The Middle East conflict is once again exposing the fragility of global supply chains. As with Covid and Ukraine, the consequences are unlikely to be immediate – but they will spread across sectors in ways that are difficult to predict.

High profile casualties include tourism, airlines, energy and travel infrastructure.

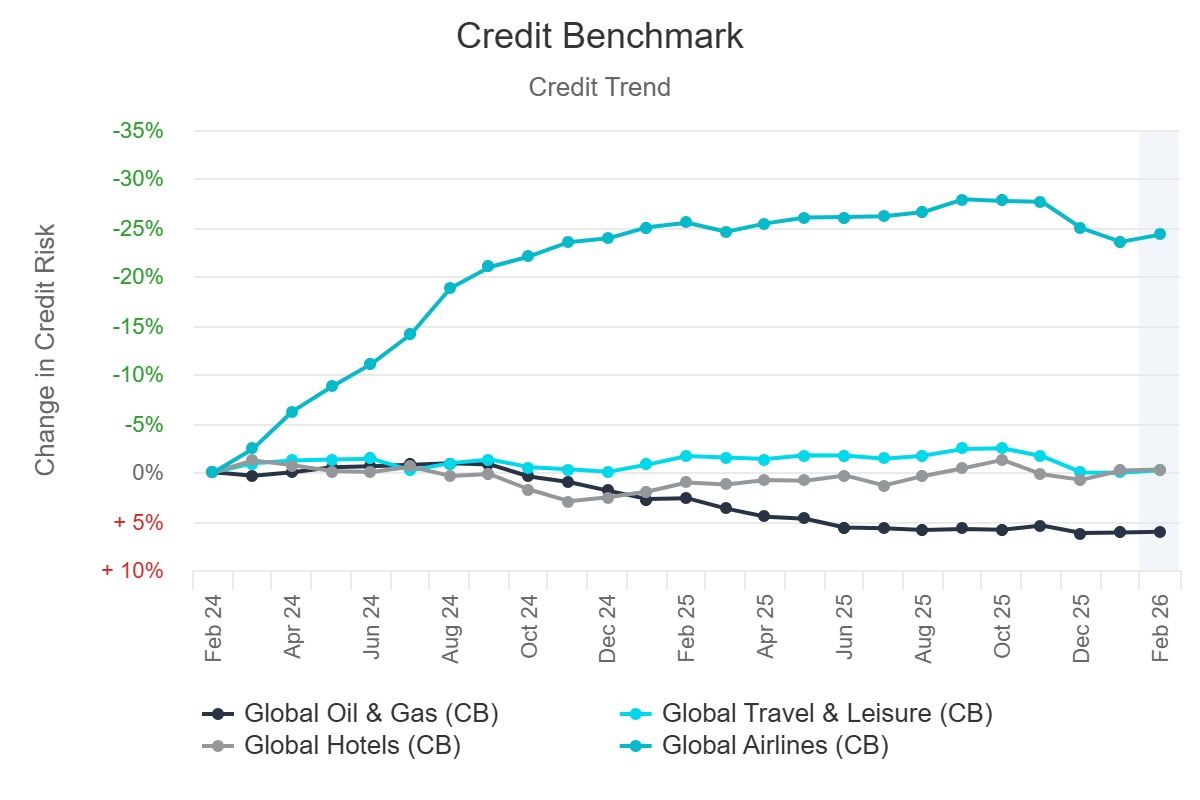

While the Travel sectors have partly recovered from Covid, more than 20% of the Travel & Leisure and Hotels segments are in the ‘b’ category or worse. Airlines have seen a huge credit improvement in the past 2 years, but that could unravel very quickly if airport and airspace closures continue or spread.

