Regulators, auditors, and internal committees increasingly demand independent external validation for credit models. Traditional rating agencies provide established benchmarks for public companies and large bond issuers—but a significant portion of most institutional portfolios consists of entities outside their coverage.

For middle-market borrowers, private credit exposures, and fund counterparties, the question becomes: what independent sources exist at all? Three distinct methodologies serve different segments of the credit universe:

- Issuer-paid agencies covering public companies and large corporates

- Subscriber-paid agencies offering an alternative model with narrower coverage, and

- Consensus-based approaches aggregating views from banks with actual lending relationships across rated and unrated entities alike.

Each carries different conflict structures, regulatory acceptance levels, and coverage profiles. Understanding these differences determines which sources apply to which validation needs.

This article examines what makes an institutional credit ratings source independent, evaluates how each source performs against regulatory guidelines, and identifies where consensus data extends validation to exposures traditional agencies don’t cover.

What Makes Credit Ratings “Independent”? Three Models Compared

In credit risk management, independence requires that ratings data be free from structural conflicts that could bias the assessment. A rating source can be “third-party” without being independent. A vendor model is external but reflects algorithmic outputs rather than lender judgment. True independence requires structural separation from both the rated entity and the rating’s end users.

The three primary models available to institutional credit risk professionals each carry distinct conflict profiles:

| Model | Paid By | Primary Conflict | Unrated Coverage |

|---|---|---|---|

| Issuer-Paid (S&P / Moody’s / Fitch) | Rated entity | Commercial pressure for favorable ratings | Public companies and large corporates; ~10% of institutional portfolios |

| Subscriber-Paid (Egan-Jones) | Investors | Capital relief incentives | Narrower than issuer-paid; limited to entities investors request |

| Consensus (Credit Benchmark) | No payment relationship with rated entities | None structural | 120,000+ entities across 160 countries; 90%+ unrated by traditional agencies |

Issuer-Paid Agencies (S&P, Moody’s, Fitch)

Traditional agencies have provided credit opinions for over a century, establishing the rating scales and methodologies that define credit markets.

For public companies and large bond issuers, agency ratings offer deep analytical coverage, published methodologies, and broad market acceptance.

The model carries an inherent tension: rated entities fund their own coverage through fees typically ranging from $50,000 to $300,000+ annually. Agencies compete for issuer business, creating commercial pressure that drew regulatory scrutiny after inflated ratings on mortgage-backed securities contributed to the 2008 financial crisis. Post-crisis reforms improved practices, but the underlying economics remain unchanged.

Coverage concentrates where the economics work—public companies and large corporations whose bond issuance justifies the expense. Middle-market borrowers, private companies, and fund structures fall outside this coverage, not because agencies assess them poorly, but because the issuer-pays model doesn’t extend to entities that don’t issue public debt.

Update cycles run quarterly or annually, appropriate for through-the-cycle stability but less suited to continuous portfolio monitoring.

Subscriber-Paid Agencies (Egan-Jones)

The investor-pays model emerged as a proposed solution to issuer-pays conflicts. If investors fund the ratings, agencies have no commercial relationship with rated entities. Egan-Jones, the most prominent subscriber-paid agency, marketed this independence advantage after 2008.

Research has identified a different concern. A 2023 study published in the Journal of Accounting and Economics found that Egan-Jones issues more optimistically biased ratings, less timely downgrades, and less accurate ratings for bonds extensively held by its institutional subscribers.

The researchers concluded that subscriber-paid agencies don’t resolve conflicts of interest but rather alter their nature. The SEC also penalized Egan-Jones for misrepresenting its track record during the financial crisis.

Consensus-Based Approaches (Credit Benchmark)

