Standard credit risk analysis industry practices work great for public counterparties, with a rating to anchor to, financials to feed the model, and a market price to check it against, but fail for private unrated counterparties, which lack those.

An internal model still returns a PD and a CCF, but there’s no external opinion to corroborate it before a credit committee, an auditor, or a regulator.

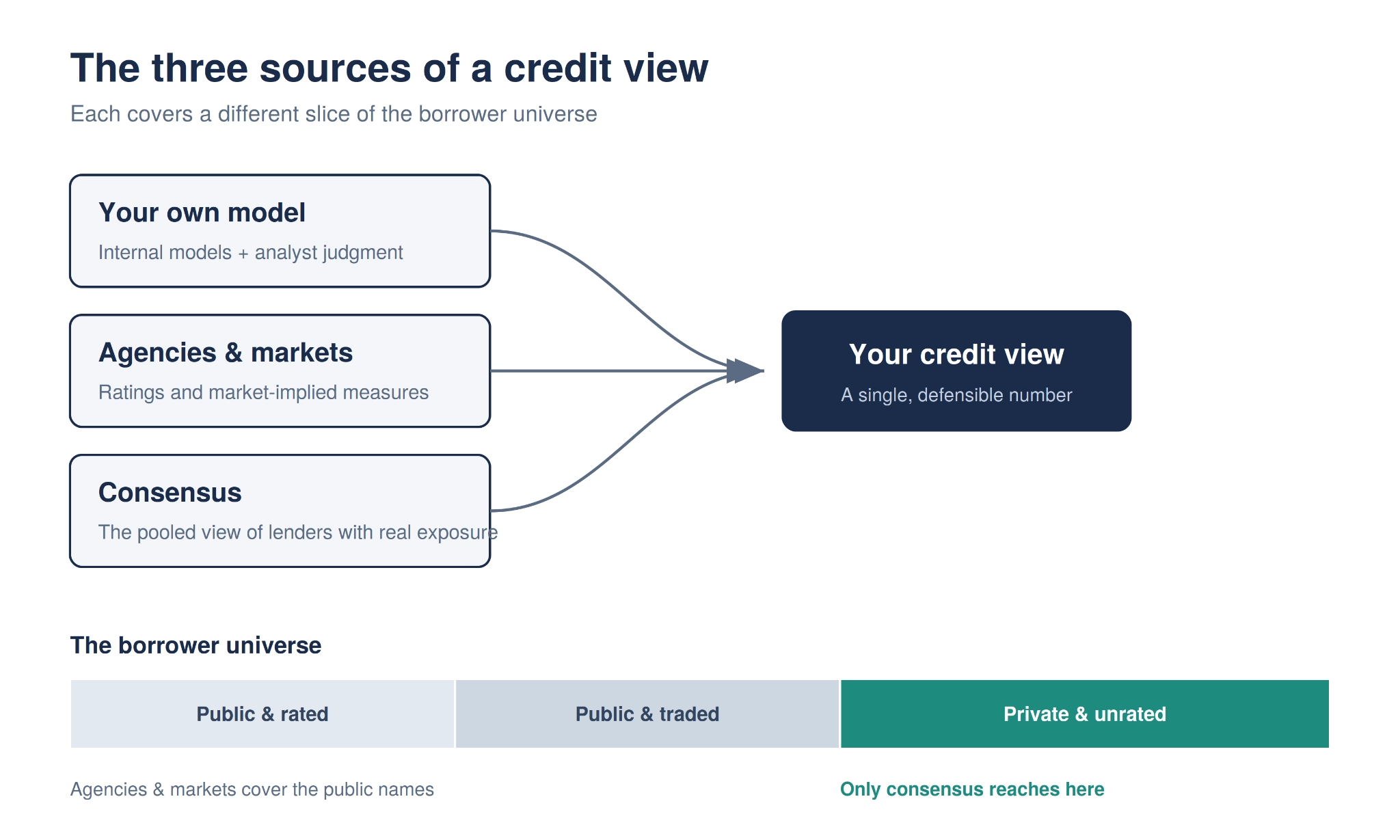

In a market where unrated entities account for a large and growing share of most books, that gap is too big to ignore. Strong risk teams close it by triangulating across three sources of a credit view:

- The overarching view, through internal models and analyst judgment.

- The view generated from designated outside assessors: the rating agencies and market-implied measures.

- The view of the crowd that actually carries the exposure

This article walks through how each source works, where each one falls short, and how leading institutions combine them, with a sharp focus on the counterparty, which none of them covers well.

Input 1: Internal models and analyst judgment

The overwhelming majority of the world’s borrowers carry no external rating, so a credit view on them has to be built in-house. For banks, the Basel Internal Ratings-Based (IRB) approach permits supervised institutions to use their own estimates of the core risk parameters to calculate regulatory capital. Buy-side and insurance risk teams build the same models to mark positions, set limits, and satisfy their own supervisors.

