 7% – 10% on slower growth.

- Italy and Germany to rise 7% (after a stable 2025).

- UK and Canada to show slight increase of 3% – 4%, both due to looser fiscal stance.

- Private Financials: Japan and France projected to rise 3.5%-5%. China, US, Canada and Germany expected to drop 0-2%. UK expected to drop 4%.

- Financials expected to again outperform Corporates overall.

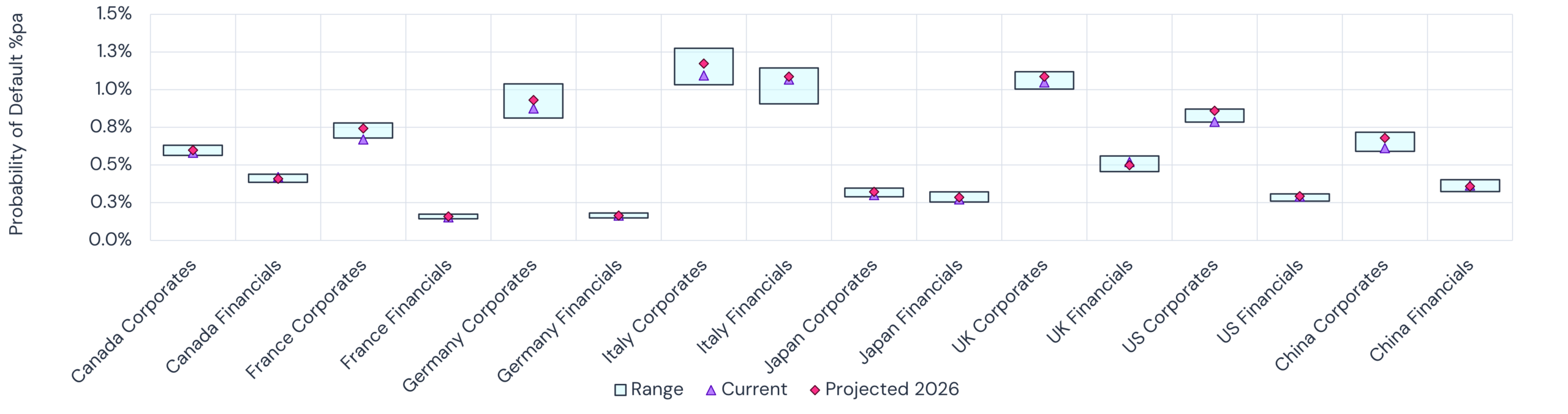

- Prediction ranges are highest for France, Germany and Italy Corporates plus Italy Financials.

- Prediction ranges generally much narrower for Financials vs. Corporates.

Table of Contents

Overview: G7 + China Macro and Default Risk Landscape

This report presents Credit Benchmark’s latest assessment of macroeconomic conditions and default risk across the G7 economies and China, using bank consensus credit data and forward-looking Probability of Default (PD) estimates for private corporates and financial institutions. By aggregating internal credit views from global banks, Credit Benchmark data provides risk practitioners with an early and consistent signal of changes in credit conditions across regions and sectors.

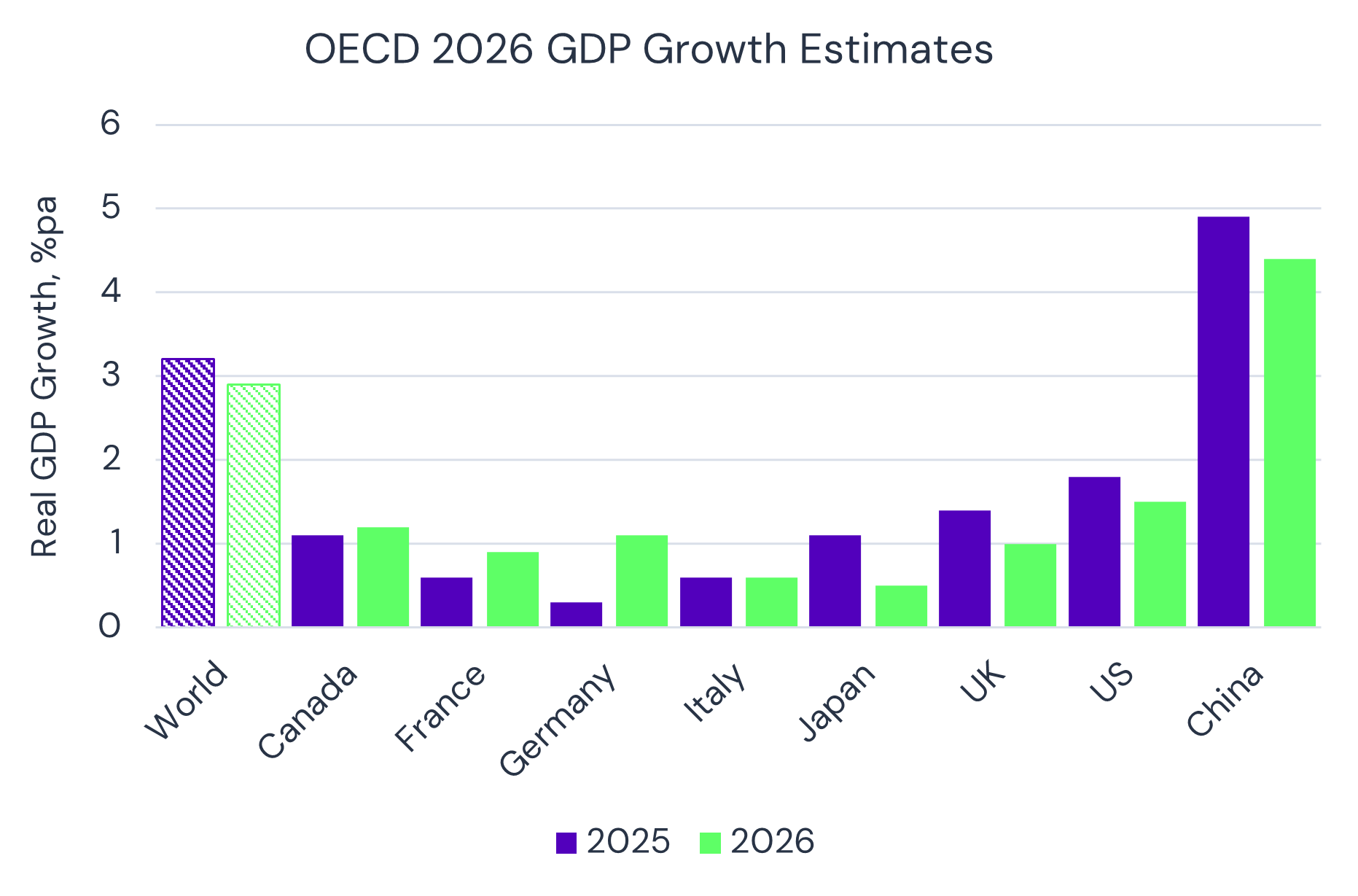

Against this backdrop, the IMF warn of slower global growth in 2026 due to rising protectionism and “fragmentation”. They cite erosion of institutional independence as likely to lead to inflationary policy decisions, with the risk of a financial shock from a Tech-led equity correction. The OECD increased their global GDP growth estimate for 2025 from 2.9% to 3.2% (2024 posted 3.3%); but they continue to expect a modest slowdown to 2.9% in 2026.

The OECD expect some recovery in Germany but continued sluggish growth overall. They expect material slowdowns in US, UK, China and Japan but modest recovery in Canada.

Macro drivers:

- Geopolitics: US actions in Venezuela set a possible precedent for other countries, especially China and Russia. Europe looks increasingly isolated as it seeks to defend its resource rich territories at the same time as it is ramping up defence of its eastern borders. Continued volatility, with winners and losers, seems most likely but the chances of a spike in the global risk premium have increased in recent weeks.

- Debt: Sovereign debt piles continue to grow and attempts to push short rates down to reduce the interest component have been neutralised by long bond vigilantes – long bond yields continue to trend higher globally. For corporates this has been partly offset by credit spreads hitting 10-year lows.

- Trade: While tariffs were widely anticipated, the actual rollout and impact has been skewed to specific countries and sectors, with the main losers being producers and users of metals and timber as well as farmers (exports blocked), pharma companies (regulatory blocks), and retailers (margin shrinkage). SE Asia has also taken a material hit. There have been some positive and negative effects on trade balances and fiscal positions, but apart from increased inflation pressures (offset by lower energy prices) the main outcome is heightened uncertainty – with many investment plans on hold across the globe.

- Inflation: While the meteoric rise in the gold price suggests increased concerns about inflation, liquidity is tightening. Lower oil prices have taken a toll on Middle East finances (e.g. Saudi Arabia have scaled back the Neom project).

- Markets & Money: Equity markets have been more volatile but net positive for most of the year. But there are worrying straws in the wind – Tricolor, First Brands, plus regulator warnings – especially in Private Credit and Technology segments. But the US Technology industry remains bullish, and very low credit spreads provide cheap finance for multiple data centres the size of midtown Manhattan – enough to keep US construction firms in business for years.

- Default risk perspectives: Allianz Trade report a mild (single digit %) increase in insolvencies for G7 + China in 2025 YTD1 – they expect peak insolvencies in 2026 and a drop into 2027 S&P estimate that 2025 YTD Speculative Grade defaults are in line with the 5-year average and suggest that the global default rate shows signs of stabilization.

If 2025 has not yet brought a “cred-apocalypse”, what does 2026 hold? In this report, we project 2026 changes in bank consensus default risk estimates for private firms for the economies of the G7 + China. This builds on the October 2025 launch of the US Private Credit Risk Index (CRI); we look at trends for the equivalent universe of firms in Canada, China, Germany, France, Italy, UK and Japan.

1Outside of this group, insolvencies are spiking in Hong Kong, Singapore, South Korea, Australia, Brazil as well as in Italy and Switzerland.

2026 G7 + China Default Risk Forecast

2026 Projected Changes in 1-year Private Default^ Rates – G7 + China - by size of change

2026 Default Risk Projections and Ranges for Private Indices – G7 alphabetical + China

^ Default Risk is defined as an average of the index constituents’ Probability of Default (PD), projected one year forward. See Methodology section for more detail.

Default Outlook for US Private Corporates* & Financials

US corporate default risk edges higher on tariffs and deficits, while financials stabilize amid strong tech investment.

