UK insurers hoping Brexit might signal a bonfire of regulations, particularly the onerous and complex requirements of the Solvency II directive, got a glimpse of what the future might hold at a seminar hosted by the London Business School this week. Sam Woods, deputy governor of the Bank of England and chief executive of the Prudential Regulation Authority (PRA), said that though, “some aspects of the [Solvency II] regime had been found wanting”, it was in “nobody’s best interests…to make wholesale changes.”

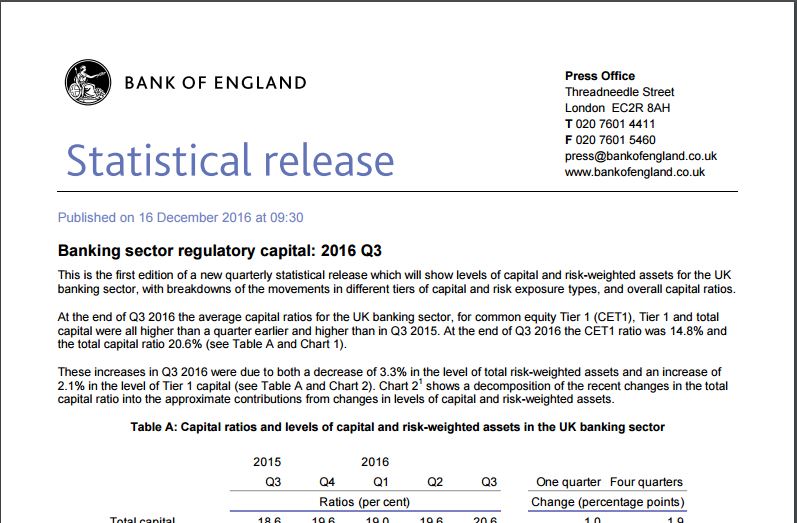

Woods stressed that the data reporting requirements of Solvency II could not be fudged. Both the frequency and volume of data were crucial to the PRA delivering its twin objectives of protecting policyholders and the soundness of the insurance industry. He mooted that the Bank of England may also seek to produce an insurance equivalent of the new quarterly Statistical Release for the banking sector, based on data it received from firms . The first release has been pencilled in for this autumn.

While emphasising the importance of frequent, high quality data, Woods also held out the possibility of a “series of tweaks and improvements” to regulation. One concern of UK life insurers has been the interpretation of the Matching Adjustment (MA), which gives a capital benefit if asset cashflows can be matched with liability cashflows. This is relatively straightforward to demonstrate for sovereign bonds and liquid credit, but less so for illiquid assets such as infrastructure debt and loans.

Woods said given a “completely free hand” he would alter the MA to allow a wider definition of fixed and predictable. He estimated that by interpreting the regime “intelligently” the PRA had already delivered a £59 billion reduction in capital requirements to the industry. However, he also noted that illiquid securities and loans required specific skills in structuring, valuation and risk management, which have not been traditional areas of expertise for insurers.

Woods was also keen to point out that the PRA had not gold plated Solvency II in relation to internal model approvals. He added that the quantitative indicators used by the PRA did not represent pass/ fail standards. He said: “Modelling credit risk is a complex business, subject to nuance and considerable expert judgement. Indeed, reasonable, knowledgeable experts might perfectly well disagree on some of the key assumptions.”