Defining default and the objective

Before any parameter is estimated, two things have to be fixed: what counts as default, and what the model is for.

How “default” is defined matters, as it affects everything downstream. Institutions can lean on both IFRS 9 and the Basel capital rules: the latter defines default as a borrower being 90+ days past due or unlikely to pay, while IFRS 9 lets banks use their existing internal definitions, with the 90-day rule as a fallback. Every team in the bank needs to use the same definition, thresholds, cure periods, and scope so its outputs are not misleading.

The objective then drives the method used to estimate the probability of default (PD). Regulatory capital needs a one-year PD, smoothed (through-the-cycle) to reflect a borrower’s average risk across good years and bad years. IFRS 9 needs a forward-looking PD (point-in-time) and a lifetime PD for weaker loans covering their full remaining term.

Estimating probability of default (PD)

PD gets the most attention because it’s both the hardest parameter to estimate and the one with the biggest impact on the final loss estimate. The best model choice depends on the portfolio, the data in hand, and how the PD will be used.

Statistical scorecards are the default choice. They are usually built with logistic regression, partly because its output naturally falls between 0 and 1. The model is fed a history of borrowers and their outcomes, from which it learns which financial and behavioral traits tend to precede default and converts that into a probability score. It’s used for large retail books, SME portfolios, and mid-corporate lending when sufficient data is available. On large, data-rich portfolios with sufficient defaults to train on, machine-learning methods are increasingly used in the same role.

This is the core of corporate credit analysis at scale. However, machine-learning methods are increasingly used on large, data-rich portfolios where sufficient defaults are available to train them reliably.

Structural (market-based) models are used for large, publicly traded borrowers. The Merton model treats a firm’s equity as an option on its assets and uses the level and volatility of the share price to estimate distance to default. A related version reads default risk straight from the firm’s CDS spread. These react quickly to new information because they’re built on continuously updated prices, but only work where a market price exists, limiting them to the largest public names.

Reduced-form (hazard-rate) models are the standard tool for pricing and for building PD term structures across multiple horizons. They model how the intensity of default risk changes over time and calibrate that to market spreads.

Expert judgment takes over where the data runs out, typically in low-default portfolios such as investment-grade corporates, banks, or sovereigns, where too few historical defaults exist to fit a statistical model. In practice, it rarely stands alone; rather, a scorecard produces a base score, and an analyst adjusts it for factors the data can’t capture.

Estimating Loss given default (LGD)

LGD is driven by recovery history and largely shaped by structural factors: the collateral backing the exposure and where the financial institution sits in the capital structure. As such, a senior secured claim against liquid collateral recovers far more than an unsecured one.

There are two ways to measure it. Workout LGD tracks the recovery process to its end, sums the cash actually collected, and discounts it to present value. Market LGD reads recovery straight off the price at which the defaulted loan or bond still trades. But for regulatory capital, downturn LGD takes priority to reflect the weak-recovery, high-default environment seen during periods of economic stress, rather than a benign average.

Estimating exposure at default (EAD)

For a fully drawn term loan, EAD is essentially the outstanding balance. It gets harder for facilities with undrawn commitments, such as credit lines, where the current balance understates the real exposure, as borrowers approaching default tend to draw down whatever credit remains available. Standard practice adds the drawn amount to a modeled fraction of the undrawn limit (credit conversion factor or CCF). However, the CCF is difficult to model since it’s a forecast of unpredictable behaviour.

Rolling up to loss and capital

Multiplying the three values gives expected loss, priced into the deal upfront. However, to accommodate unexpected losses, the IRB framework expects institutions to hold capital sized to the tail of the loss distribution. That’s why supervisors focus on capital rather than expected loss. And it’s why accurate PD, LGD, and EAD estimates matter so much, as any error in those numbers directly affects how much capital the bank is required to hold.

Validation and governance of internal models

Model risk management standards require that internal models be validated both at build and on an ongoing basis. They are to be tested for conceptual soundness, stress tested, monitored for performance, and benchmarked against external reference points. One problem makes this genuinely hard: low-default portfolios offer too few defaults to validate a PD against outcomes with any statistical confidence, and validation depends on having an external source to check the view against. For a large and growing part of the book, that external reference simply doesn’t exist. So an internal model, however rigorously built, remains an isolated opinion. That limitation is precisely why institutions reach for the second source.

Input 2: Agency Ratings and Market-Implied Measures

The second source is the credit view of rating agencies, which assess creditworthiness through analysis, and of financial markets, which assess it through prices. Neither competes with an internal model; their output often feeds internal models as an input. But both share the same weakness in covering private, unrated borrowers.