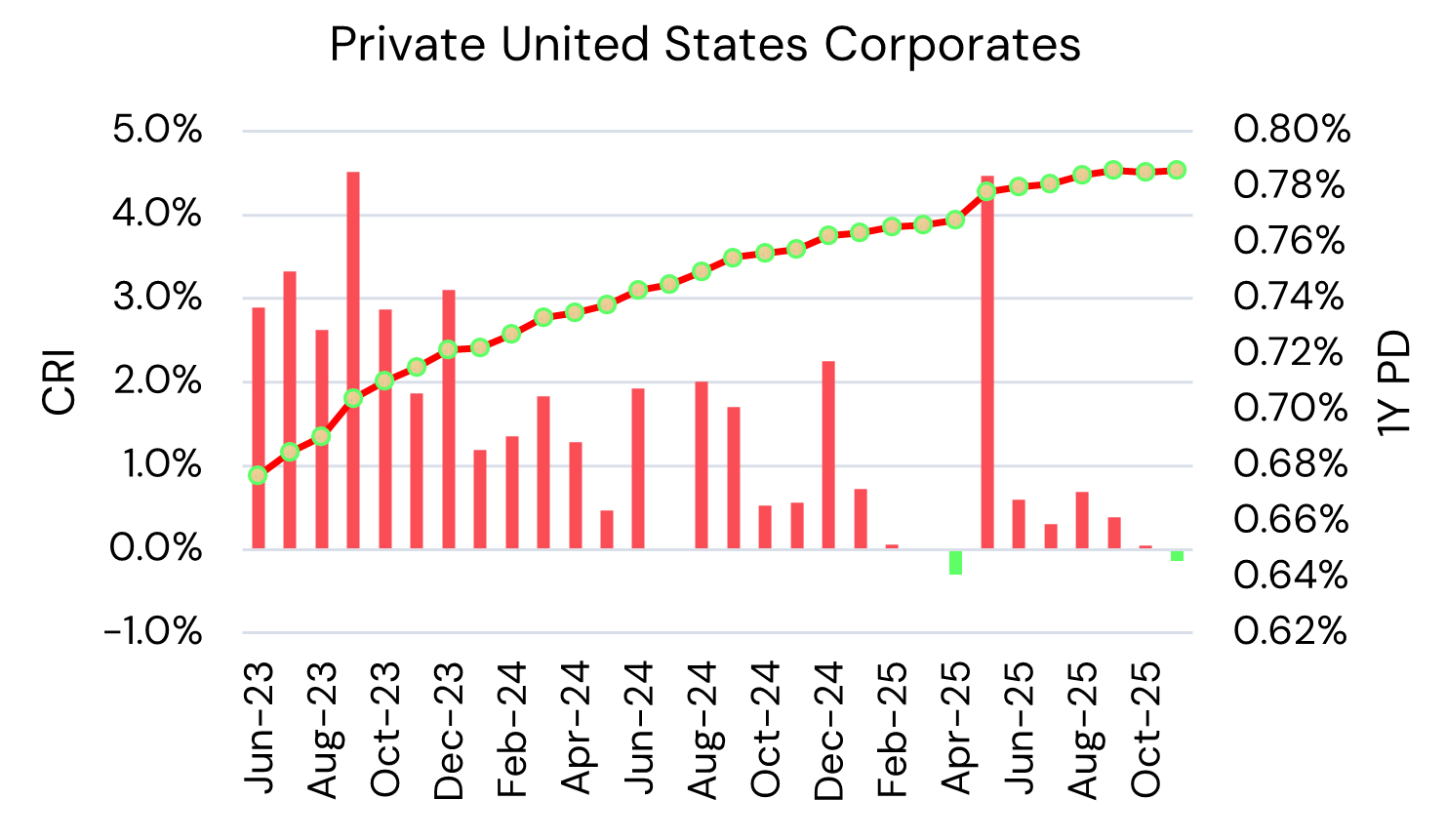

US Private Corporates – Credit Risk Index (CRI) and Probability of Default (PD)

US Private Corporates – PD Projections

US Private Financials – Credit Risk Index (CRI) and Probability of Default (PD)

US Private Financials – PD Projections

Key Takeaways:

- Private Probability of Default Now & Projected Q4 26:

- Corporates 0.86% from 0.79%

- Financials unchanged at 0.29%, but note wide range of estimates

- US Corporate downgrades and upgrades close to balance again after tariff-related spike in April – long term trend favours Improvement in H2 2026. Upgrades outpacing downgrades in Financials for past 6 months so PD likely to stabilize; but pace of rate cuts will determine scale of any improvement.

- Twin deficits are a growing challenge and projected benefits from tariffs are patchy. US Private Corporates have a relatively high % in ‘c’ category borrowers – and tariffs have damaged some sectors, especially metal Importers, timber users, and retailers. But major benefits for tech Infrastructure builders, and providers of materials / labour / finance for these developments.

* Covering all corporate sectors in Credit Benchmark’s Industry Schema but excluding financial institutions.

Default Outlook for Canada Private Corporates & Financials

Canadian default risks remain relatively contained, supported by fiscal flexibility and a recovering housing market.

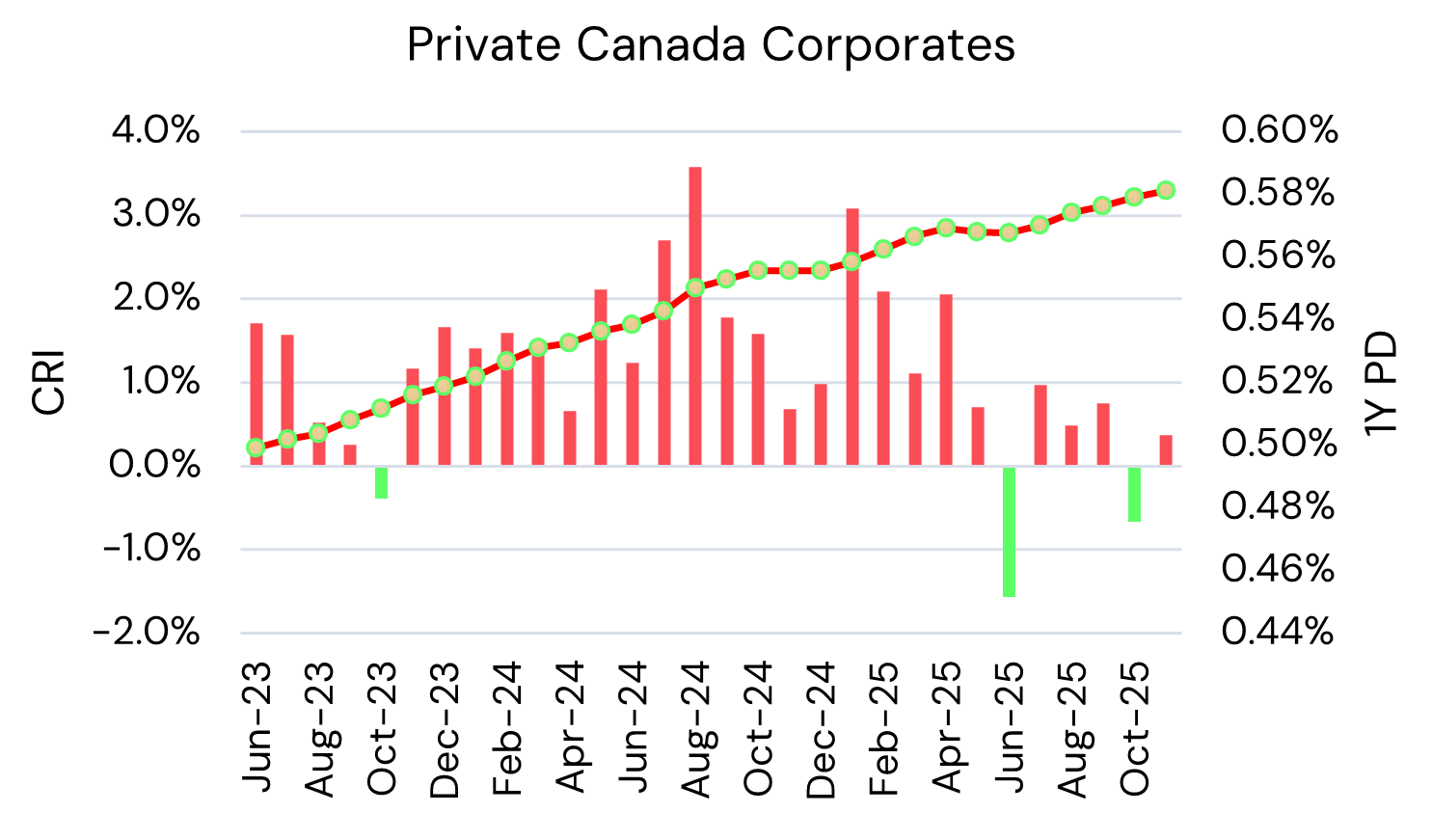

Canada Private Corporates – Credit Risk Index (CRI) and Probability of Default (PD)

Canada Private Corporates – PD Projections

Canada Private Financials – Credit Risk Index (CRI) and Probability of Default (PD)

Canada Private Financials – PD Projections

Key Takeaways:

- Private Probability of Default Now & Projected Q4 26:

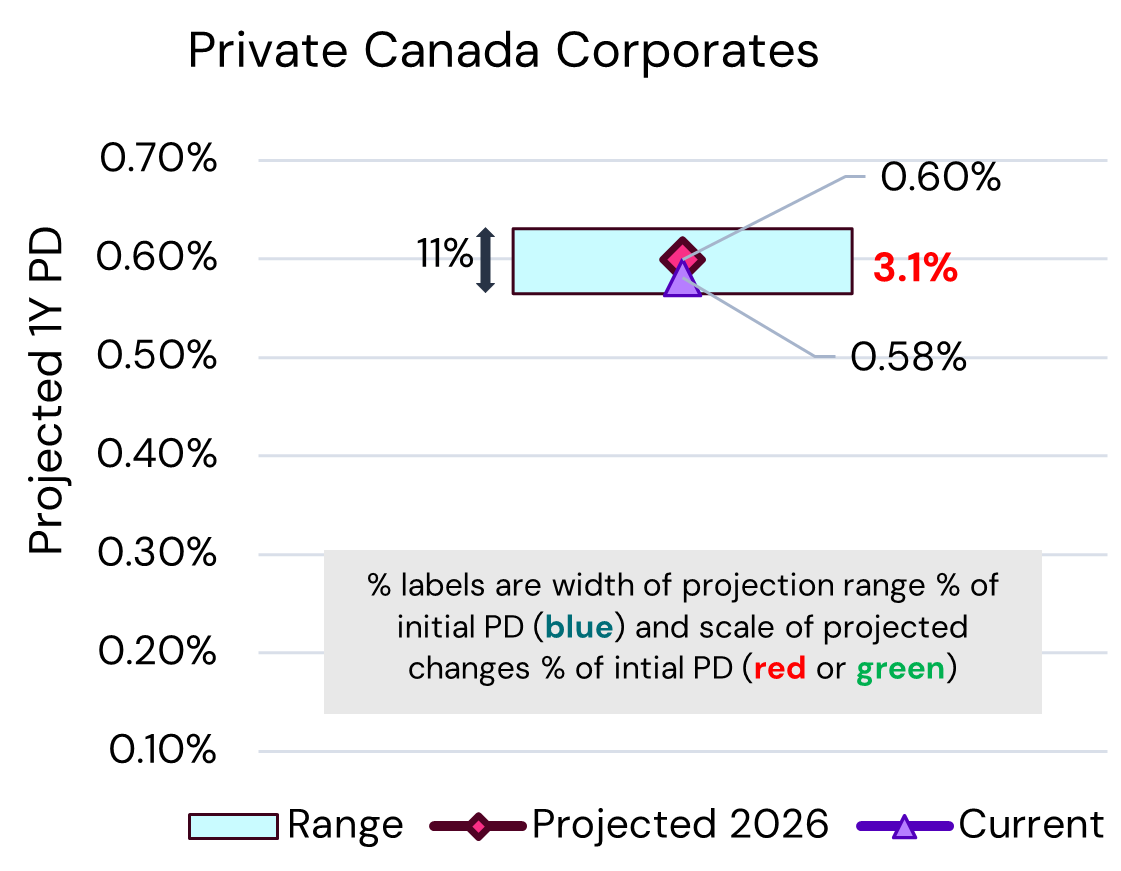

- Corporates 0.60% from 0.59%; estimate range of 11% (similar to US Corporates.)