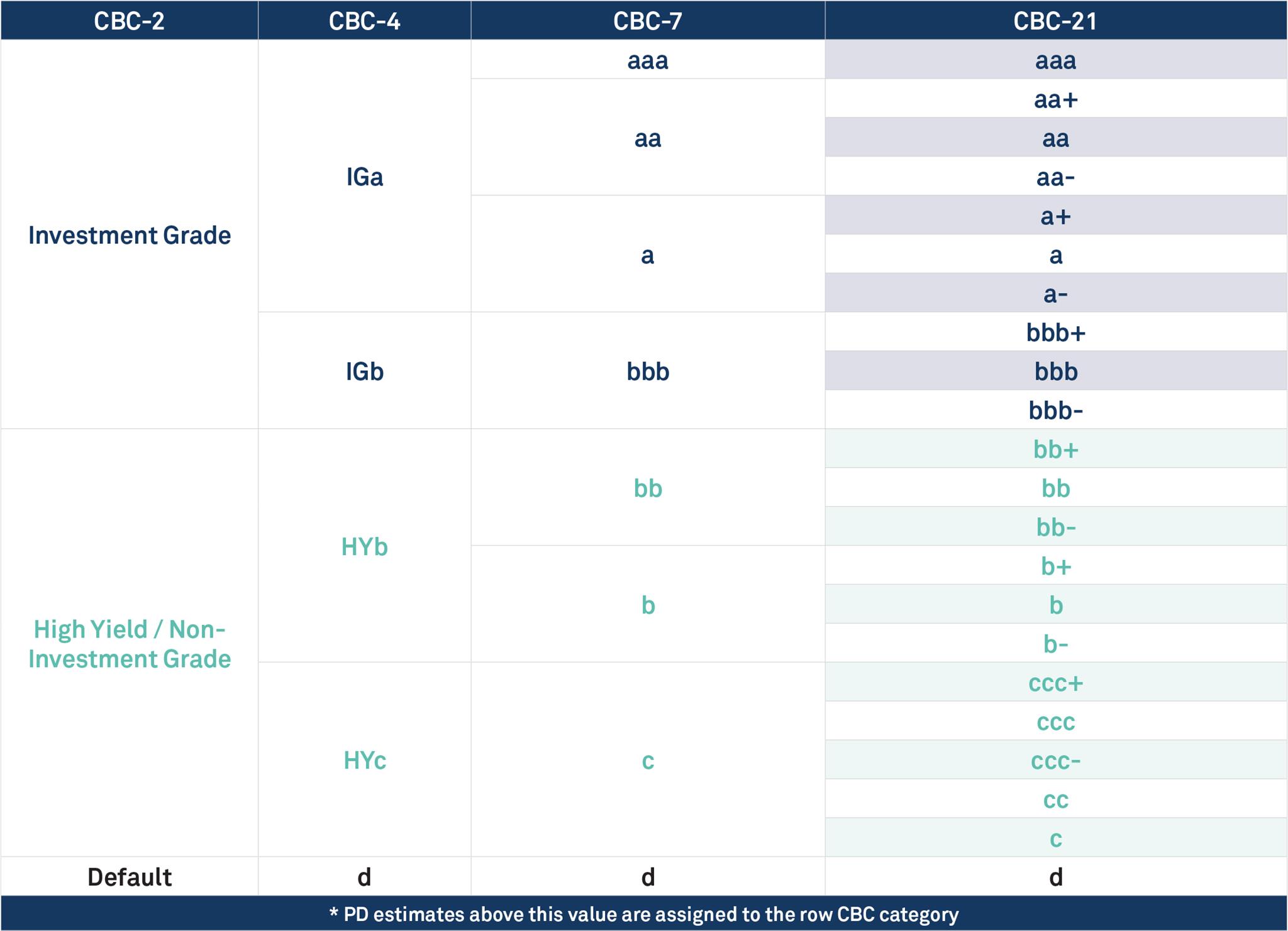

Credit Benchmark publish consensus credit views (CBCs*) for a growing number of obligors, and the majority of these are unrated. The dataset also supports a diverse set of credit transition matrices which can be used to isolate liquidity risk premiums. Contact us for more information.

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of bbb+ is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

Disclaimer: Credit Benchmark does not solicit any action based upon this report, which is not to be construed as an invitation to buy or sell any security or financial instrument. This report is not intended to provide personal investment advice and it does not take into account the investment objectives, financial situation and the particular needs of a particular person who may read this report.

Image Source: Bank of England Website

{kind=link}