Poland’s credit standing is going down while Belgium’s rises. The divergence is mostly political. Poland’s economy is healthy and debts are low but the ruling populist party makes analysts nervous. Belgium’s many divisions mask a uniform commitment to fiscal restraint.

In the world of sovereign credit risk, politics can matter more than anything else. The diverging directions of Poland and Belgium are a good demonstration of this principle. In the latest CBC* data, Poland’s sovereign debt went down a notch. Belgium’s CBC rose by one notch two months ago.

In many ways, Poland remains a model of post-Communist economic development. In 1995, the International Monetary Fund calculates that Polish GDP per person was 23% of Spain’s, one of the poorer Western European countries. By 2015, the ratio was 43%, with 3.6% GDP growth expected this year in Poland.

The growth has not been supported by excessive government borrowing. On the contrary, the fiscal deficit has been steadily below 3% of GDP, and the ratio of government debt to GDP is a comfortingly low 52%. The ratings revision reflects a new attitude from the Law and Justice Party, which has been in power since late 2015. It has taken a strong populist line. The EU warned in June that a promised large increase of child benefits is likely to bring the deficit over the 3% line.

Less tangibly, analysts are nervous about the government’s nationalism and its apparent distaste for a politically neutral bureaucracy. Jarosław Kaczyński, the Polish party’s leader is not likely to find a sympathetic audience in Brussels if help is ever needed. This looks like a government whose response to bad economic news or political challenges could be increased deficit spending.

Across the continent, the Belgian economy basically rises and falls with the euro zone, and right now the European economy is doing a bit better. In the distant past, Belgian governments tried to paper over regional problems with big deficits, but those days are long over. The ratio of sovereign debt to GDP, fell from 136% in 1994 to 87% in 2007. It rose after the financial crisis, but has stabilised at 106%.

The current government continues the national commitment to low deficits. And after two years in power, even the country’s troubled politics look a bit more stable. For the foreseeable future, no Belgian government is likely to squander any unexpected growth dividend.

Still, if Belgium were less developed, its fractious politics and Flemish-French linguistic split would be concerning. But the civil service is competent, the political tensions are manageable, and no one wants to threaten the country’s close integration with the rest of Europe.

Brussels, Belgium gains from its warm relationship with Brussels, Europe.

Politics are particularly important for credit when times are perceived as tough. That’s the case now in the divided and economically stalled European Union, where governments will be tempted to reach for the chequebook. Poland, from the populist right, and Belgium, from the threatened centre, are good tests of the will to resist.

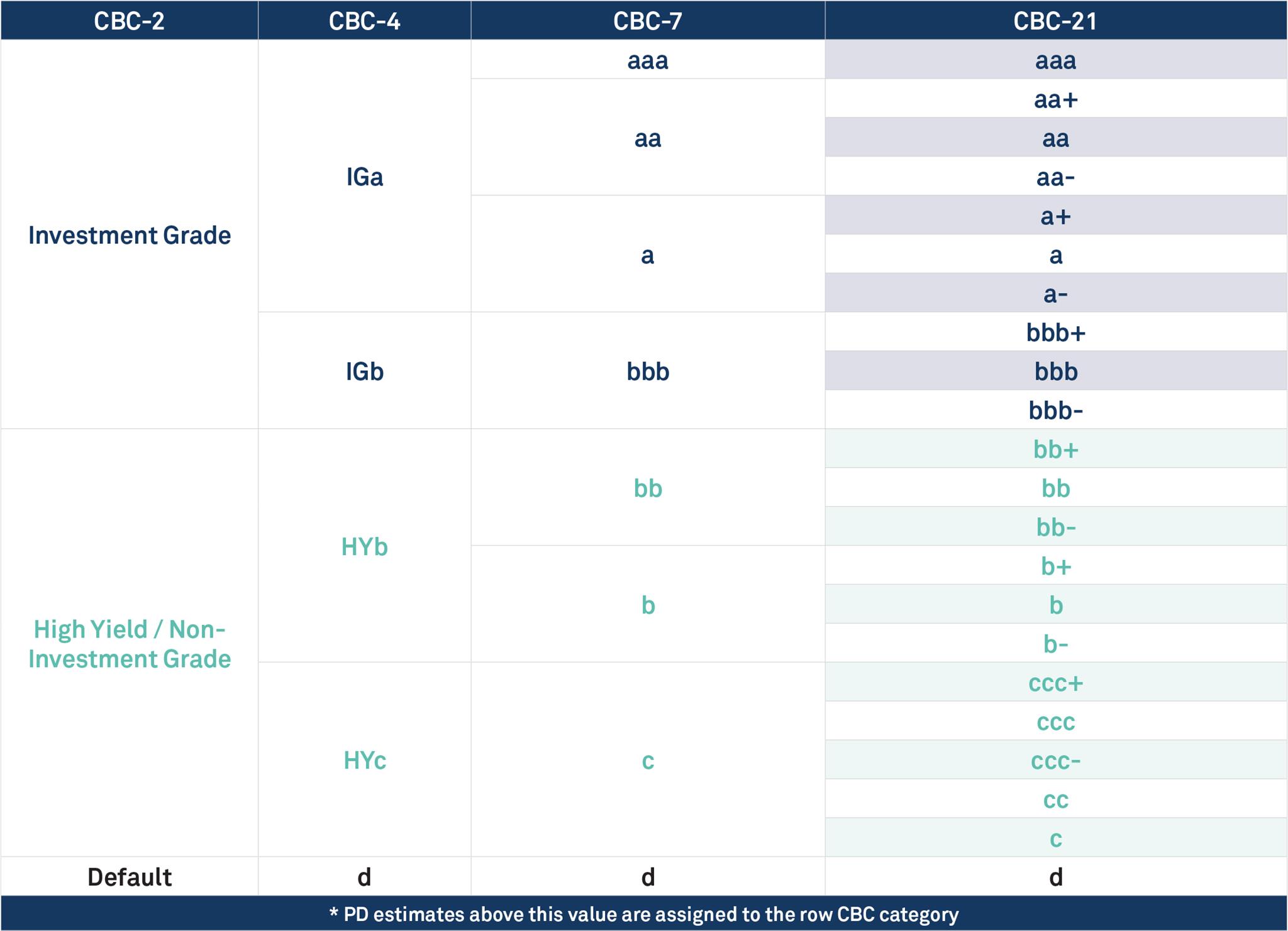

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of [bbb+] is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

{kind=link}