African economy on tightrope but growing commodity exports may see Sovereign default risk improve by 10%+ in next year

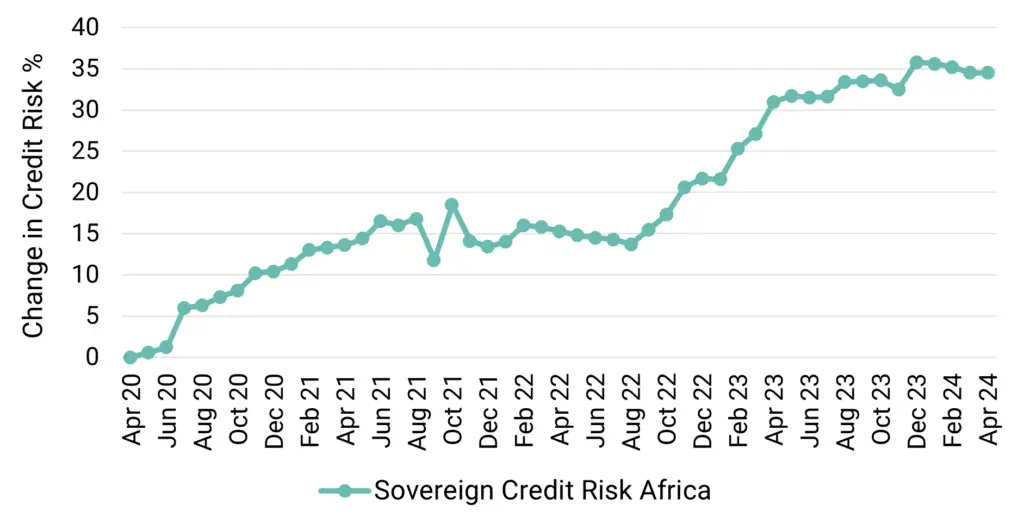

Steady credit deterioration for African sovereigns since 2020

African Sovereign credit ratings have deteriorated significantly in recent years, hit hard by Covid, the Ukraine war, climate change, military coups and Sovereign debt defaults. The chart below shows that Credit Benchmark’s consensus credit rating index for African Sovereign default risk has increased by 35% since early 2020, especially after the Ukraine invasion.

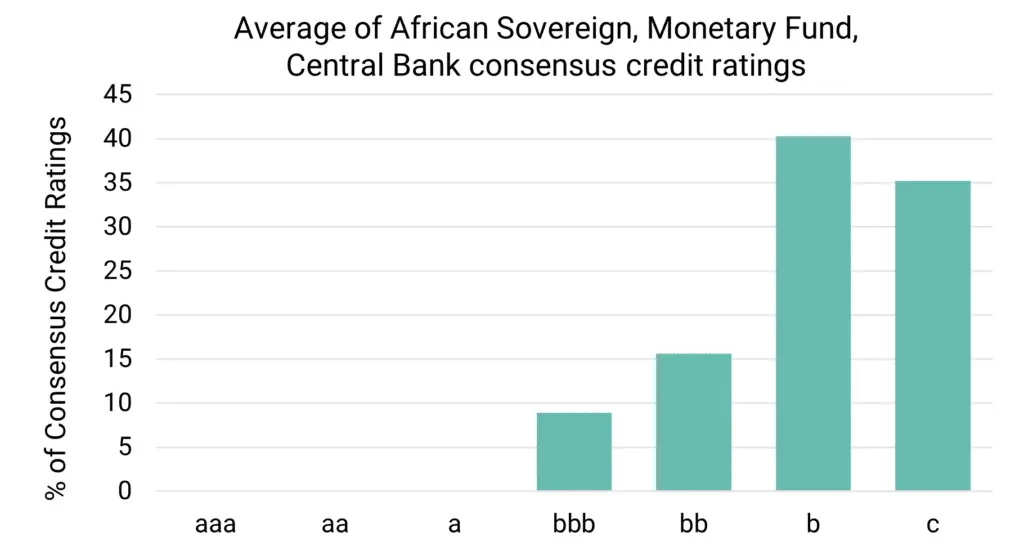

Most African Sovereigns are non-investment grade, mainly in the b and c credit rating categories.

