US equities have now had 3,453 days without a correction of 20% or more – the longest bull run in US financial history. And since mid-2016 alone, the Dow index is up more than 40%. European equity returns have been more modest but still respectable: France, Germany and the UK are all up about 25% (in local currency) over the same period.

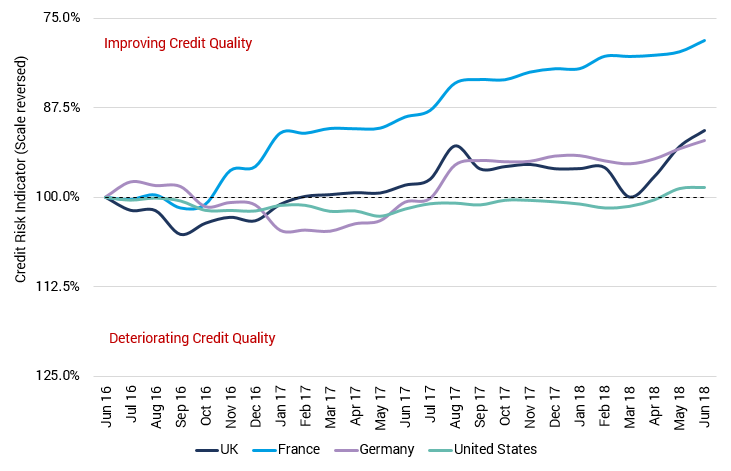

However, the credit trends for the constituent companies in each index are very different. The chart* shows average credit risk levels for each country, based on the constituents of the Dow Jones, the CAC40, the DAX30 and the FTSE100. The credit risk of the Dow constituents actually increased slightly until mid-2017, and has since marginally improved. Credit risk for the UK and German indices also increased before modestly dropping from March 2017 onwards; for the FTSE100 constituents, the prevalence of Dollar earners combined with a weak currency has been credit-positive.

But France has shown a dramatic drop in credit risk, starting back in late 2016 and currently standing at close to a 25% improvement. In early 2017, the French financial markets were worried about a Far-Right election victory; CDS spreads expanded but bank credit views remained stable to optimistic over this period. The continued improvement is probably a reflection of French economic growth and employment picking up, closing the gap with Germany. And some commentators think that France could be a major beneficiary from the UK’s withdrawal from the EU.

Equity and credit can diverge for long periods: equities reflect earnings growth while credit trends reflect balance sheet strength. But if equity markets reverse, the credit position in each country becomes increasingly important.

*rebased to 100%, vertical scale reversed