If the winner of the US presidential election on November 8th follows most of his or her party platform, there could be some big changes in the corporate credit world. That’s a big if, of course.

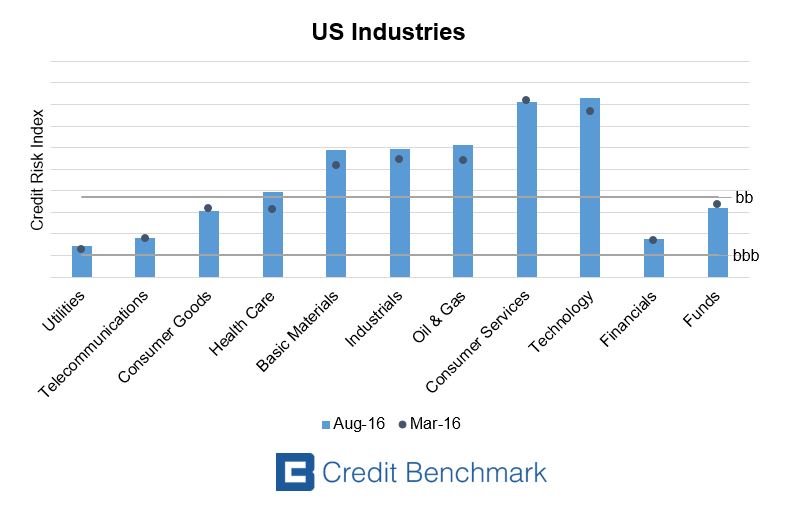

As the chart shows, it doesn’t look like lenders to Corporates are expecting any major changes from this contest, with the CBC* for American companies staying at [bb] from March to August. There was a slight negative tendency within the band, but that is probably due to weak GDP growth rather than political worries. Lenders may be reserving judgement until they see what policies are actually put into practice.

Either way, there should be good news for construction: Donald Trump promises to build a huge wall on the Mexican border, while the Democratic platform is committed to “the most ambitious investment in American infrastructure since President Eisenhower created the interstate highway system”.

But the Democratic platform also promises to “incentivize companies to share profits with their employees on top of wages and pay increases”. Under Hillary Clinton, US corporate profits may be facing the end of a long and benign era.

On the other side, much of the Republican agenda looks credit-friendly. The platform calls for a major retrenchment of Federal regulation, which could reduce some of the costs and fines which have to be paid before interest and principal. It calls for simpler corporate taxes, and a removal of the tax on repatriated profits. It also promises to promote domestic producers of energy, whose average CBC has slipped a little since March.

But one Republican idea would not be good for credit quality. The GOP want to see the central bank following “sound economic principles and sound money” rather than the current “easy money and loose credit”, while Trump has accused the Fed of being “more political than Secretary Clinton”. Trump is expected to make major changes to the Fed team in 2018, and the monetary authority might be tempted to appease either administration with faster rises in policy interest rates. That would be a shock to the corporate system.

Party political platforms and candidate statements can be unreliable guides to the actual outcome, mainly because of America’s legislative gridlock. Lenders and borrowers are well aware that most laws come very slowly and major changes are rare. This election is unlikely to provide a widely popular president whose party has firm control of Congress, so that gridlock is likely to persist. The US Sector CBCs seem to support that view.

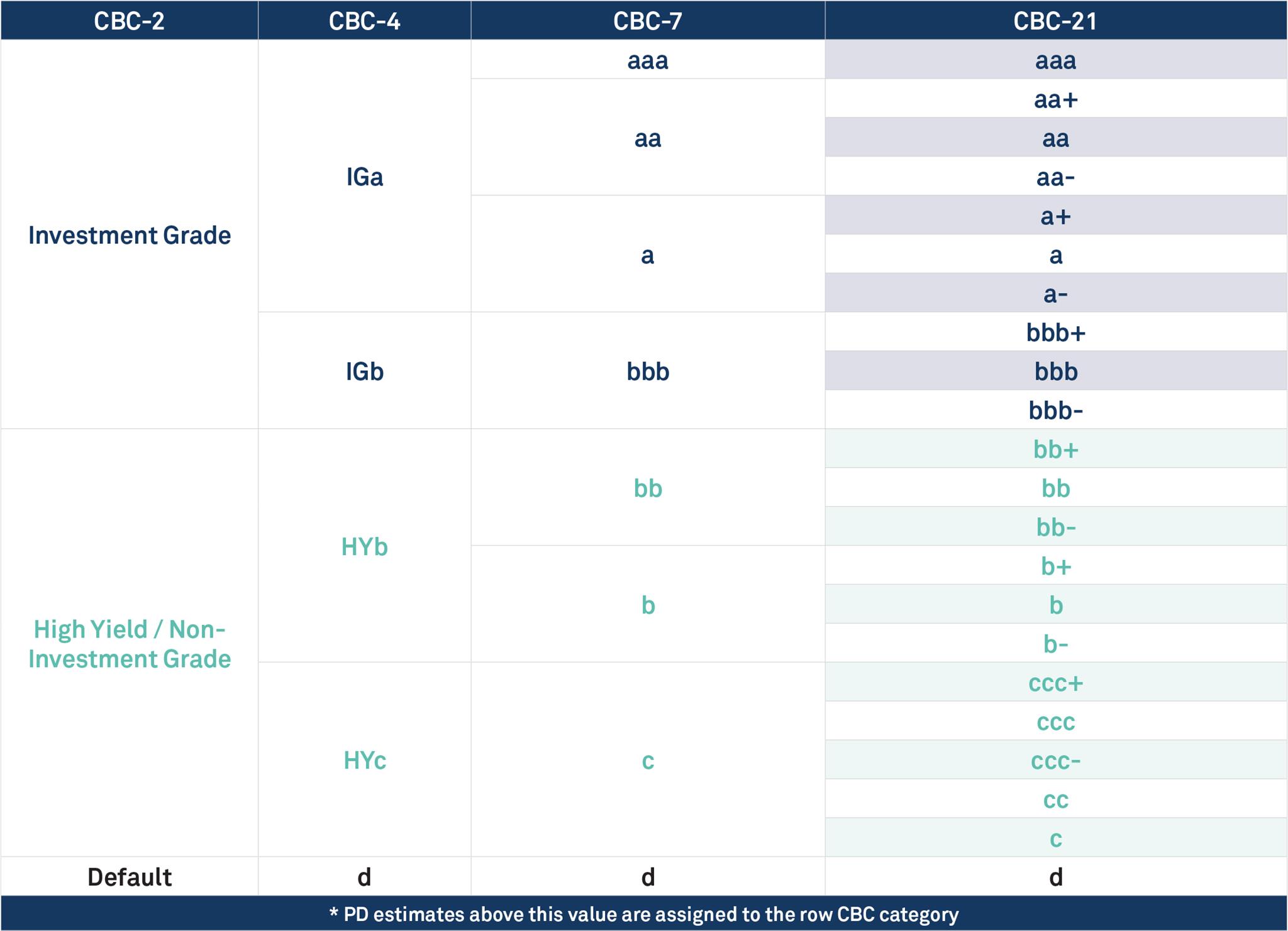

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of [bbb+] is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

{kind=link}