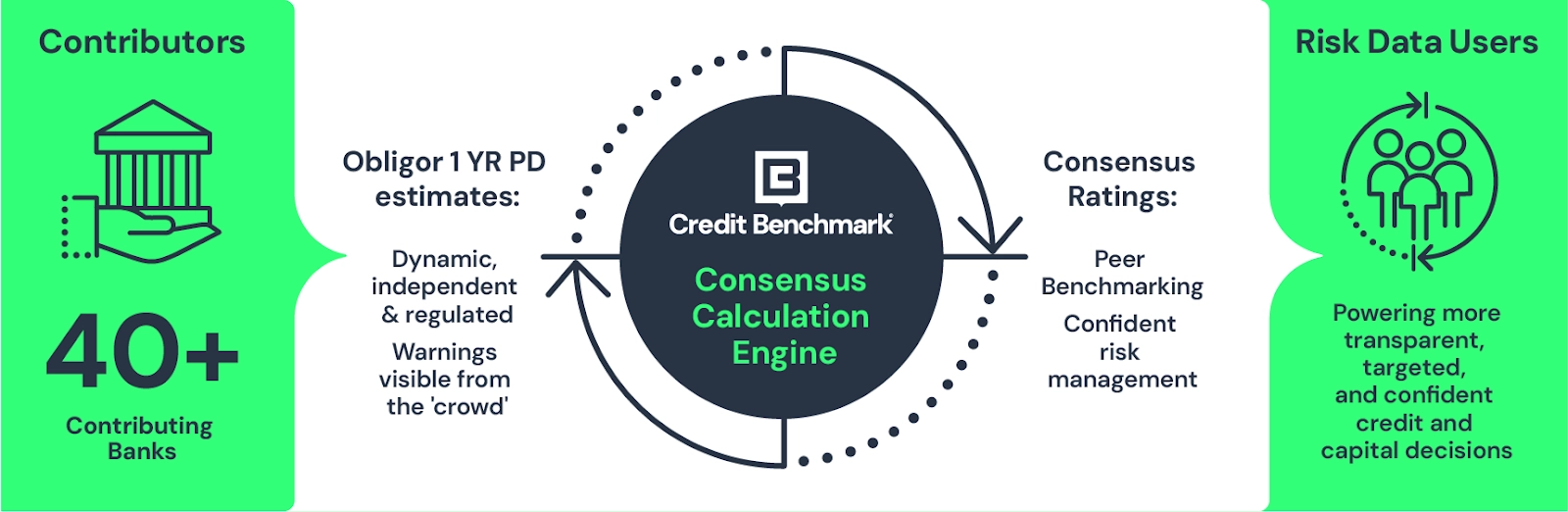

Consensus methodology aggregates anonymized internal credit views from banks with actual lending exposure to rated entities. Banks contribute their internal Probability of Default and Loss Given Default estimates—the same assessments they use for regulatory capital calculations, loan pricing, and portfolio management—in exchange for access to the aggregated consensus across all contributors.

No payment relationship exists between rated entities and the rating process. Contributing banks share views developed for Basel compliance, subject to supervisory examination by their primary regulators. The consensus reflects how institutions with capital at risk assess creditworthiness based on actual lending relationships.

Coverage extends to segments traditional agencies don’t reach: middle-market borrowers, private credit portfolio companies, fund structures, and unrated subsidiaries.

For entities with agency coverage, consensus data provides a complementary benchmark reflecting lender perspectives rather than issuer-funded opinions. Weekly updates reflect how contributing banks continuously adjust internal ratings for active portfolio management—a different rhythm than agencies’ through-the-cycle approach, suited to different use cases.

Why Consensus Ratings Offer Structural Independence

Understanding why consensus methodology achieves independence requires examining the mechanics of data collection, aggregation, and quality control.

Inputs Come From Regulator-Validated Models

Over 40 global banks (half of which are Global Systemically Important Banks) contribute their internal credit assessments to Credit Benchmark. The specific inputs are one-year, forward-looking Probability of Default and senior unsecured Loss Given Default estimates.

These are the same assessments banks use for regulatory capital calculations, loan pricing, and portfolio management—developed for internal risk decisions, then contributed to the consensus.

Contributing banks submit views on all their corporate clients under contractual obligation, mitigating concerns about selective data submission. A bank cannot cherry-pick which entities to include based on whether the consensus would favor their positions.

No Commercial Incentive to Inflate

Banks operating under Basel IRB frameworks already maintain internal rating models as a regulatory requirement. The infrastructure exists; contributing to the consensus adds a marginal operational burden while providing access to anonymized peer views across 120,000+ entities.

The value exchange is reciprocal benchmarking, not a commercial transaction. Contributing banks gain visibility into how 40+ institutions assess the same counterparties—information that supports their own model calibration, identifies outlier assessments requiring review, and strengthens regulatory exam readiness.

The cost is information sharing; the benefit is distributed market intelligence unavailable through any other channel.