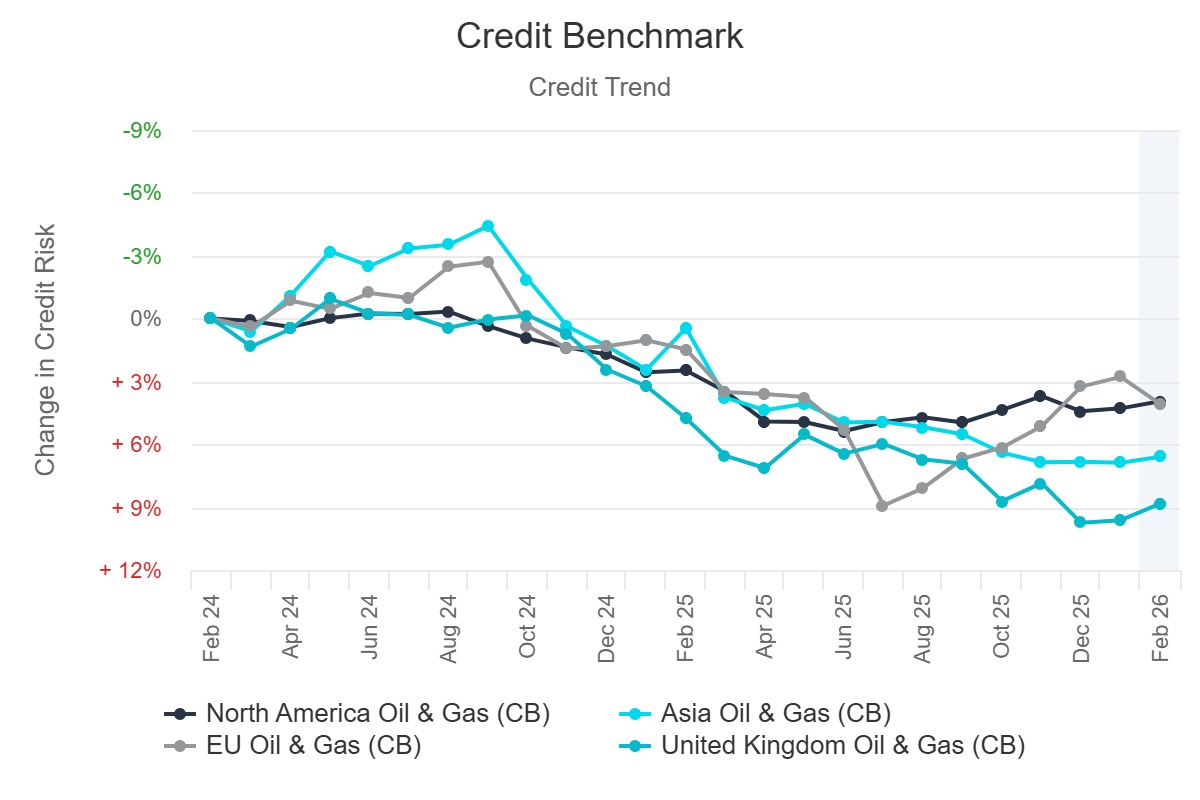

The impact on Oil & Gas is likely to show an East-West split despite Iran making exceptions for Chinese and Indian tankers.

Asia is very dependent on oil and gas from the Gulf, while the Americas can tap reserves with scope for major production expansion.Europe is already seeing gas price hikes, but they have some scope to increase their own oil supply, although the UK is unlikely to be able to bring North Sea production back in the near term.Globally, the energy industry has rebuilt its balance sheet in the past few years and less than 10% of the sector is in the ‘b’ category.