- Financials 0.41% from 0.42%; but wide range or estimates (similar to US Financials.)

- Canada Private Corporate downgrades still outweigh upgrades but moving rapidly towards balance despite sluggish GDP growth – PDs could stabilize in H2 2026. Upgrades prevail in Financials In recent months and PD stable.

- Inflation on target and growth projected to recover, with some scope for fiscal loosening. Tariffs have been negative but manageable, Government is prioritising long term Investment and housing market is recovering. Some risk from further trade disputes and global commodity price weakness.

Default Outlook for Germany Private Corporates & Financials

Weak growth and trade fragmentation lift German corporate risk, partly offset by defence-led investment.

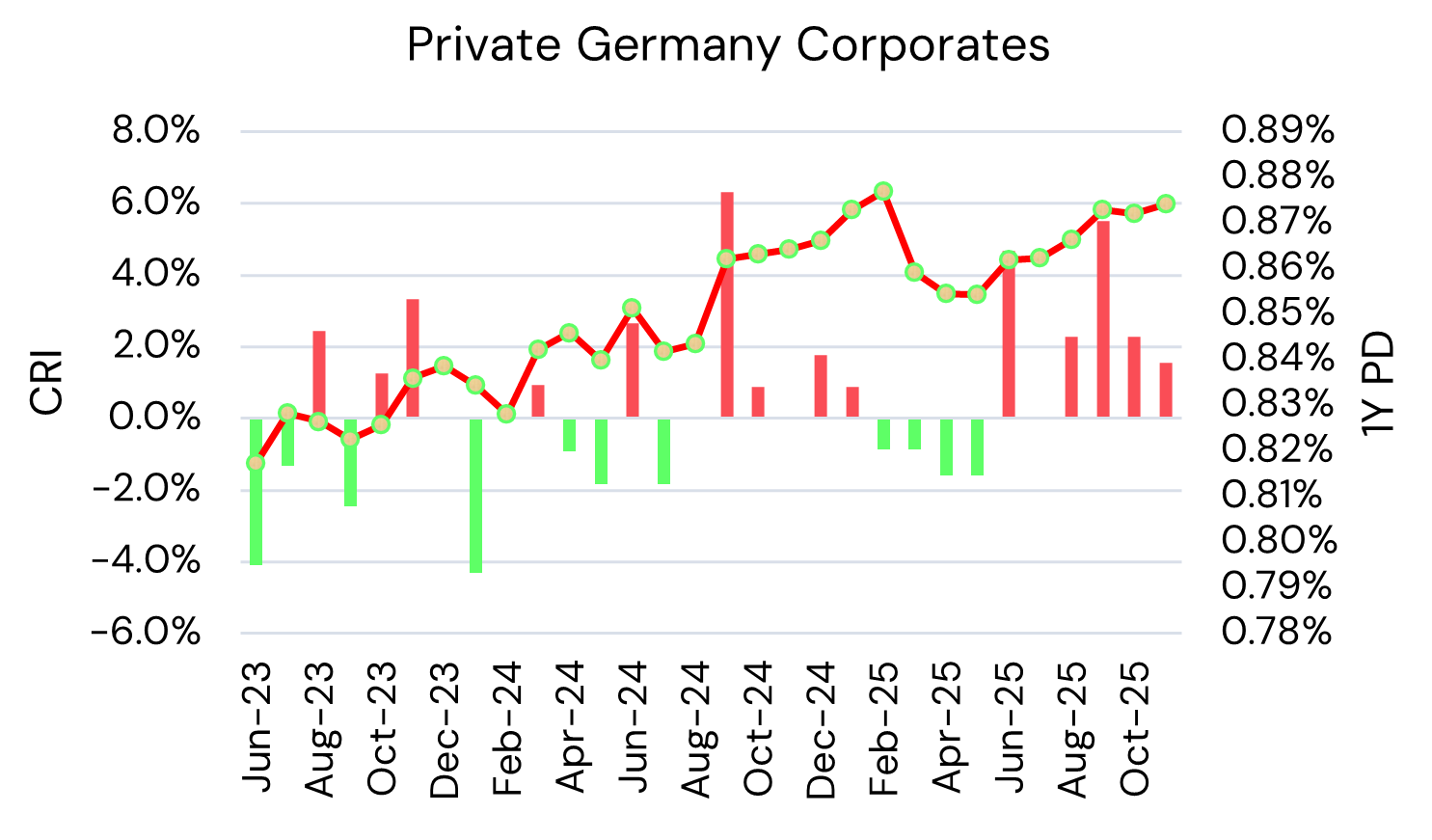

Germany Private Corporates – Credit Risk Index (CRI) and Probability of Default (PD)

