Global corporate credit risk increased nearly 20% in 2020. Global Financials credit risk increased nearly 10%.

The global percentage of investment grade corporates dropped from 50% to 46%.

The proportion in category c has more than doubled.

North American credit risk rose 24%. Sovereign risk has risen by 5%.

Fallen Angels: nearly half of the Travel and Leisure sector dropped from investment grade to high yield. The average across all sectors is 14%, compared with 8% for the same period in 2019.

Rising Stars: nearly 20% of the Aerospace and Defense sector moved from high yield to investment grade, but more than a quarter of the same sector are Fallen Angels – showing how Covid is disrupting traditional business classifications.

A number of global industries saw credit risk increase by more than 30%. In some global sectors, credit risk increased by as much as 70%. Regional increases have been even higher: US Hotel credit risk rose by a staggering 340%. Airlines globally deteriorated 160%, equivalent to two notches in the 21-category credit scale. UK Aerospace insolvency risk rose 56% and is still deteriorating.

Global leveraged loan private issuer credit quality deteriorated more than 60%; public issuers by about 40%.

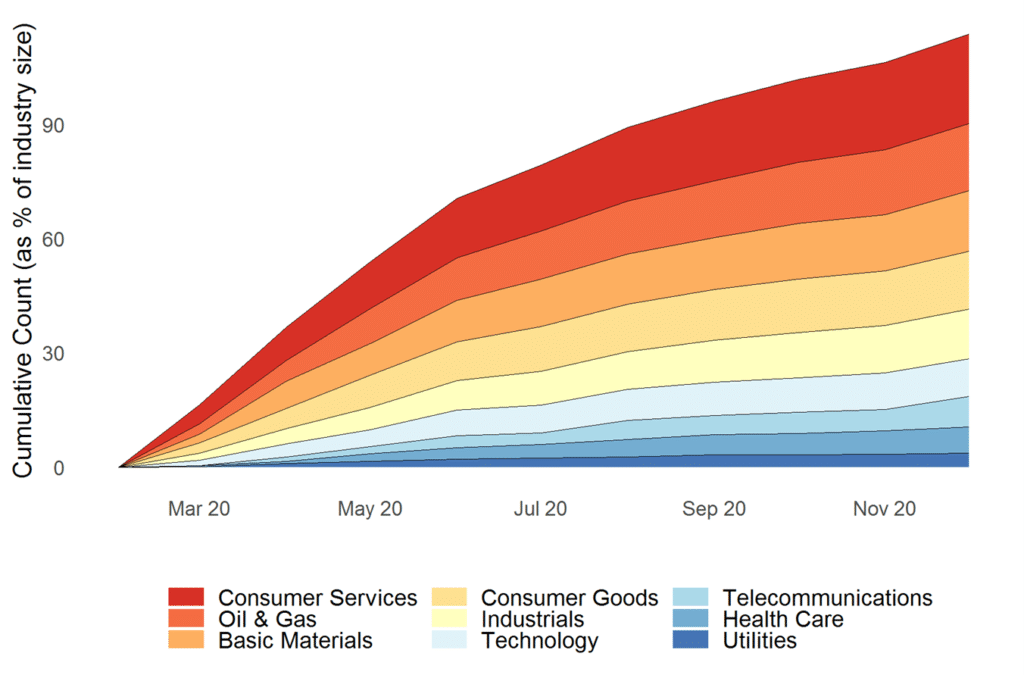

Figure 1.1 shows the cumulative increase in Fallen Angels, with each layer showing the cumulative % total of the respective industry universe, by December from a March start date corresponding to the onset of the pandemic.

The 2020 pandemic brought various forms of disruption, hardship and human tragedy. Governments and businesses around the world had to rely on trial and error to find the best response.

There have been some high-profile corporate winners – companies that support home working, online delivery and logistics providers, packaging firms, some pharmaceuticals. But Covid has highlighted economic and social inequalities, and added “health poverty” to the lexicon.

There have also been many losers, with almost entire industries being downgraded to junk. But default rates have been low, due to massive government support programs, and a wave of mergers and acquisitions as larger firms with strong balance sheets swallow their struggling competitors. Good news for investment banks, who along with insurance companies have weathered the crisis well.

This report shows the key credit and solvency trends that emerged in 2020 and provides some pointers towards what we can expect in 2021.

Download the latest whitepaper to read the full analysis:

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok