The latest GDP numbers from the US show a blistering real growth rate of more than 4%, implying that the Trump tax cuts are having the desired effect across the US economy.

But as the equity results season gets into full swing, some of the technology giants have been suffering huge share price drops: Facebook and Twitter were down nearly 20% last week, and Netflix is down 15% from its June high. Amazon and Alphabet have so far ridden out the storm and saw their share prices rise following their recent results.

It is possible that the differences between Main Street and Silicon Valley are more nuanced than the simple labels suggest. Amazon is now a key part of the physical distribution chain while Alphabet (i.e. Google) is effectively an information distributor at the heart of the online economy.

But social media companies and streaming services are at the mercy of trend changes by fickle (mainly young) users – these companies may have been the prime movers in their spaces, but they have less protection from barriers to entry than the infrastructure stalwarts like Amazon and Alphabet.

Meanwhile, the traditional US economy is booming. Trade wars remain a moderate risk, but the US economy has a strong domestic focus; exports account for just 12.5% (Germany is at 46%). It will take time for corporate tax cuts and other fiscal boosts to pass through, so Main Street growth – especially in the industrial sector – is likely to be sustained.

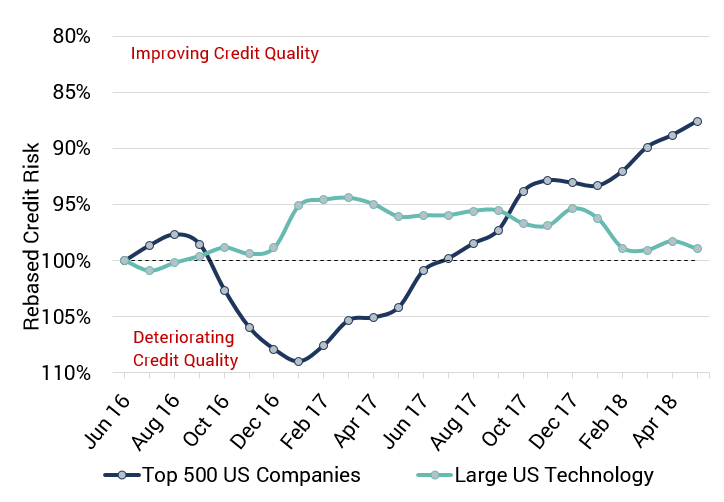

Looking at the chart below, it is clear that the credit risks for Main Street and Silicon Valley are behaving very differently. Towards the end of 2016, technology showed a slight improvement while the broader measure of the 500 largest US companies was steadily deteriorating. These trends began to reverse in early 2017; technology has now given up its gains, while the broader group has made a huge swing from a 10% deterioration to a 15% improvement.

Credit trends in technology seem to be reflecting the nuances described here. If US GDP growth continues at its current pace, some of the core technology companies are likely to share in the benefits; but some of the largest Silicon Valley companies may begin to see Main Street pull further ahead.