Oil price volatility has jumped. Annualised daily volatility reached a near term low of 19% earlier this year, but it is currently close to 30%, mainly because of a high level of uncertainty about supply. For example, Brent Crude recently fell 7% in one day (from a recent high of around $80) due to Libyan production returning to the market. The oil industry faces long term structural headwinds, but geopolitics are currently causing price spikes as well as drops. Recent price highs were driven by renewed US sanctions on Iran, which will reduce global output later this year; OPEC have very limited spare capacity to offset this. Research by Bank of America Merrill Lynch estimates that complete removal of Iranian output – without any replacements from other oil-producing countries – could lift the price per barrel to $120 from the current level of around $80. Iran has even threatened to retaliate against US sanctions by closing the Straits of Hormuz – which some commentators think could take the oil price as high as $250. But in practice there are likely to be some sanction waivers, and China has already announced plans to take Iranian oil in response to their current trade friction with the US. And that trade friction also threatens to depress demand. So although the balance of geopolitical risks is still towards higher prices, volatility is likely to persist.

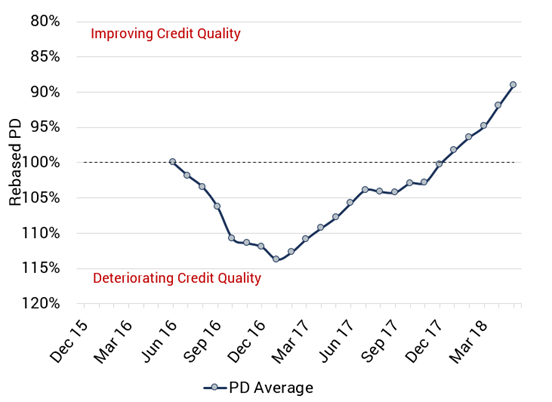

US oil companies have successfully distanced themselves from some of the extremes of the global market. The US is now a net exporter of oil, but recently announced domestic stockpiles are below the seasonal average levels – so there is scope to switch supply between local and global demand sources. The more favourable environment for US oil producers is reflected in bank-sourced credit data for nearly 400 companies in the US oil and gas industry. The charts below show that the credit distribution for these companies has improved in the past year; the proportion of companies in the b and c categories has reduced, with 40% of the US Oil & Gas sector now in the bb category. There have also been minor increases in the a and aa categories. This reflects a slow but steady improvement in average credit quality of around 25% over the past 18 months.