Germany Private Corporates – PD Projections

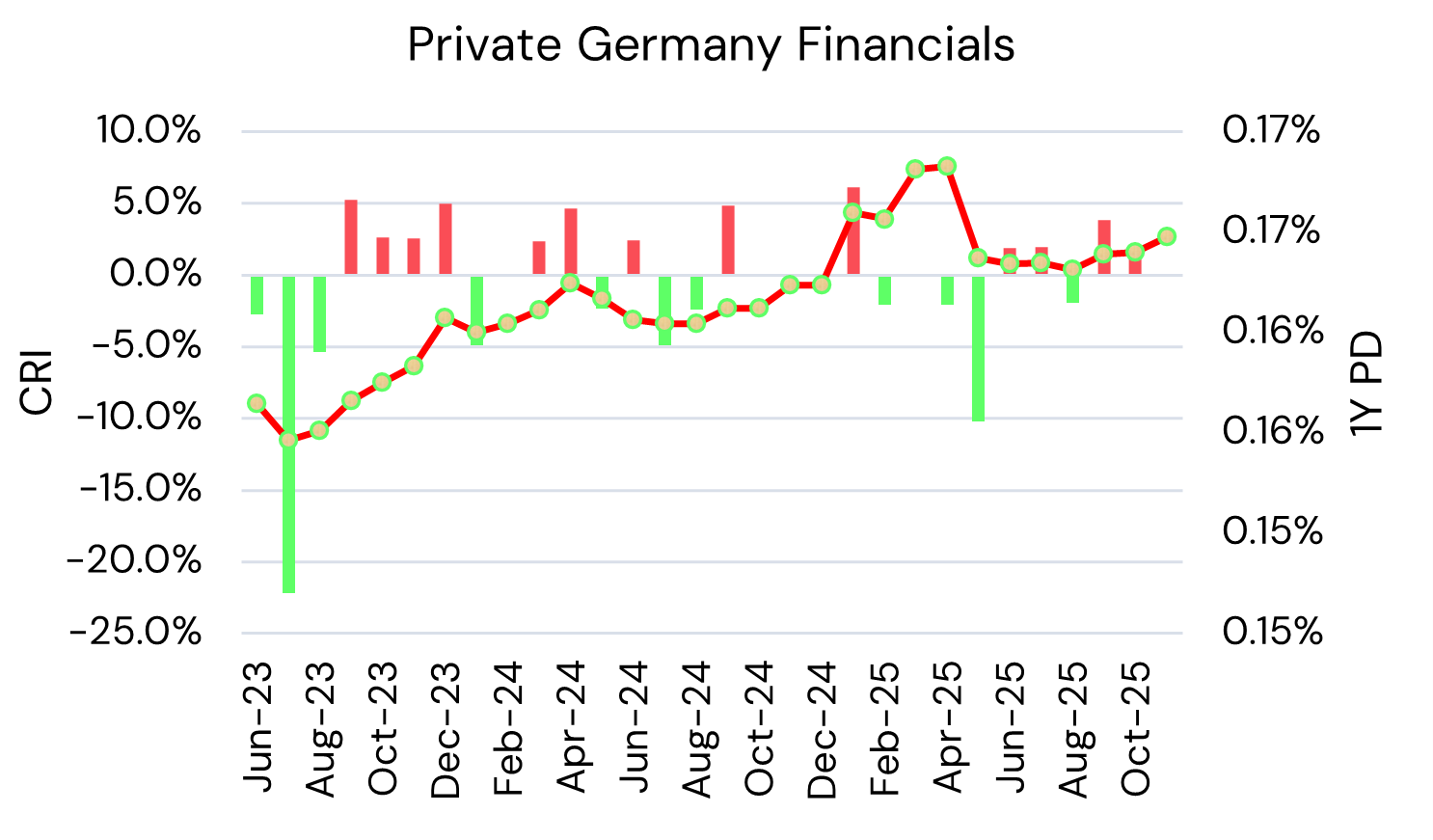

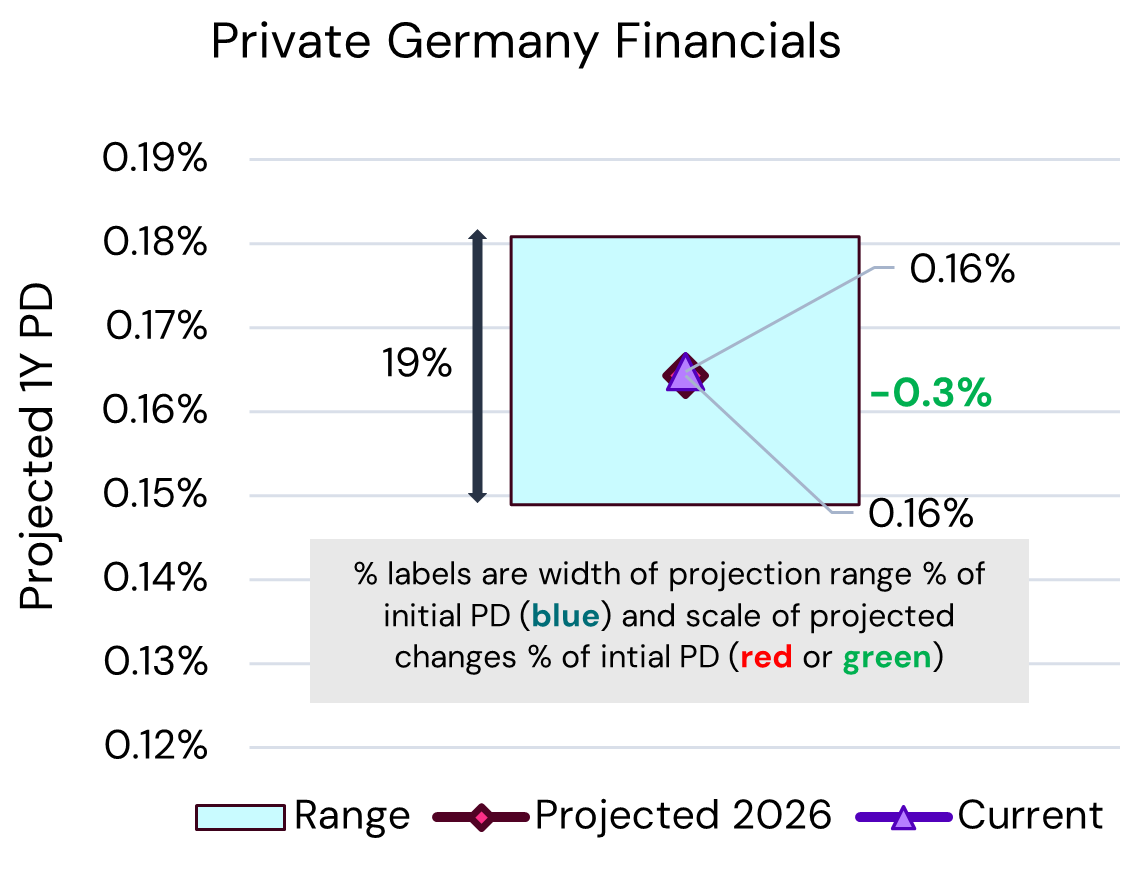

Germany Private Financials – Credit Risk Index (CRI) and Probability of Default (PD)

Germany Private Financials – PD Projections

Key Takeaways:

- Private Probability of Default Now & Projected Q4 26:

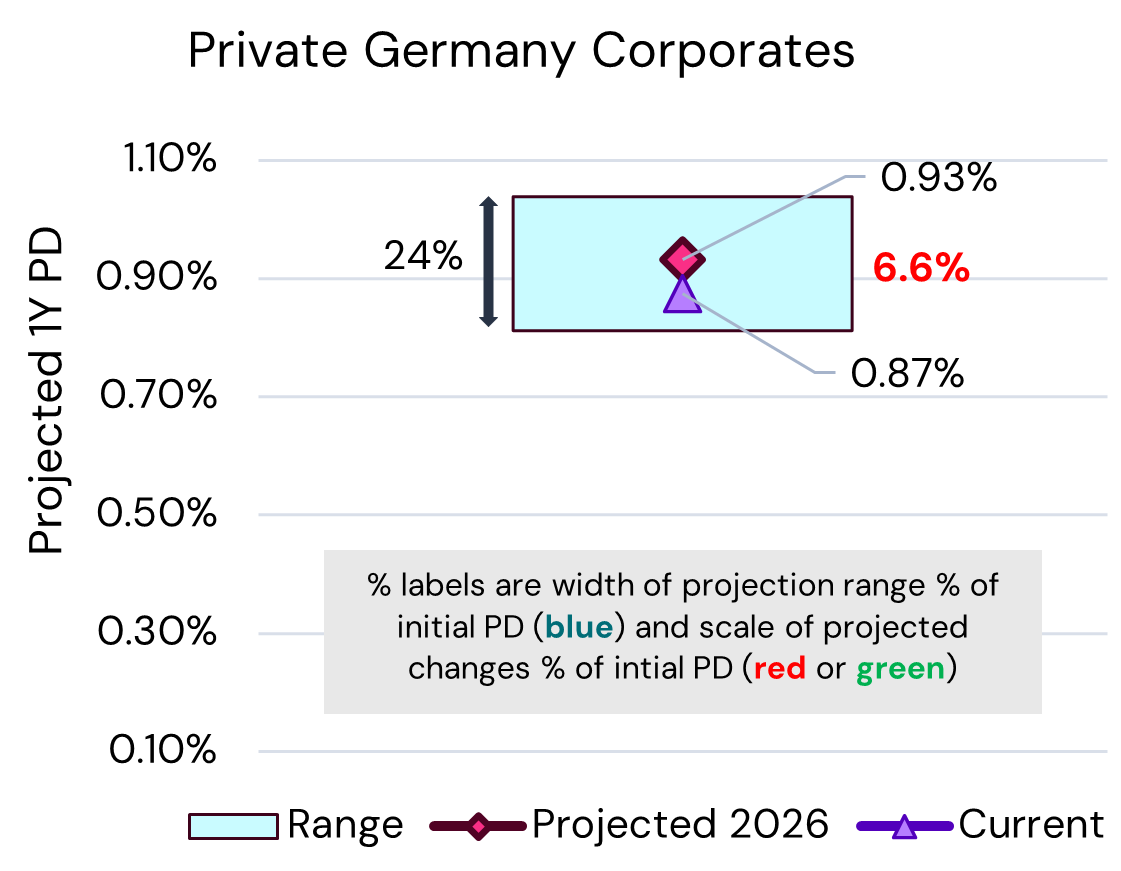

- Corporates 0.93% from 0.87%

- Financials unchanged at 0.16% but large +/-% range (on a low base.)

- Germany Private Corporate downgrades show an erratic rising trend vs upgrades, with a backdrop of weak GDP growth. Financials have been biased to positive in the last three years, but recent months show a possible deterioration.

- Inflation Is under control and the budget position is still one of the best in the G7 apart from Canada. But the large trade surplus could shrink if the global trade landscape continues to fragment. However, the urgent need for European military readiness is positive for German defence, engineering and software sectors.