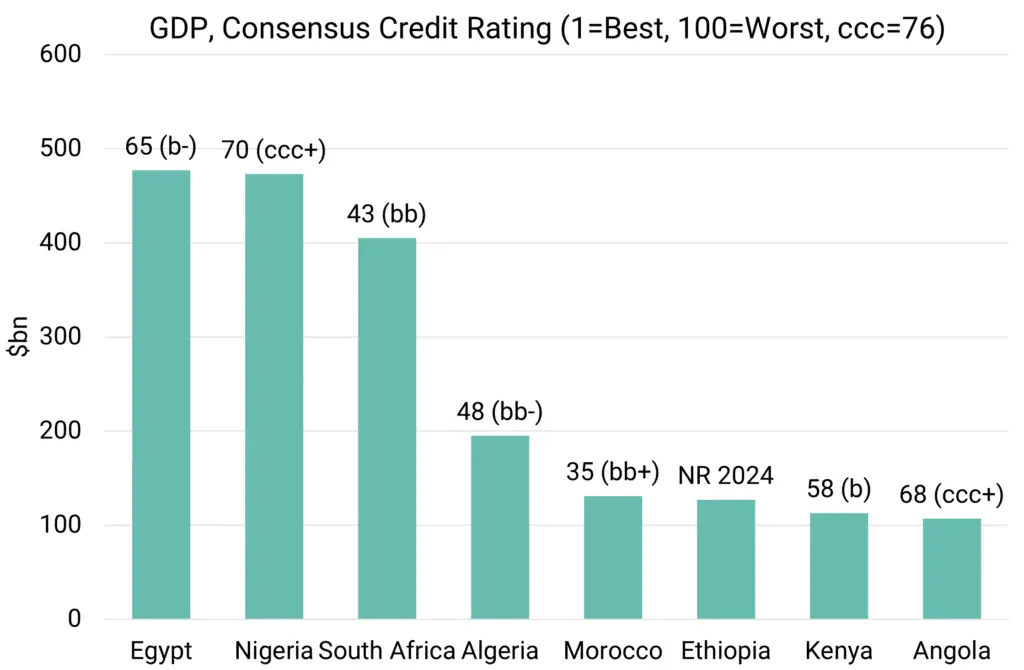

But some African Sovereigns have fared better than others. The 8 largest economies generate nearly 70% of African GDP; the chart below shows the breakdown with detailed 100-point consensus credit ratings.

Prior to technical default in Q4 2023, Ethiopia was highest risk with a consensus credit rating of 76 (ccc+); lowest is Morocco (consensus credit rating = 35, bb+).

In recent years, oil-rich Nigeria has deteriorated from b to ccc+ (consensus credit rating = 70). Troubled Kenya has also deteriorated but remains in the b category (consensus credit rating = 58).

Angola (consensus credit rating = 68, ccc+) has slightly improved, but is below the main credit rating agency ratings.

South Africa (consensus credit rating = 43, bb) and Morocco (consensus credit rating = 35, bb+) have remained stable. Egypt – Africa’s largest economy – dropped from b to ccc+ in recent years but has since recovered (consensus credit rating = 65, b-).

Algeria (consensus credit rating = 48, bb-) has very patchy credit rating agency coverage; but consensus credit data shows an improving trend over the past 9 months.