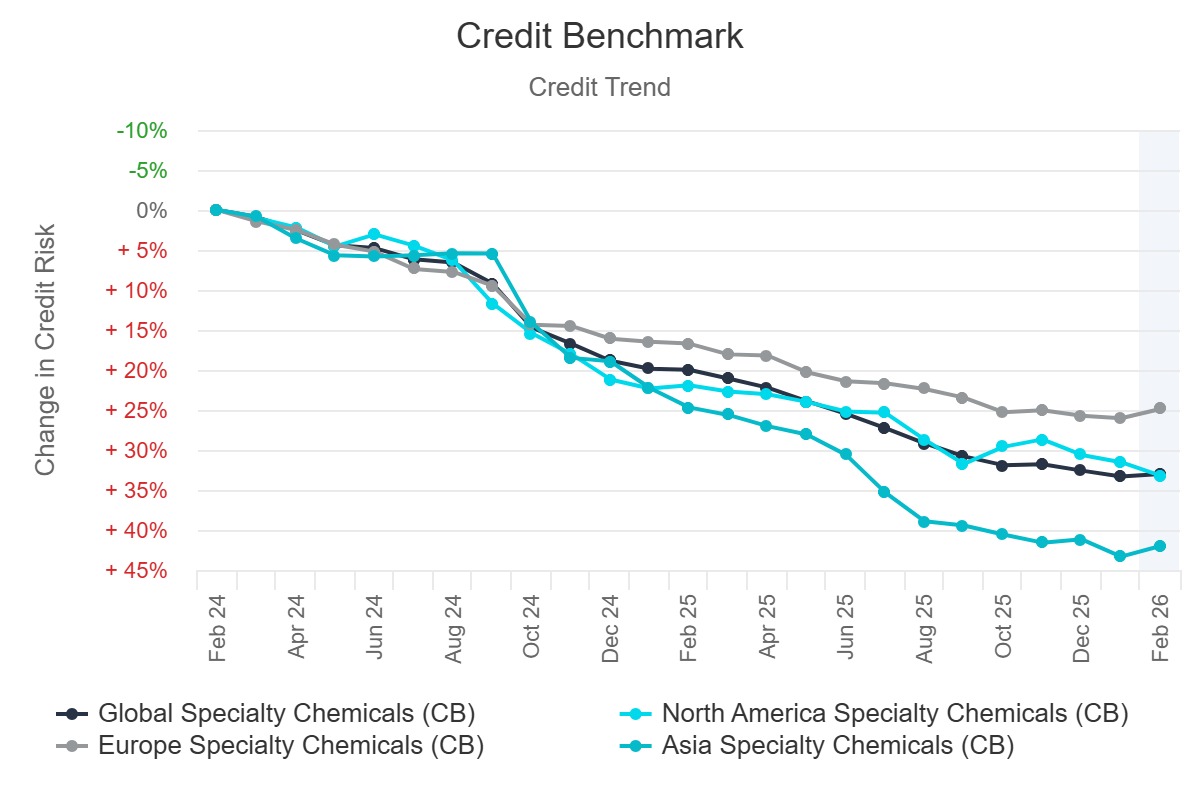

The Straits of Hormuz are critical for a large range of derived Oil & Gas by-products, including fertilizer and plastics.