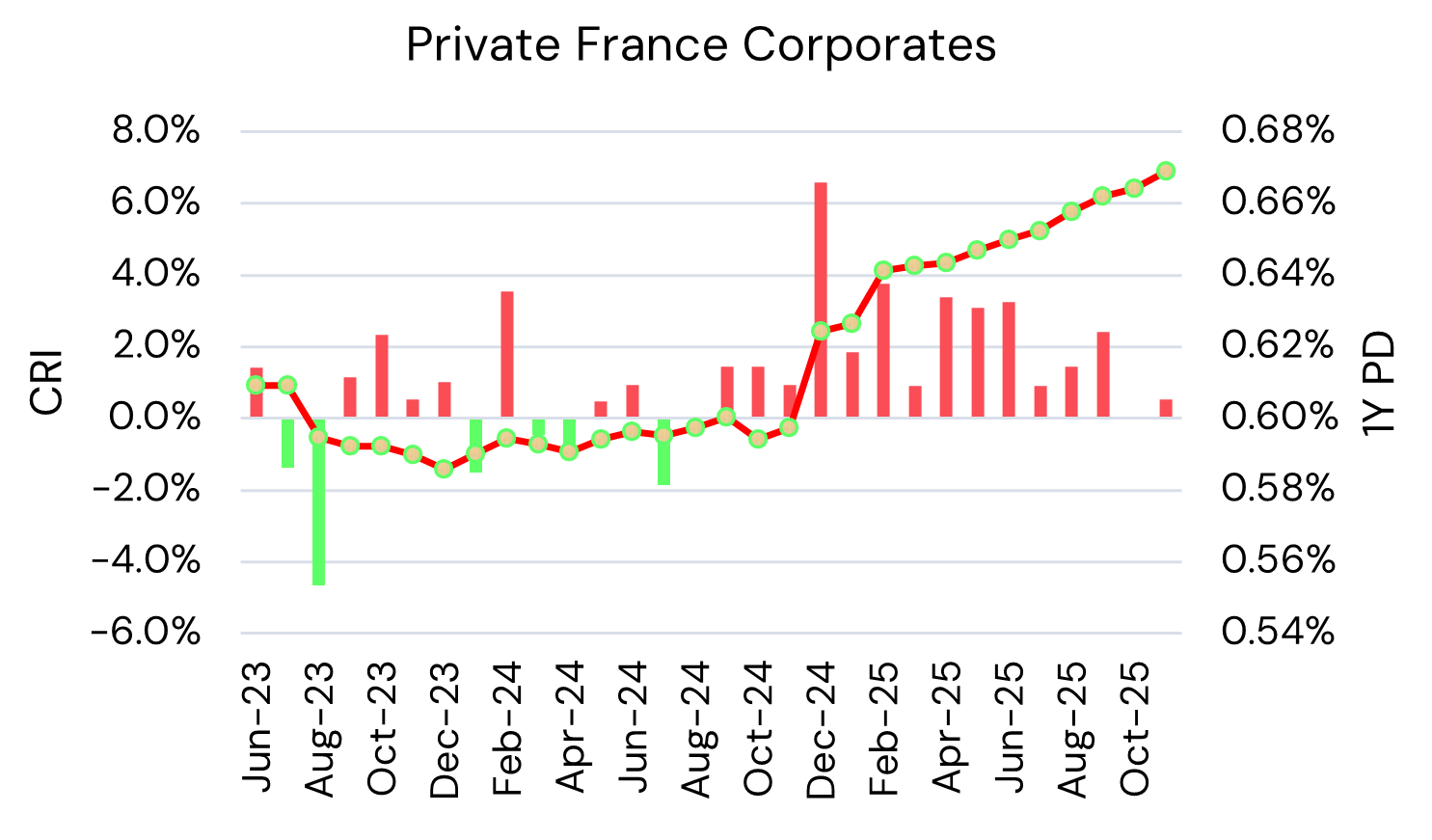

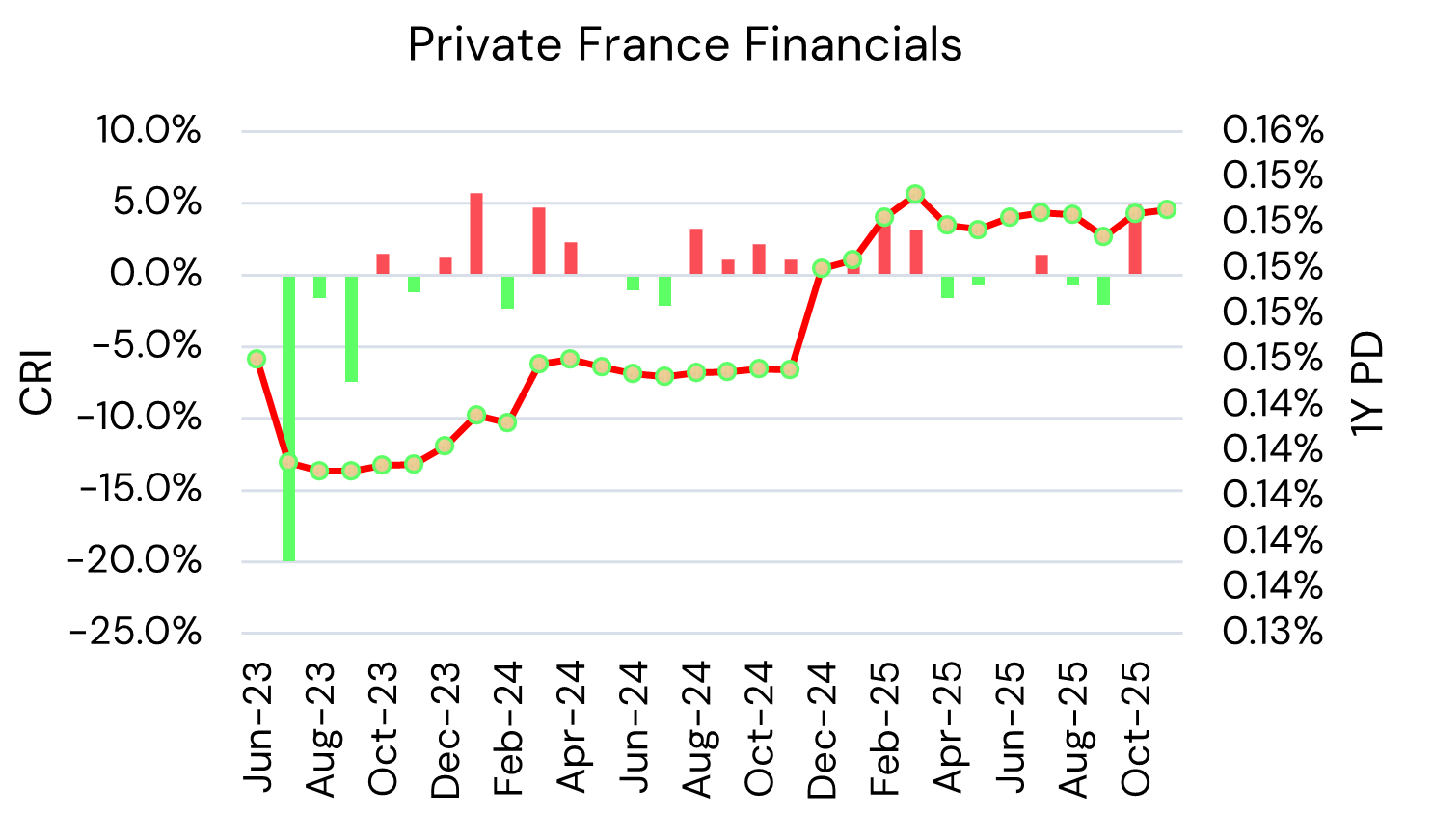

Default Outlook for France Private Corporates & Financials

France faces the sharpest rise in corporate default risk amid slow growth, high real yields and fiscal strain.

France Private Corporates – Credit Risk Index (CRI) and Probability of Default (PD)

France Private Corporates – PD Projections

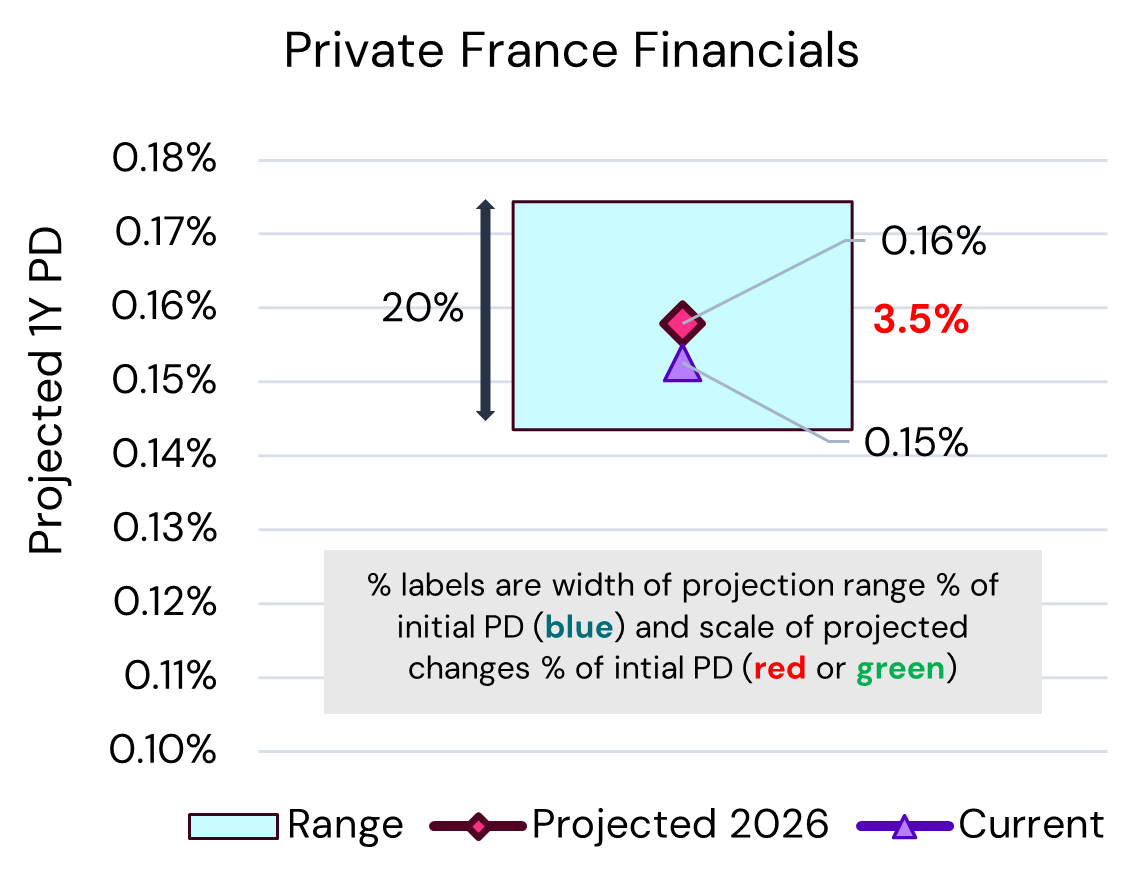

France Private Financials – Credit Risk Index (CRI) and Probability of Default (PD)

France Private Financials – PD Projections

Key Takeaways:

- Private Probability of Default Now & Projected Q4 26:

- Corporates 0.74% from 0.67%

- Financials 0.16% from 0.15%

- France Private Corporate downgrades have outnumbered upgrades for over a year; the pressure is easing but remains biased to deterioration; the PD trend is relentlessly up. Financials have shown slight signs of recent improvement, but the medium-term PD trend remains biased to higher risk.

- Inflation is low (although higher than Germany and Italy) but 10-year real yields are highest in the G7. The budget deficit is a major issue so real medium term funding costs will likely stay high.

Default Outlook for Italy Private Corporates & Financials

Italy shows rising but volatile default risks, with growth stagnation and funding costs posing medium-term headwinds.

Italy Private Corporates – Credit Risk Index (CRI) and Probability of Default (PD)

Italy Private Corporates – PD Projections

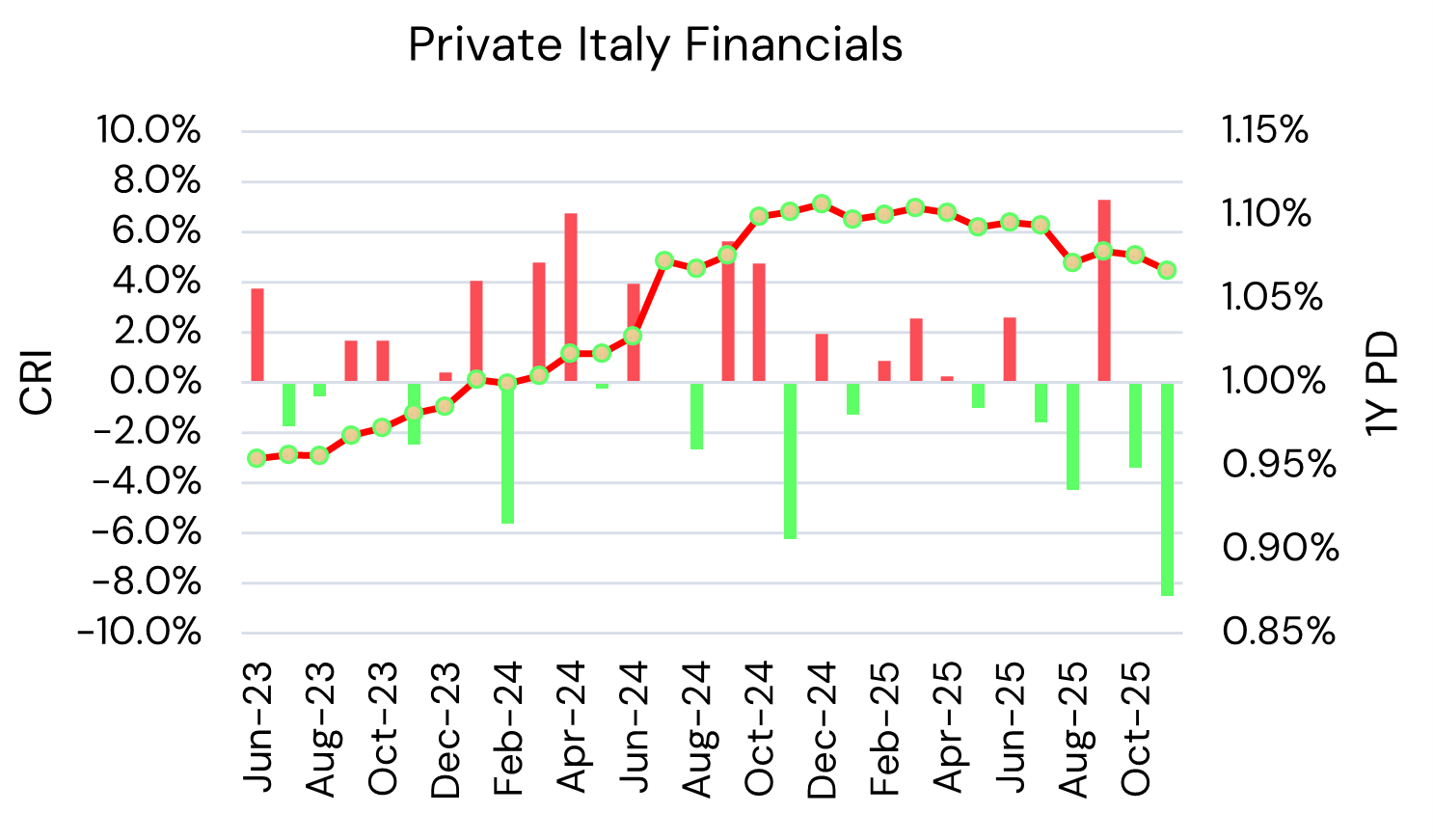

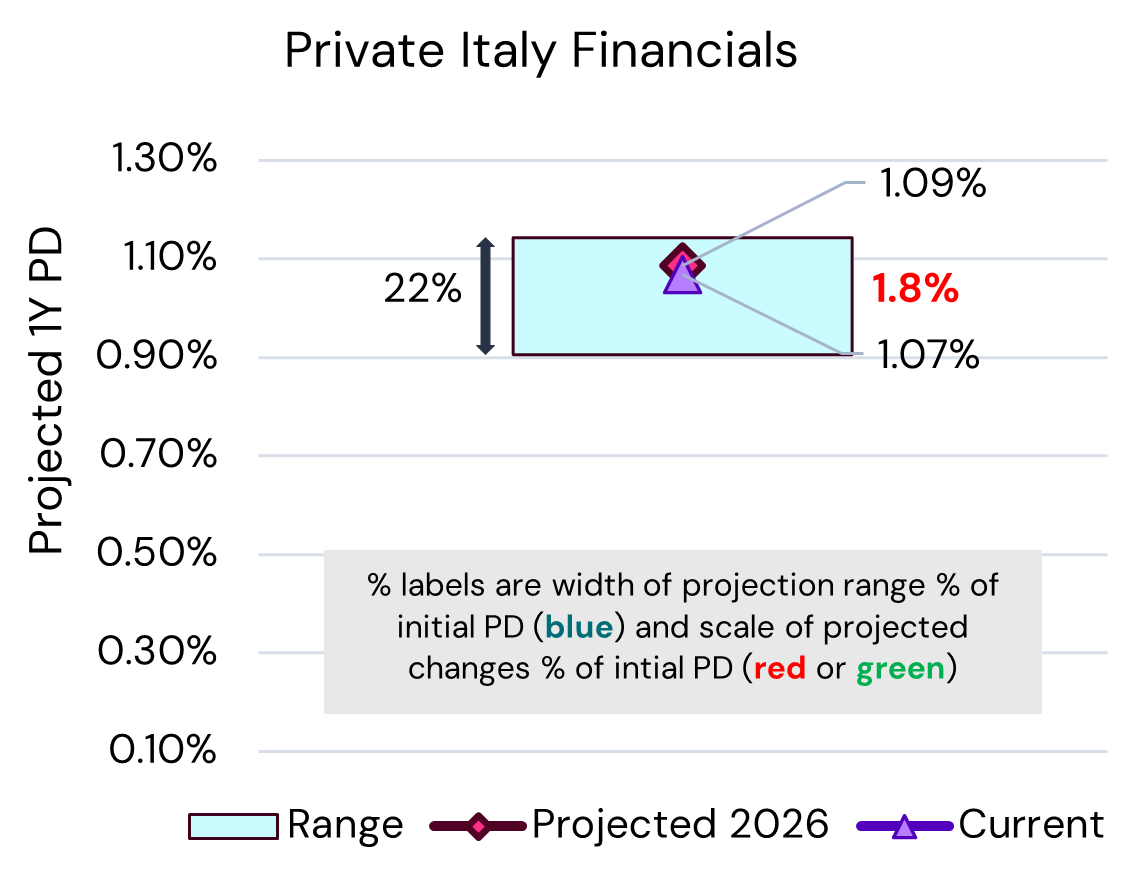

Italy Private Financials – Credit Risk Index (CRI) and Probability of Default (PD)

Italy Private Financials – PD Projections

Key Takeaways:

- Private Probability of Default Now & Projected Q4 26:

- Corporates 1.17% from 1.09%

- Financials 1.09% from 1.07%

- NB Both segments have large ranges vs. central projection – reflects volatile PDs and CRIs.

- Italy Private Corporates and Financials show a switch to upgrades outnumbering downgrades for 2 months, but both series are volatile. And as with the other EU G7 members, stagnant GDP growth is likely to increase Corporate default risk.

- Macro fundamentals are well behaved, but growth is likely to slow to German levels, and the new trade landscape is a challenge. Medium term real funding costs could be an increasing headwind.

Default Outlook for UK Private Corporates & Financials

UK corporate risks tick up modestly, while financials improve as fiscal clarity and investment sentiment strengthen.

UK Private Corporates – Credit Risk Index (CRI) and Probability of Default (PD)

UK Private Corporates – PD Projections

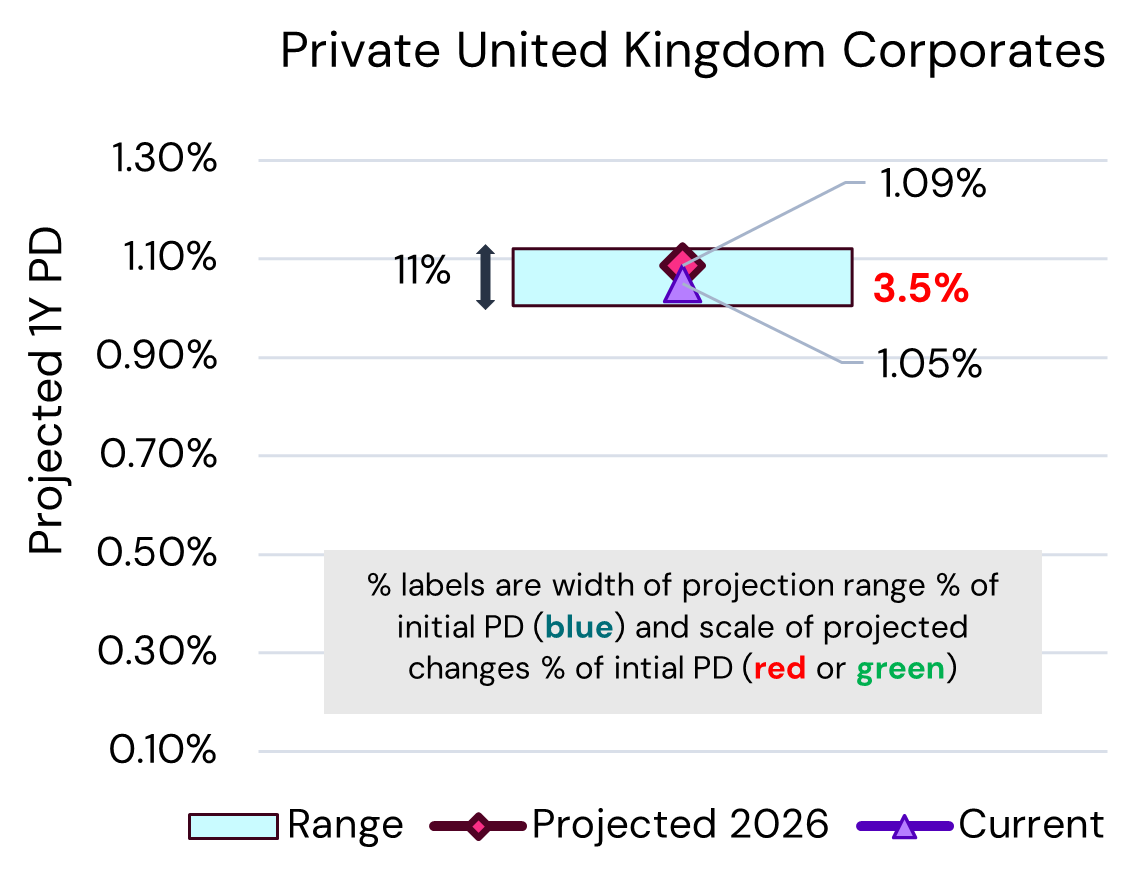

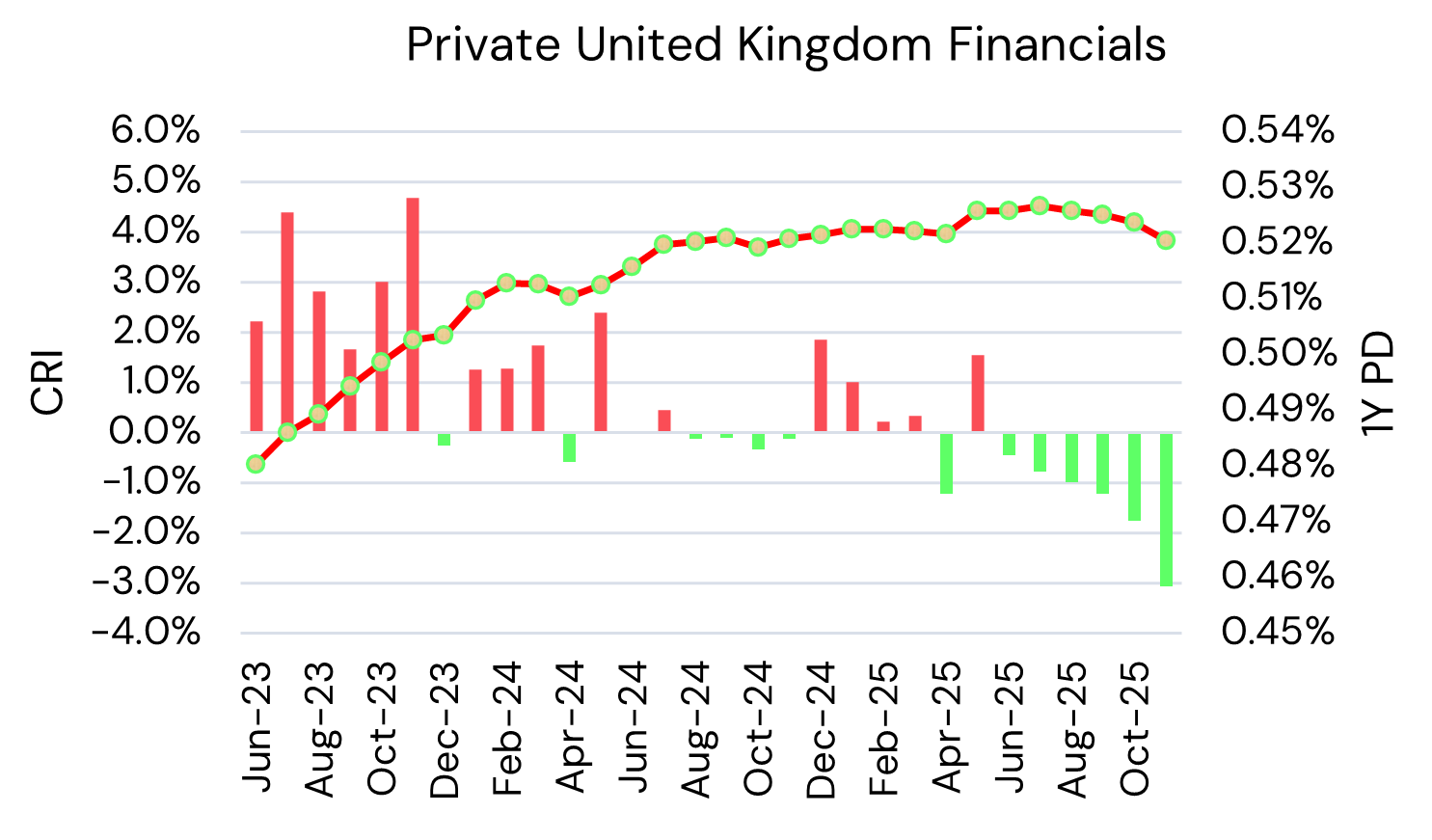

UK Private Financials – Credit Risk Index (CRI) and Probability of Default (PD)

UK Private Financials – PD Projections

Key Takeaways:

- Private Probability of Default Now & Projected Q4 26:

- Corporates 1.09% from 1.05% with a narrow prediction range

- Financials 0.50% from 0.52% (large range, but from a low base.)

- UK Private Corporate downgrades outnumber upgrades in over past 12 months, but volatile CRI favoured upgrades in past month. Financials have swung strongly towards improvements, and the PD is stabilizing with scope to drop.

- Macro fundamentals are mixed – twin deficits and above average inflation but growth is higher than EU. Tax rise impact is back-end loaded so net fiscal boost. Investment spending could climb as budget uncertainty recedes.

Default Outlook for Japan Private Corporates & Financials

Japan’s corporate default risk rises gradually on slowing growth and higher yields, with financials more resilient.

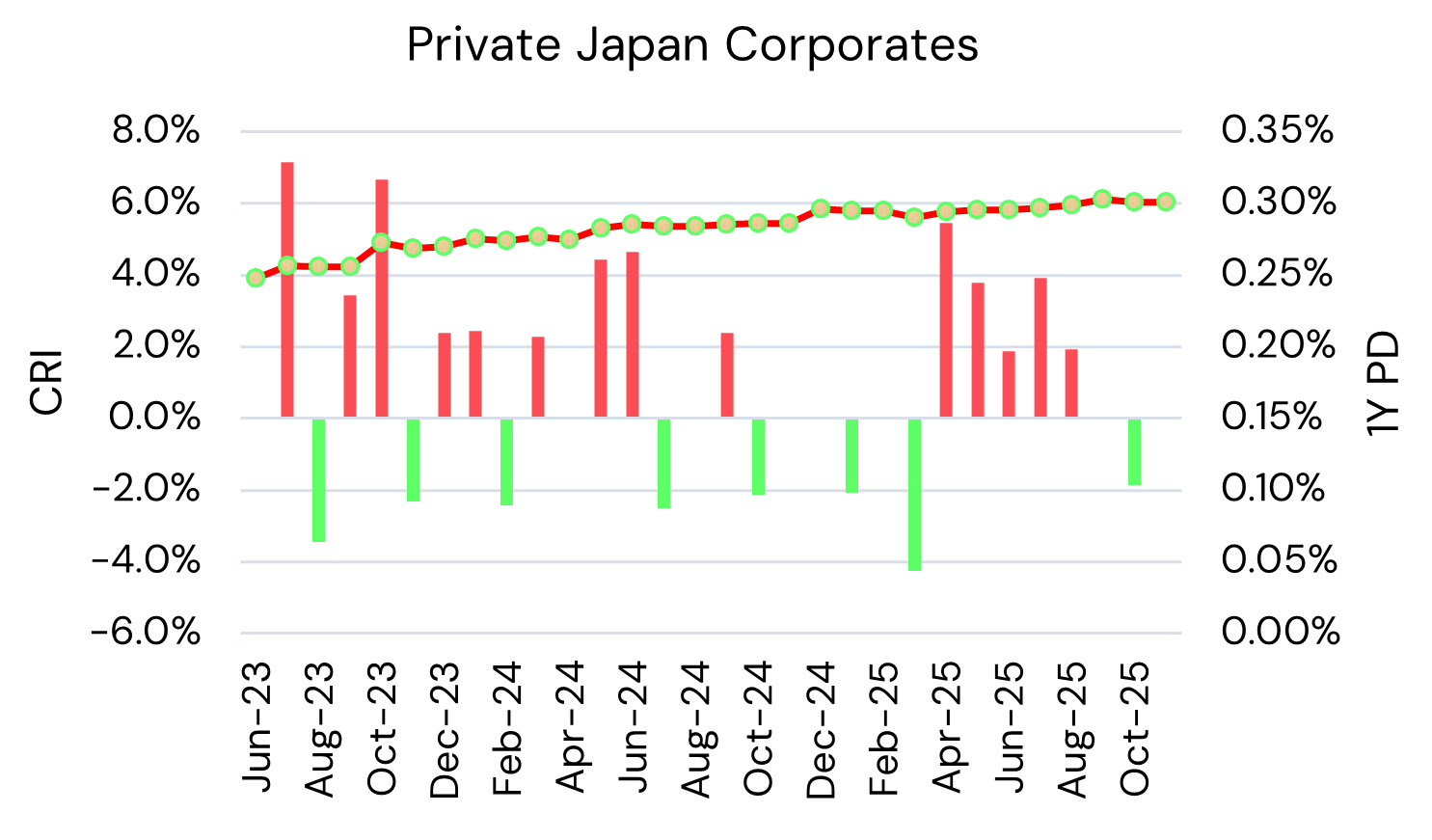

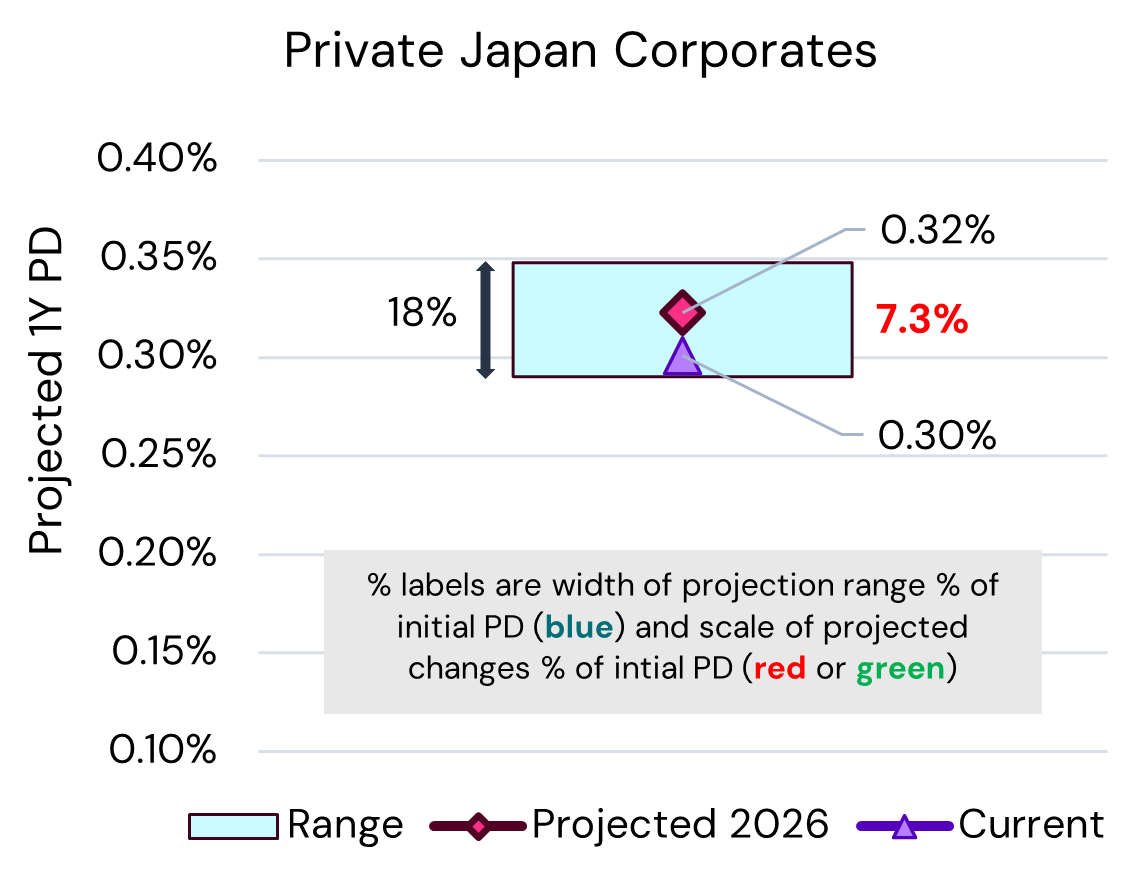

Japan Private Corporates – Credit Risk Index (CRI) and Probability of Default (PD)