Shifting geopolitics may drive demand for African resources

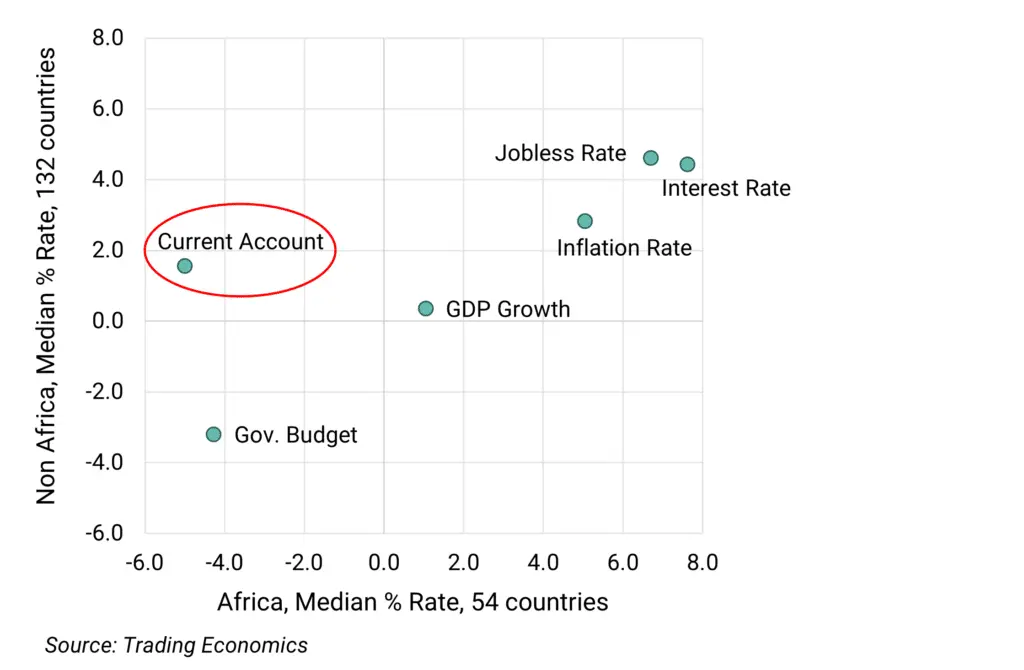

Africa may be rich in natural resources, but its 12% share of the global population earns just 3% of global GDP; sustained growth has often been hampered by some unique obstacles to economic development. The chart below plots key current economic indicators for Africa vs the rest of the world:

Median interest rates, inflation, unemployment and budget deficit in Africa are above the global ex-Africa median – but so is current GDP growth. The main outlier is the Current Account; Africa is not exporting enough to cover import demand.

But shifting geopolitics may bring new benefits: technology needs and supply chain shocks are driving China, Russia and the US to compete directly for favourable raw material trade deals with numerous African countries.

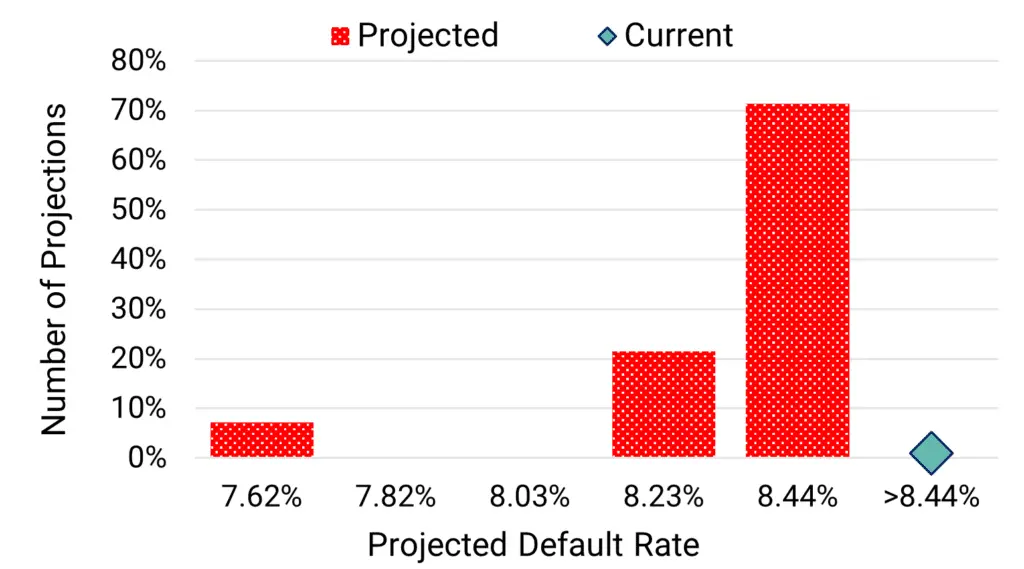

Using Credit Benchmark consensus credit rating data to project recent trends and credit cycles suggests the following range for 49 African Sovereign & Central Bank default risks over the next 12 months:

This chart is derived from 5th to 95th percentiles. It shows a high (70%) probability of a modest (13%) decline in median African Sovereign default risk over the next 12 months, and a small (<10%) possibility of a more significant drop of 20% or more. There is a small chance (<5%) that median Sovereign default risk increases.

This range in the previous chart shows possible projections of African Sovereign default risk using a mixture of linear and non-linear extrapolations. It is heavily influenced by trends in the proportion of obligors in the c credit rating category, which is the source of most defaults.

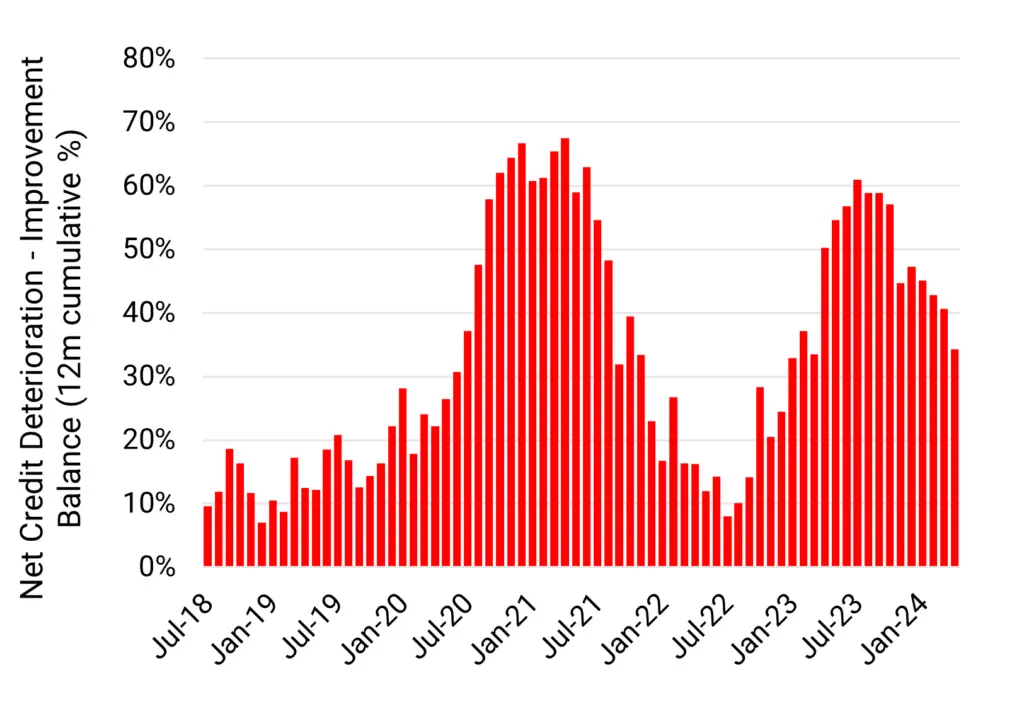

Credit cycles have a major impact on the pace of credit downgrades and hence the proportion in the c credit rating category. The balance between credit deteriorations and credit improvements in the African Sovereign universe shows the scope for turning points (obligors beginning to upgrade from the c credit rating category back into the b categories).