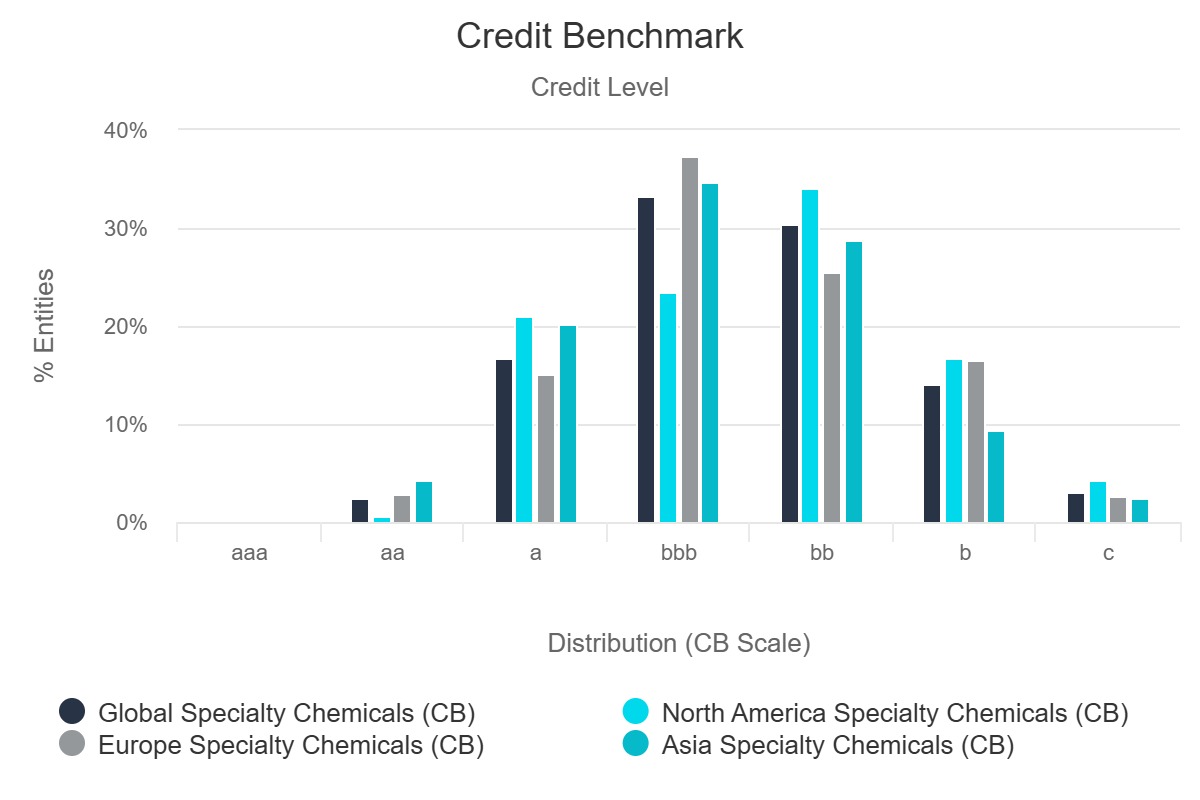

The Ukraine war disrupted the global fertilizer industry with knock-on effects on food producers. The Speciality Chemical sector has a small but significant exposure to the ‘c’ category, and its cumulative increase in credit risk of 20% – 40% over the past 2 years shows little sign of abating.