Japan Private Corporates – PD Projections

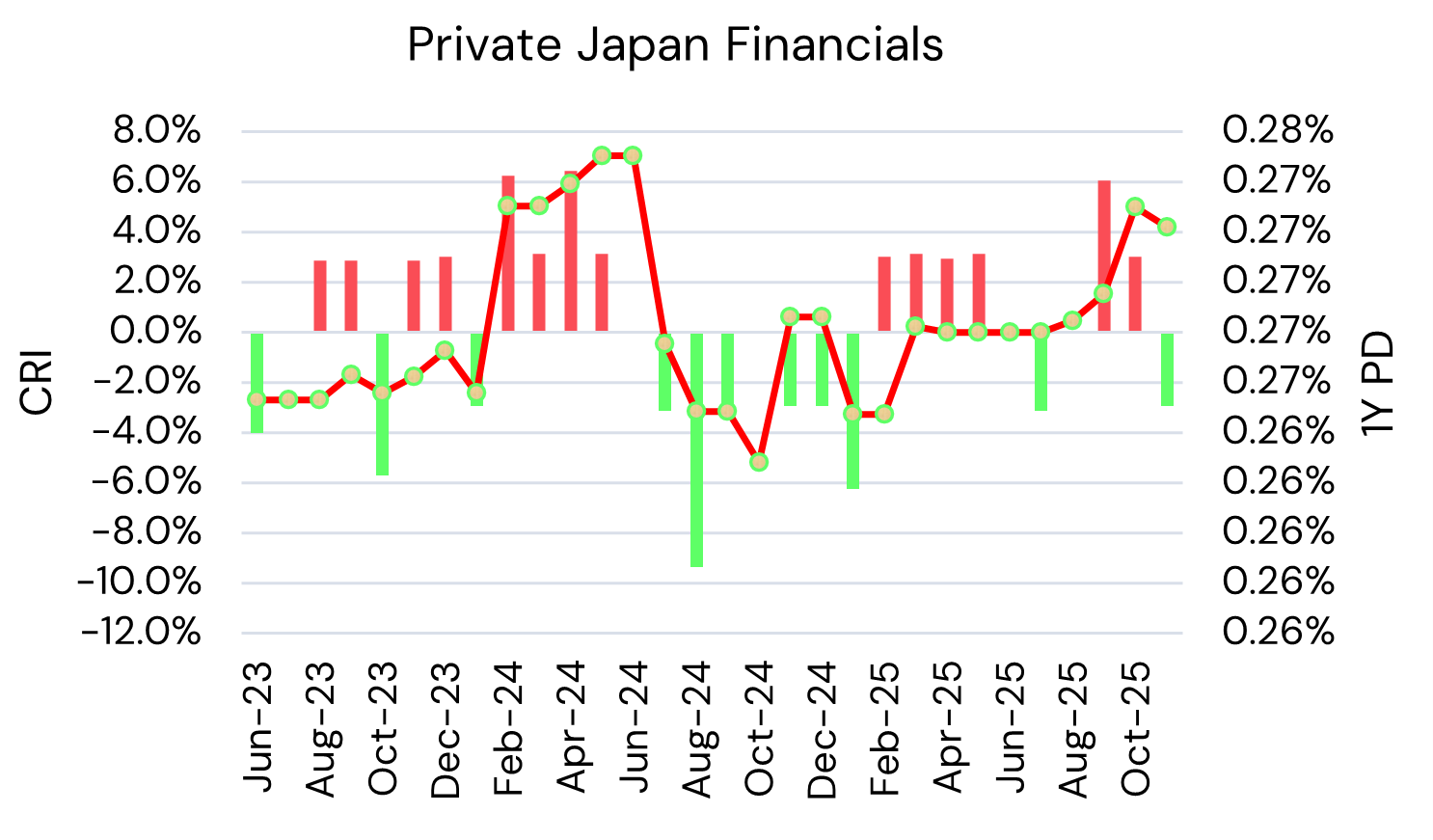

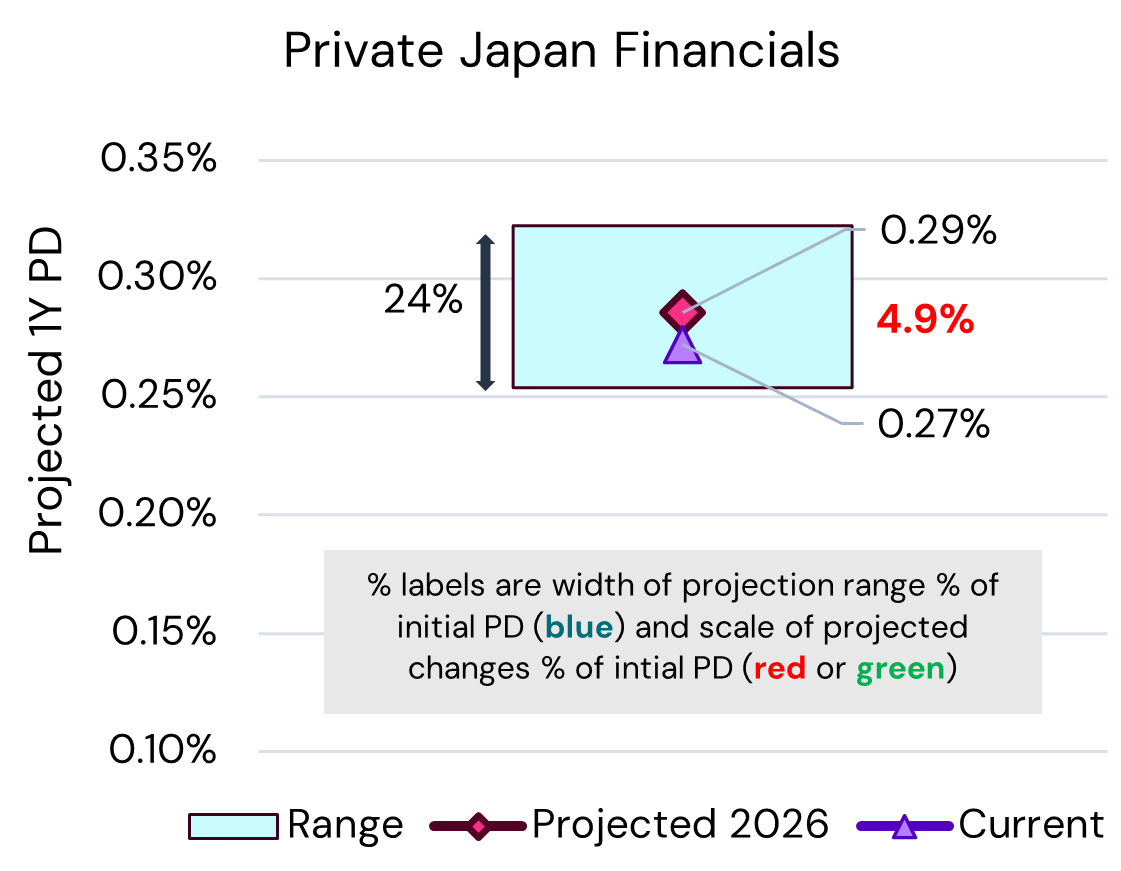

Japan Private Financials – Credit Risk Index (CRI) and Probability of Default (PD)

Japan Private Financials – PD Projections

Key Takeaways:

- Private Probability of Default Now & Projected Q4 26:

- Corporates 0.32% from 0.30%

- Financials 0.29% from 0.27% (as with most financials, large range on a low base.)

- Japan Corporates CRI biased to downgrades – likely to continue to climb on sharp growth slowdown and higher long bond yields. Wider estimation error due to low base PD.

- Japan Financials CRI very volatile. But limited projected increase in default rates.

- US tariff policy and relations with China are major unknowns – likely to hit Corporates more than Financials.

Default Outlook for China Private Corporates & Financials

China corporate default risk increases on weak growth and tariffs, while financials stabilize after property stress.

China Private Corporates – Credit Risk Index (CRI) and Probability of Default (PD)

China Private Corporates – PD Projections

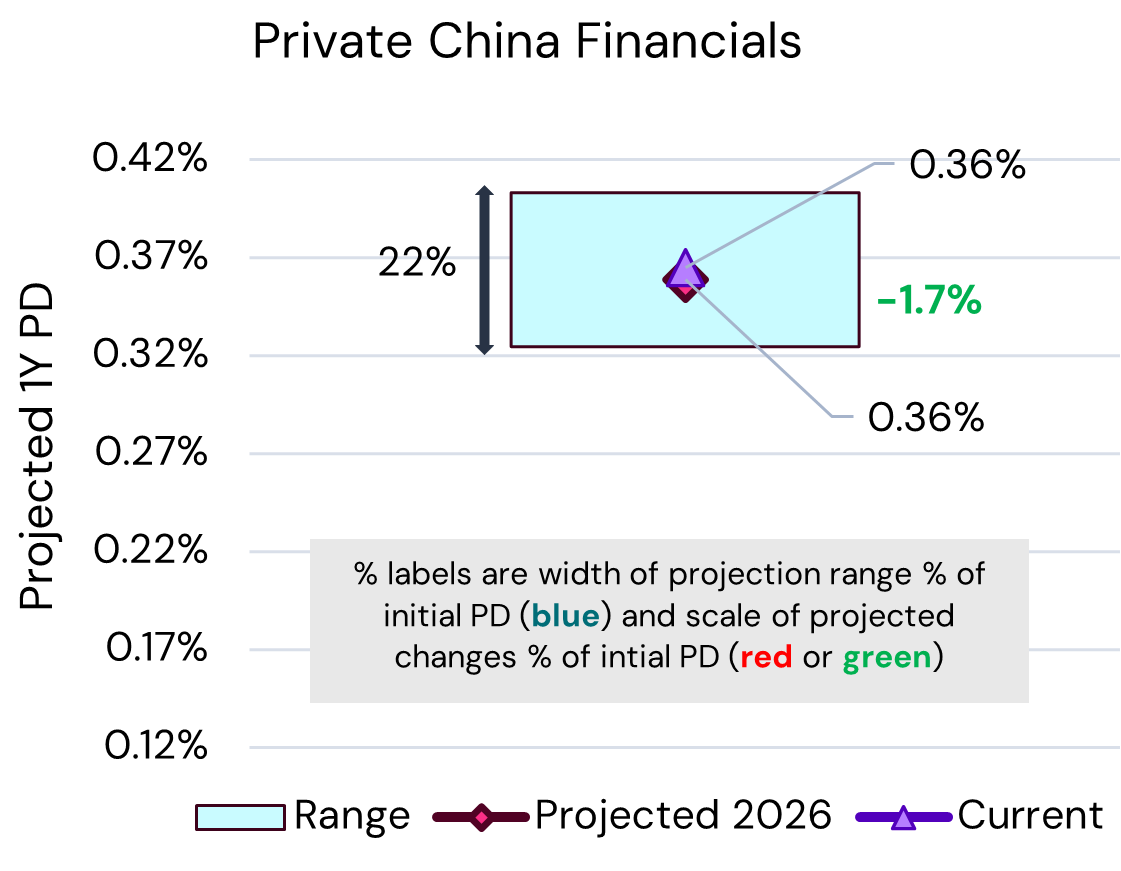

China Private Financials – Credit Risk Index (CRI) and Probability of Default (PD)

China Private Financials – PD Projections

Key Takeaways:

- Private Probability of Default Now & Projected Q4 26:

- Corporates 0.68% from 0.61%

- Financials unchanged at 0.36% (and wide range on narrow base.)

- Private Corporate credit migrations consistent bias to downgrades. Tariffs have hit exports and OECD projections are for slower GDP growth.

- Financial CRI volatile but stabilizing, expect Financials to show recovery after recent property-related problems.

Download PDF

Appendix: Methodology

Forecasts are based on two linear extrapolations – the actual Probability of Default (PD) trend and the PD conditioned on the short-term Credit Risk Index (CRI) trend. If these show different signs, then a turning point is possible. The combined forecasts is a weighted average with weights derived from relative goodness-of-fit of the two extrapolations.

This weighted average combination of PD and CRI trends is further adjusted by:

- The % of borrowers in the ‘c’ category for each country / borrower type.

- OECD GDP projections

The upper and lower range limits are derived from:

- Maxima / minima of the two extrapolations

- Standard error of the regression fits for the two extrapolations

- Volatility of the CRI