Rating agency downgrades have hit unprecedented levels over the past few months, but the majority of the downgrades have been for companies that were already classed as high yield. Fallen Angels – companies that cross the boundary from Investment Grade to Junk – are still in a minority, as agencies (and their corporate clients) display an understandable reluctance to avoid the “BBB cliff”.

But consensus credit data shows that, in the opinion of their lenders, a growing number of companies are falling over the cliff edge, providing clues to likely future default rates.

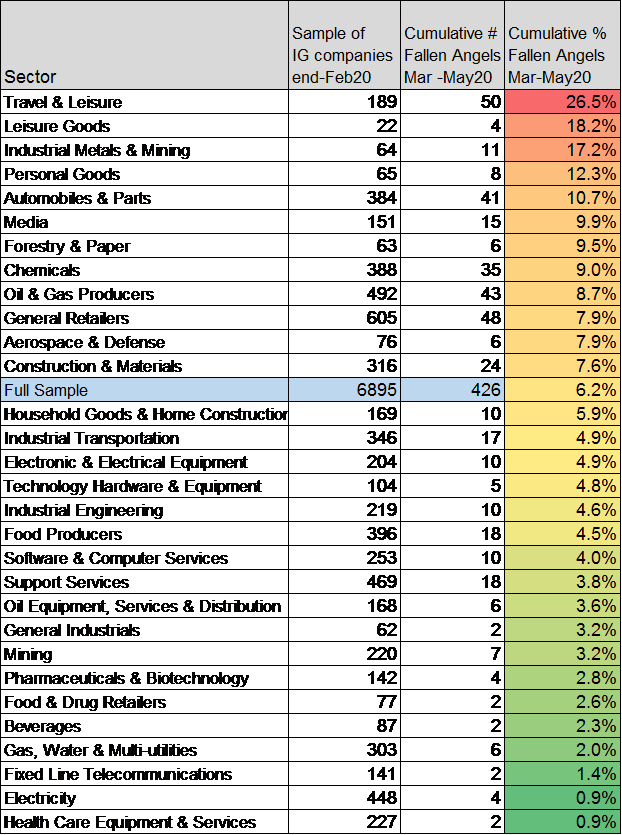

Figure 1 shows, for the full set of global sectors, the proportions of a sample of 6,895 companies that have migrated from Investment Grade to Non-Investment Grade in the past three months. In total, 426 companies (around 6%) have migrated to and remained in Sub-Investment Grade territory over this period.

More than a quarter of the Travel & Leisure sector sample has moved to non-Investment Grade over the past three months. The Leisure Goods sector rate is 18%, while Industrial Metals and Mining are running at 17%. Automobiles and Parts, Media and Forestry & Paper are all at about 10%.

Sectors with a significantly lower Fallen Angels rate than the overall sample rate of 6% include Food Producers, Pharmaceuticals & Biotechnology, various Utility sectors, and Health Care Equipment & Services. Oil Equipment, Services & Distribution is also below average, whereas most of the broader Oil sectors are already dominated by below Investment Grade companies.

Ed Altman has robustly estimated that up to a third of all corporate bonds in the BBB category could move to Junk status, and consensus credit data earlier this year seemed to corroborate that analysis.

It is worth noting that the consensus credit sample discussed here is based on issuers (rather than issues) and includes all Investment Grade companies, not only BBB. But the Fallen Angel rates shown here – which cover just three months of the COVID crisis – suggest that the transition rate for some sectors by the end of 2020 may be even higher than has so far been suggested.