No Single Bank Controls the Output

Credit Benchmark requires multiple observations per entity before publishing—typically 3-5 contributing banks—ensuring statistical reliability while protecting individual contributor confidentiality. No single bank’s view dominates the consensus; the methodology aggregates across all contributors to produce a market-weighted assessment.

Weekly publication cycles reflect how contributing banks continuously adjust internal ratings for active portfolio management. When multiple banks independently downgrade the same counterparty, the consensus captures that signal within days. Quarterly agency review cycles, by contrast, may not reflect the same deterioration for months.

Distributed Supervisory Oversight

The contributing banks’ internal rating models undergo supervisory examination by the Federal Reserve, ECB, PRA, and other primary regulators as part of ongoing Basel compliance. When consensus data reflects the aggregated output of these examined models, it carries validation credibility that proprietary vendor algorithms cannot match.

A 2024 study published in the Review of Accounting Studies examined Credit Benchmark’s consensus ratings against traditional agency ratings and found that consensus data improves default prediction accuracy.

The research attributed this to the methodology’s foundation in actual lending relationships—contributing banks assess counterparties they hold exposure to, creating accuracy incentives that neither issuer-pays nor subscriber-pays models replicate.

Case Study: A $150B U.S. Bank Validates Internal Models for SNC Exams Through Consensus Data

One of the largest U.S. banks, with approximately $150B in total assets, needed peer-driven insights to understand where its internal credit views stood relative to other institutions.

The Chief Credit Officer faced a specific challenge: without external validation, the bank couldn’t determine whether its credit assessments were too conservative, too aggressive, or properly calibrated—particularly for entities lacking traditional ratings.

The bank embedded consensus data directly into its credit models, using it to recalibrate PDs and LGDs while leveraging peer insights for Shared National Credit exam preparation.

The results included improved model accuracy through pressure-testing against market consensus, stronger regulatory positioning through peer validation, and confident decisions on unrated entities where traditional validation methods weren’t available.

“Credit Benchmark has given us a clearer lens into how our peers assess credit risk, especially for unrated names. The ability to benchmark our internal views has significantly increased our confidence in risk decisions, and it’s directly informed model recalibration efforts.”

– Chief Credit Officer

How Each Model Performs Against Regulatory Requirements

SR 11-7’s validation framework establishes three elements: conceptual soundness, ongoing monitoring (including benchmarking), and outcomes analysis. Each credit data model serves different validation needs depending on portfolio composition and coverage requirements.

Issuer-Paid Agencies

For rated entities, traditional agency ratings provide established benchmarks with published methodologies and long performance track records. Regulators accept agency ratings as external reference points for the entities they cover.

Two limitations affect comprehensive validation. First, the conflict structure raises questions about independence for some supervisory purposes—examiners may probe whether issuer-funded ratings constitute the “independent alternative” SR 11-7 contemplates.

Second, coverage gaps prevent portfolio-wide benchmarking. Agency ratings exist for approximately 10% of typical institutional portfolios; validation relying solely on agency comparisons leaves the majority of exposures without external reference points.

For portfolios concentrated in rated public companies and large corporates, agency data serves validation requirements well. For portfolios with significant middle-market or private credit exposure, additional sources become necessary.

Subscriber-Paid Agencies

Investor-pays models address the issuer conflict but introduce questions about capital relief incentives. Coverage is typically narrower than that of issuer-paid agencies, and regulatory acceptance remains inconsistent across jurisdictions. Institutions may find subscriber-paid ratings useful as supplementary benchmarks but face limitations for comprehensive validation.

Consensus-Based Approaches

Consensus methodology addresses validation requirements for portfolio segments that traditional agencies don’t cover:

- For conceptual soundness, the underlying inputs are PD and LGD estimates from Basel IRB models—methodologies already examined and approved by contributing banks’ primary regulators.

- For ongoing monitoring, weekly updates enable continuous benchmarking. Deterioration surfaces as contributing banks adjust internal ratings, providing forward-looking calibration checks between annual backtesting cycles.

- For independence, no payment relationship exists between rated entities and the consensus.

Coverage reaches 120,000+ entities, with 90%+ unrated by traditional agencies. For the middle-market borrowers, private credit exposures, and fund counterparties comprising the majority of institutional lending books, consensus data provides external validation where agency benchmarks don’t exist.

In practice, financial institutions use agency ratings for validation of rated exposures, consensus data for validation of unrated exposures, and both together for comprehensive portfolio coverage.

