In 2009 the UK’s Debt Management Office (DMO) oversaw record gilt issuance of £227 billion ($275 billion). At the time, Pimco’s Bill Gross described UK government debt as resting on a “bed of nitroglycerin”. Since then, however, the total return for investors in gilts has been 60%.

Gilts have benefitted from several tailwinds: the Bank of England’s quantitative easing programme; strong demand from pension funds aiming to “derisk” by hedging interest rate and inflation liabilities; and a generally improving economic and fiscal picture.

Gilt issuance in 2016/2017 set to fall to £115 billion, the lowest in a decade. The FT recently reported that foreigners were heavy sellers of gilts in January, but they represent less than a quarter of all investors and the UK has not been their primary target: earlier this week, the yield on the 10-year gilt was 136 basis points lower than the equivalent US Treasury, the biggest spread since 1992.

However, there are reasons for all investors to be cautious. In the run-up to the Brexit referendum the CBC* for the UK Government dropped one notch. The underlying probability of default estimated by banks recovered after the vote, but it is now reaching new highs. By contrast, overall sovereign credit quality in Europe is improving.

This is reflected in credit default swaps, where the five-year cost of insuring against UK Sovereign default jumped from 33 basis points to 50 basis points in the immediate aftermath of the Brexit vote. It has since edged lower, though it is still higher than it was in 2015.

Since the Brexit vote, Sterling has dropped 18% against the US dollar. Although this weakness is primarily due to uncertainty about the outcome of the negotiations with the EU, it is also being driven by the divergence of monetary policy compared with the US. While the Federal Reserve has paused quantitative easing and is now in the process of normalizing interest rates, the Bank of England has voted today to delay any rate rise despite record employment levels and rising inflation.

Gilt issuance may be low, but bank-sourced data shows growing uncertainty over the credit impact of a hard Brexit and possible monetary tightening.

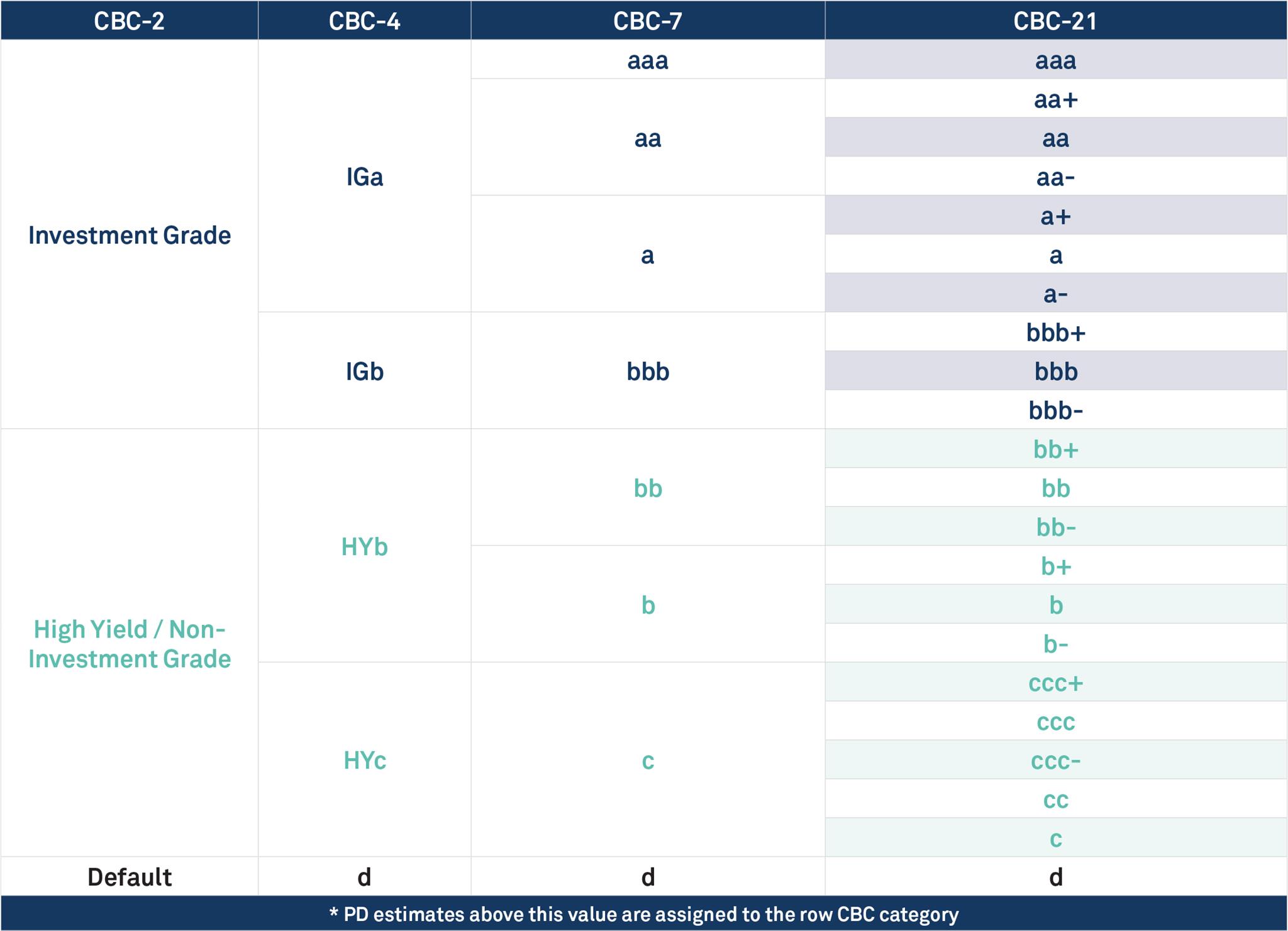

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of bbb+ is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

Disclaimer: Credit Benchmark does not solicit any action based upon this report, which is not to be construed as an invitation to buy or sell any security or financial instrument. This report is not intended to provide personal investment advice and it does not take into account the investment objectives, financial situation and the particular needs of a particular person who may read this report.

{kind=link}