The energy shock of 2026 could become a bigger problem for credit markets than the shock of 2022, when Russia invaded Ukraine. That’s because credit conditions and credit pricing moved in starkly different directions before each shock happened. Credit conditions were already worsening before this shock, whereas they were improving leading into the last one.

I’ve been looking at data from Credit Benchmark, a data analytics firm that I’ve advised. It anonymously aggregates the internal risk ratings of credit analysts at 40 large multinational banks on more than 120,000 obligors globally — including corporates, financials, business development companies, sovereigns, municipalities and more. Many of them are private and untracked by the big bond rating firms.

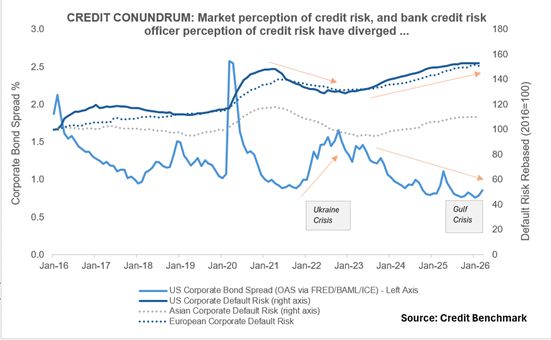

Credit risk has been building in Europe and the U.S. for a few years – meaning credit risk analysts at banks on net have been downgrading their internal ratings on corporate borrowers, even as the market’s pricing of credit risk has diminished, as embodied in spreads. Between January 2023 and January 2026, downgrades on U.S. corporate borrowers exceeded upgrades 5,624 to 4,902. It’s been a consistent, modest rise in risk.

This stands in contrast to the 2022 energy shock episode. Back then credit risk was diminishing – meaning internal bank upgrades exceeded downgrades — as the global economy recovered from the Covid crisis. Many businesses were simply flush with cash. From January 2021 to January 2023, upgrades exceeded downgrades 4,135 to 2,769. Back then, spreads jumped even as credit upgrades outpaced credit downgrades. In other words, market perceptions of credit risk were acute even though credit risk was improving, the opposite of this episode.

As the chart here shows, U.S. corporate default risk has been increasing in the U.S. and Europe, while Asia is generally steady. We’ve all seen the headlines of late – stress at Blue Owl Capital, the asset manager specializing in private debt financing; the bankruptcy of Tricolor Holdings, a subprime auto loan originator, and First Brands, an auto supplier.

Credit Benchmark analysts tell me they are seeing cracks in some sectors, such as the BDCs, but not yet an obvious crisis. It is time to be watching this space.

In the past year, the sectors with the biggest deterioration in credit included Europe iron and steel, European industrial metals and mining, European employment agencies, U.S. chemicals, European auto parts, U.S. clothing and accessories and U.S. trucking, according to Credit Benchmark’s data.