Where Independent Ratings Data Solves Validation Problems Traditional Sources Can’t

Traditional agency ratings serve their core market well—public companies and large bond issuers benefit from deep analytical coverage and established methodologies. Consensus data extends validation to portfolio segments where agency coverage doesn’t exist.

IFRS 9/CECL Model Validation

Lifetime expected credit loss calculations require forward-looking inputs across the full portfolio, not just rated exposures. IFRS 9’s staging framework demands migration probabilities across credit categories—the likelihood that a Stage 1 exposure deteriorates to Stage 2 or Stage 3 over the life of the instrument.

For rated entities, agency transition matrices provide established benchmarks. For portfolio exposures lacking agency coverage, credit rating transition matrices derived from weekly rating movements across 40+ contributing banks extend validation to middle-market and private credit exposures. Stage 2 trigger calibration benefits from both sources: agency data for rated names, consensus data for unrated ones.

Unrated Entity Benchmarking

A bank assessing a $200M private manufacturing company or mid-sized healthcare borrower has no S&P, Moody’s, or Fitch rating to reference—not because agencies would assess it poorly, but because the issuer-pays model doesn’t extend to entities that don’t issue public debt.

Consensus data answers this directly. If 12 contributing banks with lending relationships to that same entity collectively view it as “BB+”, the internal assessment has an external benchmark that otherwise wouldn’t exist. This peer comparison serves the same validation function that agency ratings serve for public companies, applied to the unrated universe.

State Street, a global financial services provider managing counterparty relationships across thousands of entities, faced this gap. When evaluating their internal ratings against market consensus for unrated counterparties, they found no comparable solution. In their own words, “No one else does what you do. Credit Benchmark data makes my job easier.”

Counterparty Credit Risk

CCPs, prime brokers, and securities finance desks manage exposure to counterparties that don’t carry agency ratings—hedge funds, proprietary trading firms, and buy-side clients whose business models don’t include paying for public ratings.

The Canadian Derivatives Clearing Corporation monitors 30+ clearing members using weekly consensus updates. For members with agency ratings, CDCC has multiple external reference points. For unrated members, consensus data provides the only independent benchmark available—extending visibility across the full membership rather than just the rated portion.

Evaluating Independence When Selecting Credit Data Providers

Procurement teams and risk officers evaluating external credit data providers can apply a consistent framework to assess genuine independence versus shifted conflicts.

Who pays? Issuer-pays models create commercial relationships between agencies and rated entities. Subscriber-pays models shift the relationship to investors who benefit from favorable ratings on their holdings. Consensus models have no payment relationship with rated entities—banks contribute internal views developed for their own risk management.

Do contributors have actual exposure? Vendor algorithms process financial statements and market data without lending relationships. Agency analysts evaluate issuers who pay for coverage. Contributing banks in a consensus model hold actual credit exposure to the entities they assess—capital at risk that disciplines the accuracy of their internal ratings.

Are the underlying models regulator-validated? Proprietary vendor models undergo whatever internal validation the vendor applies. Agency methodologies face periodic regulatory review but operate independently of banking supervision. Consensus contributors operate under Basel IRB frameworks subject to ongoing examination by the Fed, ECB, PRA, and other primary regulators—distributed validation across 40+ supervised institutions.

What’s the actual coverage of unrated entities? Traditional agencies cover approximately 10–15% of institutional portfolios due to issuer-pays economics. Subscriber-paid agencies offer narrower coverage still. Consensus data reaches 120,000+ entities with 90%+ lacking traditional agency ratings—the middle-market borrowers, private credit exposures, and fund counterparties where validation gaps are most acute.

Moving to Truly Independent Credit Validation

Independent credit validation requires matching data sources to portfolio composition. Traditional agencies provide established benchmarks for rated public companies and large corporates—the entities they’ve covered for decades. Consensus data extends validation to the middle-market borrowers, private credit exposures, and fund counterparties that comprise the majority of institutional lending portfolios.

The distinction is which source covers which exposures. For model validation teams defending PD calibration, Chief Credit Officers benchmarking internal views, and procurement specialists evaluating RFP requirements for comprehensive coverage, consensus data from 40+ banks with actual lending exposure delivers the independent validation that neither issuer-paid nor subscriber-paid sources can provide.

Request a portfolio coverage analysis to see how consensus data validates your unrated exposures.