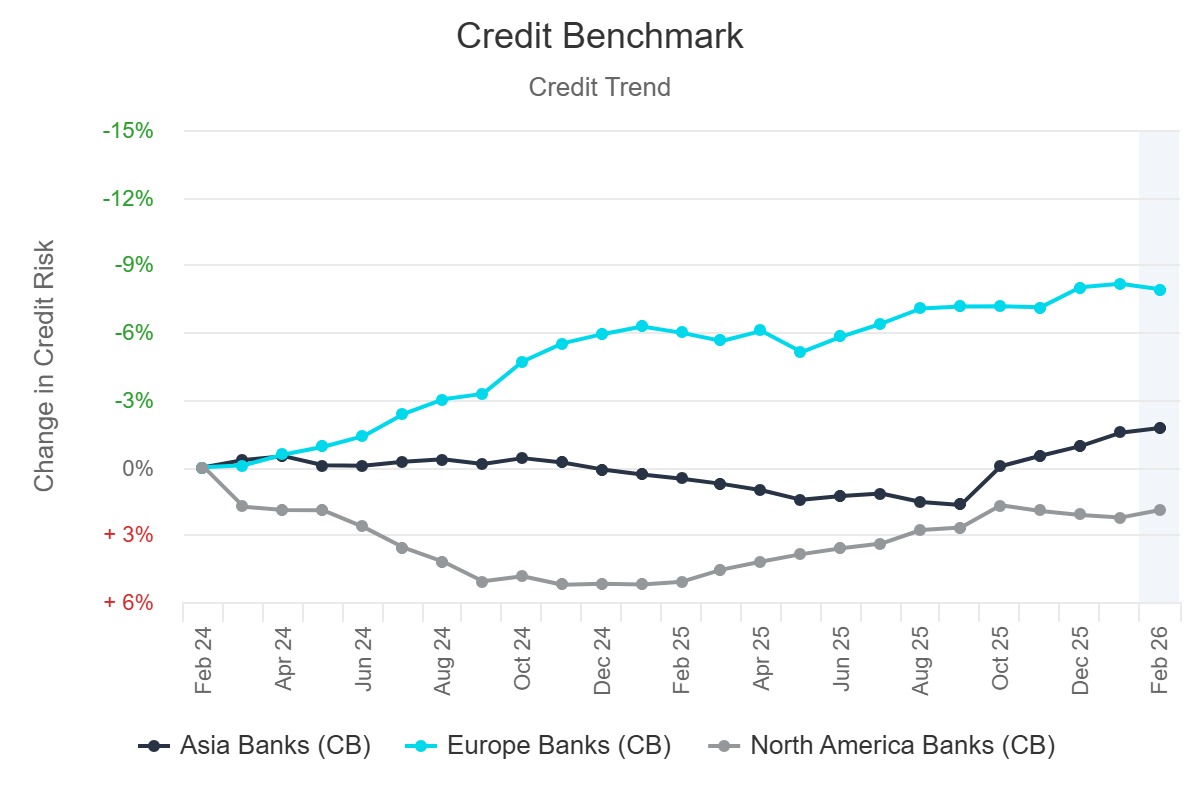

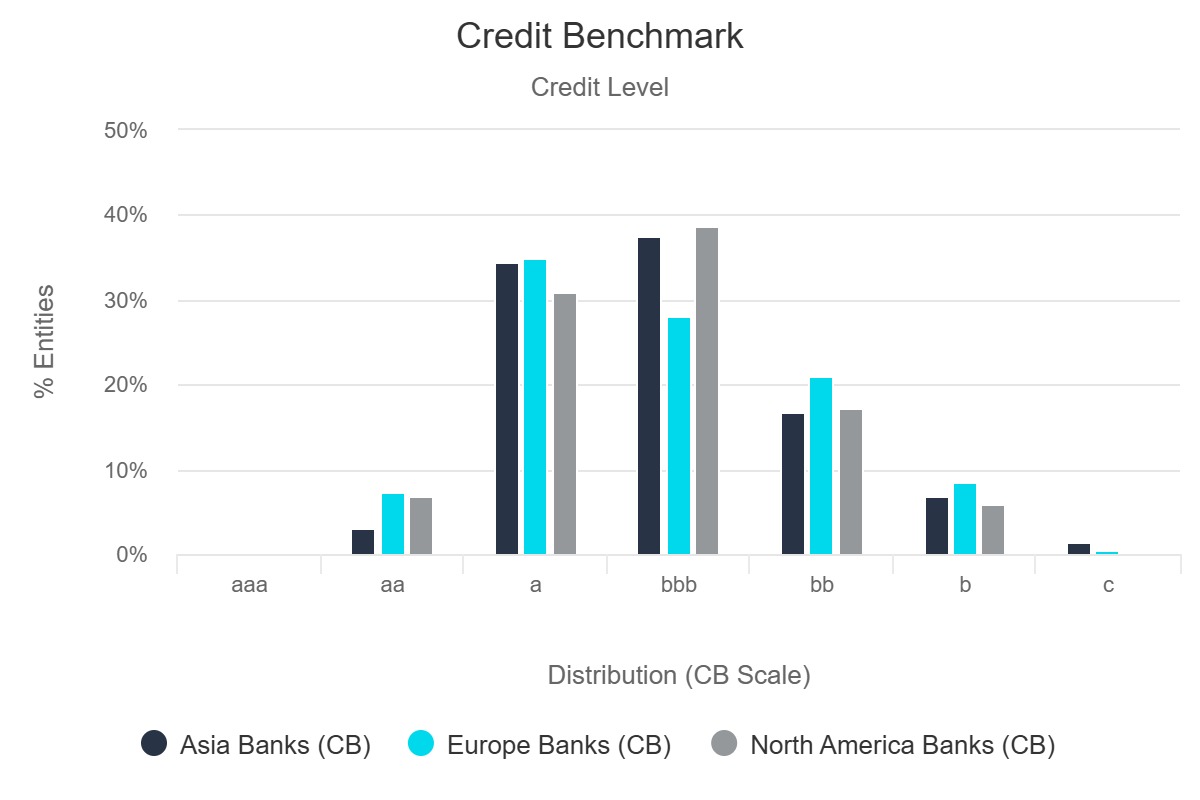

Attacks on infrastructure can directly affect loan collateral with Asian banks heavily invested in this previously safe asset class.