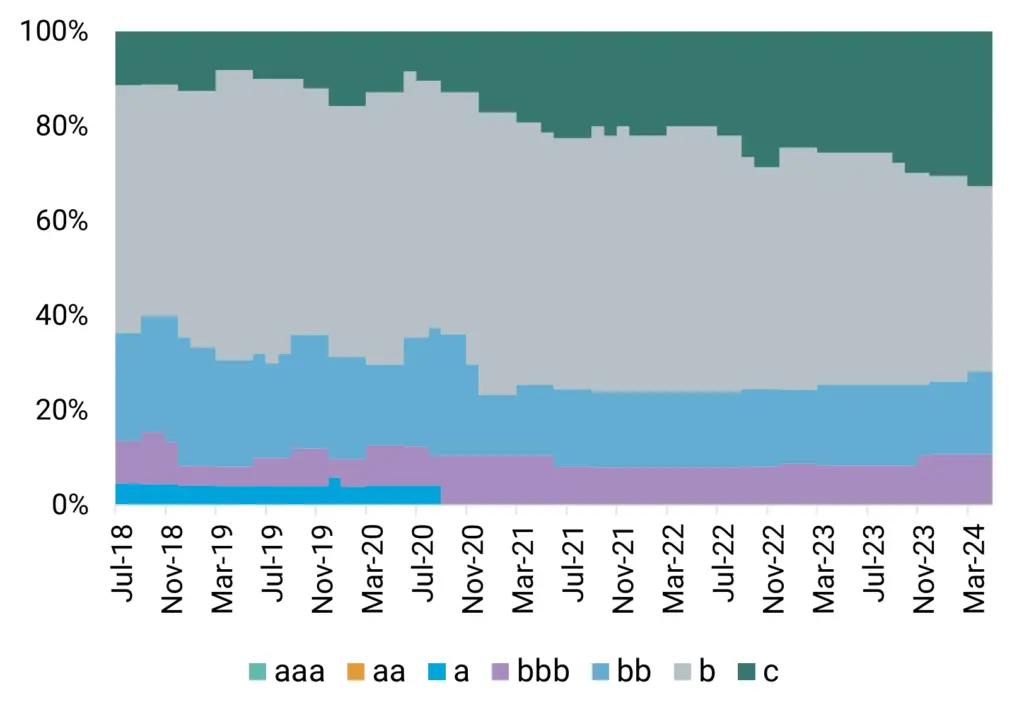

The two charts below show the credit rating category mix over time (left chart) and the 12-month cumulative balance in credit deteriorations vs. credit improvements (right chart).

The c credit rating category has more than doubled since 2018; it was particularly steep during Covid, before stabilizing in 2021. But the Ukraine invasion brought renewed credit decline and it currently stands at around one third of all African Sovereign ratings.

During Covid, rolling 12-month credit deteriorations were nearly 70%; this dropped to 10% during the recovery before spiking again to 60%. This recent trend is projected to continue, so the pace of credit downgrades is also likely to slow. At the very least, the c-category proportion is expected to stabilise and there is a possibility that African sovereign credit ratings move into a net credit improvement phase, especially if global commodity demand continues to grow.

Credit improvement on the horizon for African sovereigns

The African economy is on a tightrope – climate change and political instability are major negatives, but the growing need for raw materials of the increasingly competitive global superpowers may bring some benefits in the form of investment and growing exports. We forecast that African Sovereign default risk will improve by more than 10% in the next 12 months

Credit Benchmark offers entity-level Credit Consensus Ratings on over 105,000 counterparts and borrowers globally, alongside an extensive suite of analytical tools and products.

If you would like a free analysis of the default risk projections of your own portfolio, we encourage you to get in touch here.

Download

Please complete your details to download the PDF of this report: