Traditional pension funds have had a difficult decade: although low or even negative interest rates have been good for asset prices, this benefit has been outweighed by the cost of growing liabilities. According to the Pew Charitable Trusts, the total pension gap across the 50 US Federal States is estimated to be around $1trn.

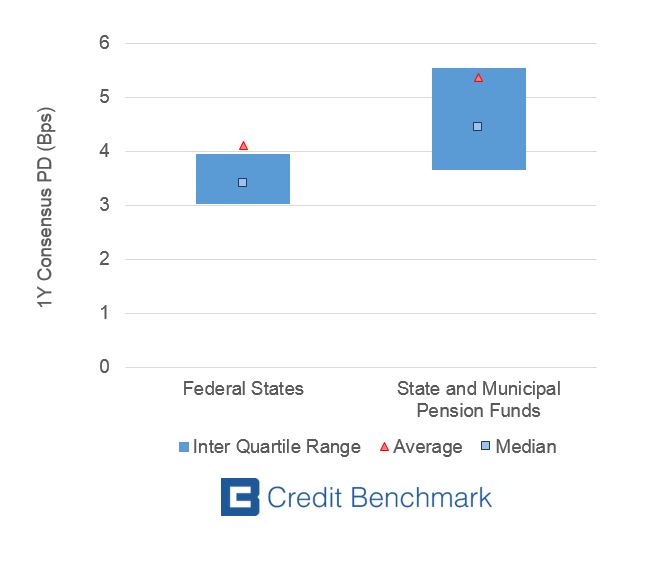

As the chart below shows, this is partly reflected in the credit risk assessments; the typical State or Municipal pension fund has a default risk that is at least 30% higher than that of the typical Federal State.

The interquartile range of credit risk estimates for pension funds is, understandably, larger than that of the actual states. There are multiple pension funds in each state and some will have significantly stronger funding than others.

According to the National Association of State Retirement Administrators, the average funding level is 73% of liabilities, but there are major differences between states. Delaware, Idaho, North Carolina, South Dakota and Wisconsin are close to 100% funded. Alaska, Connecticut, Illinois, and Kentucky are all around 50%.

According to the chart below, the typical state pension fund has an average annual default probability of more than 5 Bp, giving a CBC* of a+. The equivalent for the average state is around 4 Bp, on the boundary between a+ and aa-. Both distributions are clearly positively skewed, with the average default risk significantly higher than the median for both sets of obligors.

The $1trn funding gap is unlikely to close unless there is a sustained rise in long term interest rates. Short term interest rates are expected to continue to rise in 2017, and long term bond markets have retreated from their highs of 2016; but the recent long bond rally means that the credit risk gap between States and their Pension Funds is likely to persist.

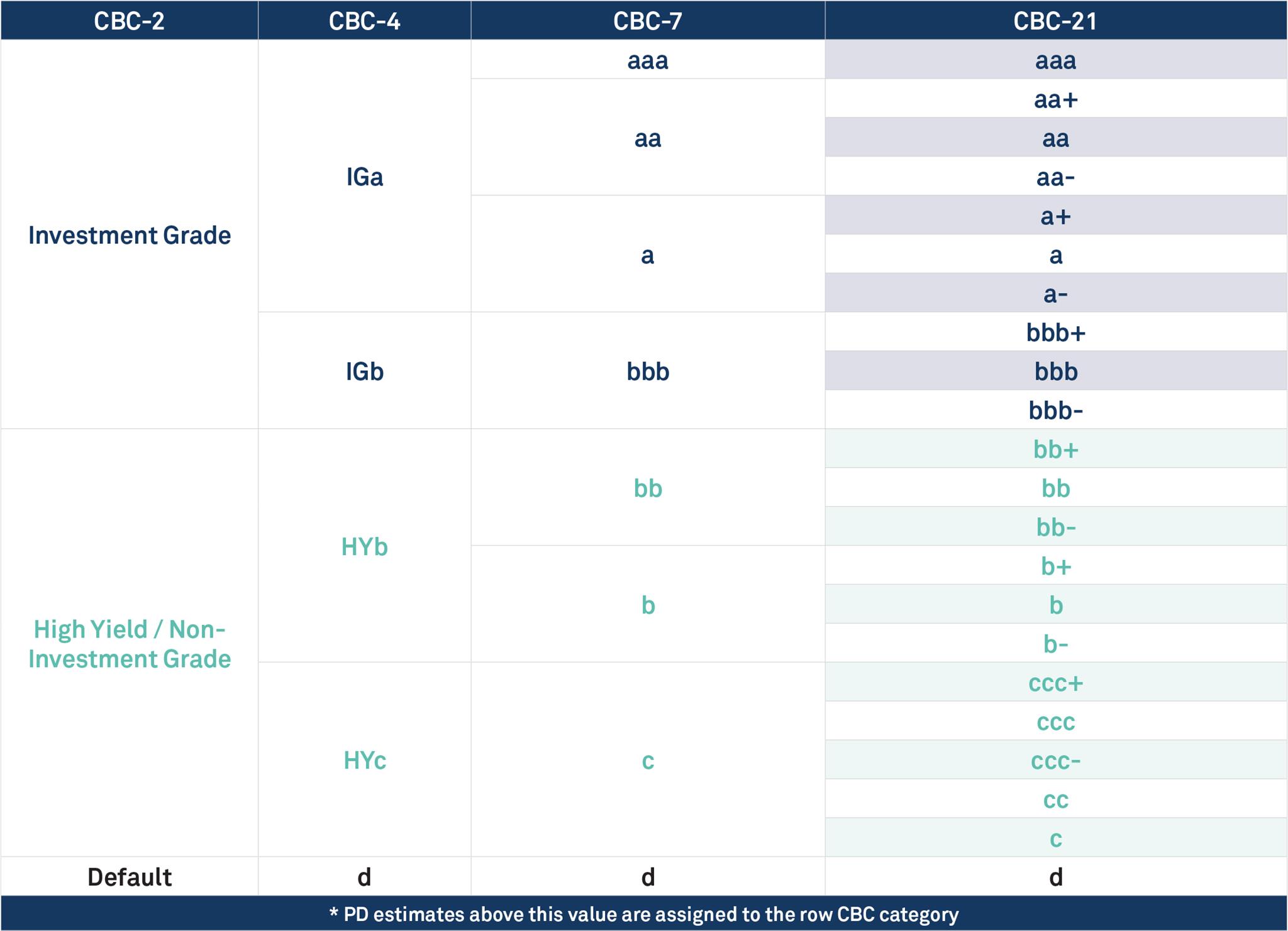

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of bbb+ is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

{kind=link}