Asian banks are typically well-capitalized with a stable credit trend but a string of defaults in their Middle Eastern portfolios could compromise domestic lending with knock-on effects in China, Japan and South East Asia.

The US is already at risk of munitions shortages, so US defence companies can expect strong revenue growth for the next few years.

But commercial airline manufacturers face a sudden halt in new orders, so the defence and aerospace are likely to see divergent credit trends this year.

US commercial Aerospace looks especially vulnerable, with a very high % in the ‘b’ category and a difficult short term outlook.

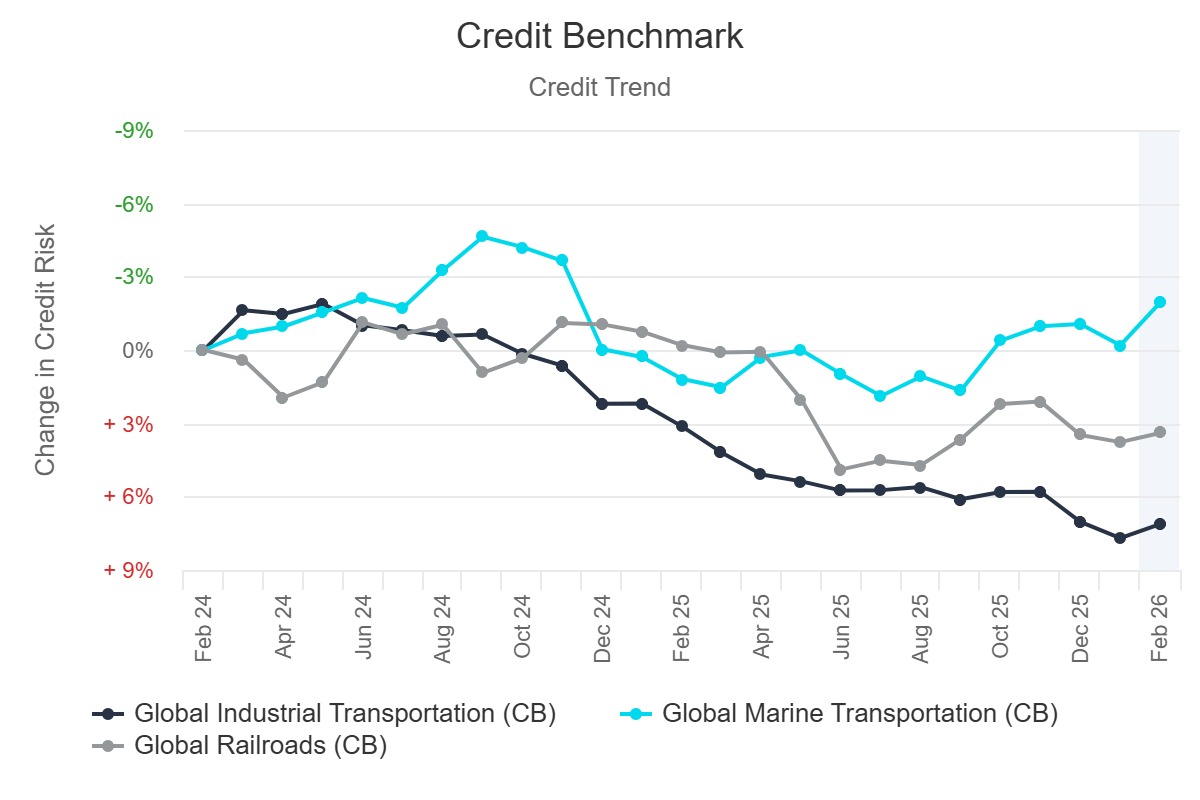

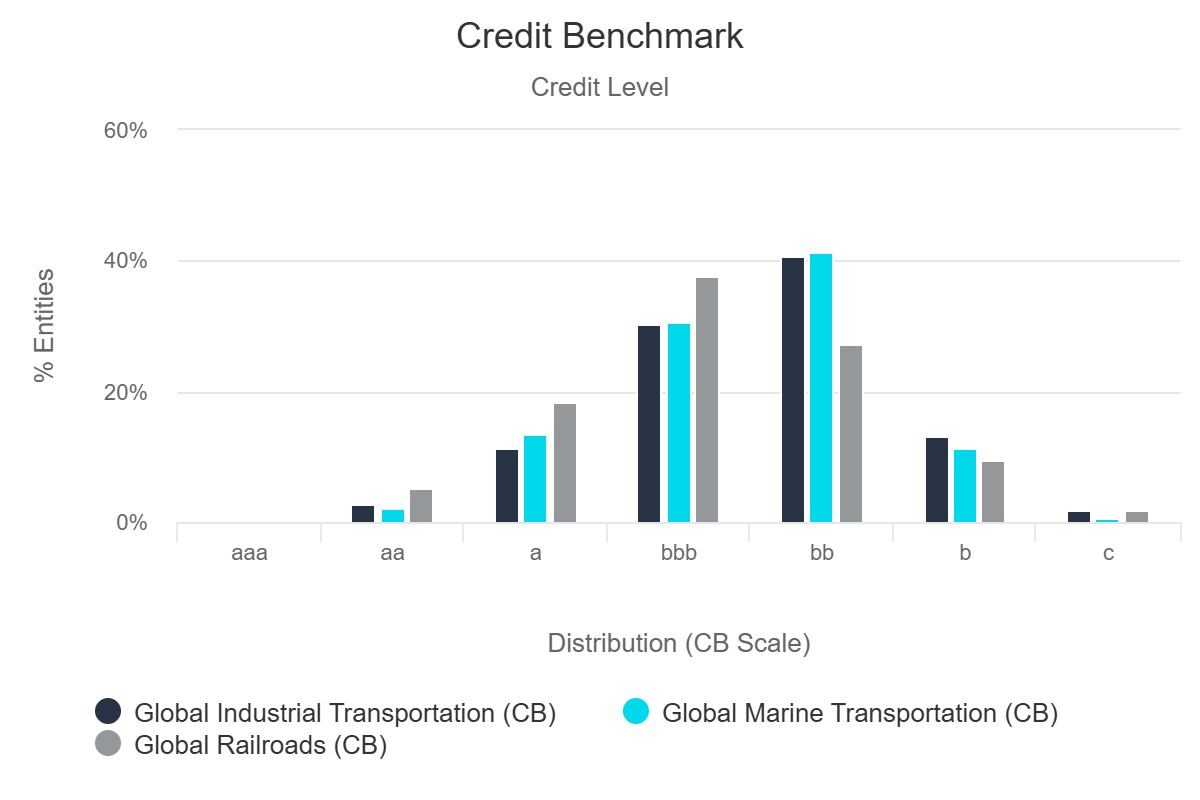

Transportation will see widespread disruption.

Insurance costs have either spiked or cover has been completely withdrawn. The US has announced waivers to allow foreign flag vessels to transport oil and gas in US waters, but this is a rare example where redeployment might be possible. Global trade volumes are likely to shrink if energy costs remain high, so expect marine and airfreight sectors to suffer most while railroads and trucking are likely to see a spike in market share but reduced volumes overall. The recent improvement in Marine Transportation is likely to reverse, especially due to rising insurance and energy costs. Railroads – already higher credit quality – are likely to benefit.

What’s next: default risk updates will start reflecting this shift within weeks.