Agency ratings

Agency ratings are consistent and comparable across issuers, industries, and time. A single-A rating is meant to signal the same level of risk whether it’s given to a utility company or a manufacturer, this year or five years ago. That consistency is built on decades of default data and deep analytical resources. However, they’re plagued by three limitations:

- Coverage. Agencies rate only large issuers that can afford it and that borrow in public markets. Most borrowers are never rated at all.

- Speed. Because ratings are reviewed periodically, they lag behind the borrower’s actual condition. They’re also designed to reflect long-term average risk rather than current conditions.

- Conflict of interest. Under the standard “issuer-pays” model, the company being rated pays for the rating. This has drawn particular scrutiny in insurance markets, where the NAIC is reviewing internal and private credit ratings seen as overly optimistic in securing lower capital charges. And there have been widespread concerns about bias in their assessments.

None of this means agency ratings are wrong. It only drives home the importance of supplementing from another source.

Market-implied measures

The second outside source is the market itself. Where a borrower has a tradeable instrument, a credit view can be read from its price:

- CDS-implied PD: derived from the cost of buying insurance against that borrower’s default.

- Equity-based models (like the Merton model): derived from the level and volatility of the stock price.

- Vendor scores: pre-packaged probabilities built by combining these signals.

Unlike agency ratings, market-implied measures react instantly to new information, often well before a new agency rating or financial statement appears. For large, publicly traded companies, this makes them a useful real-time check against both agency ratings and an internal model. But their reliance on publicly available data excludes private companies, direct lending funds, family offices, and most mid-market borrowers.

Input 3: Consensus from institutions with real exposure

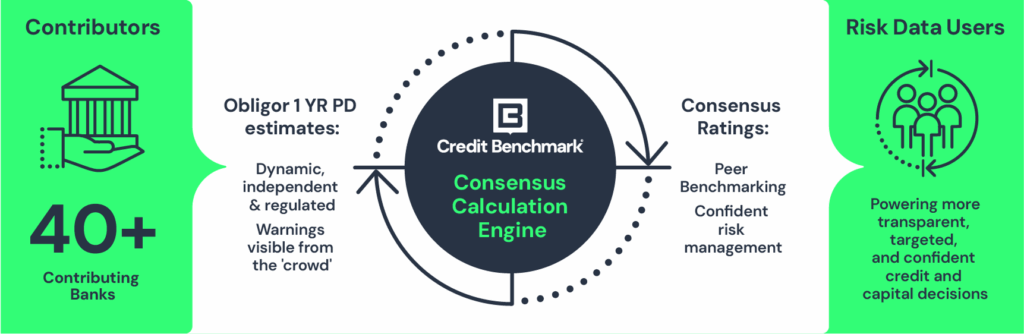

Many banks run their own internal credit models, producing regulated, analyst-reviewed PDs for each borrower they lend to. Typically, internal credit models, which are regulated, analyst-reviewed PDs for each borrower a bank lends to, stay hidden from other institutions. A consensus data provider collects these individual assessments from a network of participating banks, anonymizes the sources, and publishes an average.

Since consensus is built from internal models, a fair question is how it differs. An internal model gives no way to know whether a view aligns with the broader market; conversely, consensus provides an external benchmark drawn from the actual lenders holding the risk. Two things set consensus apart from agency ratings:

- Speed. Banks submit updates throughout the month, and the consensus average refreshes weekly, updating in near real-time. So it updates in near real time as banks change their views.

- Reach. Consensus doesn’t require a borrower to commission a rating or to have a traded price, so it can cover borrowers agencies and markets never reach.

A fair question to ask is whether an average based on many banks’ internal ratings is as discriminating as a rating agency’s carefully researched opinion. The evidence suggests it does. Over roughly a decade, consensus ratings have separated stronger borrowers from weaker ones about as well as a major agency, measured by discriminatory power (Gini), across a larger universe of entities, including unrated ones.

Assessing Unrated Counterparties

Private, unrated borrowers are now a major part of most portfolios. Private credit has grown into a market worth more than $2 trillion in assets, and PwC projects it could reach $3.4 trillion by 2030. The borrowers driving that growth (direct-lending funds, middle-market companies, private equity portfolio companies, and fund counterparties) almost never have a public credit rating.

This growth is happening at the same time the sector is showing real stress. Fitch reported a 5.8% default rate for US private credit in the 12 months through January 2026, the highest on record. In May 2026, the Financial Stability Board stated that private credit borrowers typically have no public rating, which makes it hard to monitor risk across the market, and they tend to carry lower credit quality and higher leverage than comparable borrowers who can be observed.

This is why consensus data is not a nice-to-have; rather, it is often the only external reference available for unrated entities. It only needs enough other lenders to also have exposure to that borrower. For private credit funds, mid-market companies, and fund counterparties, that’s usually true: many private borrowers have multiple lending relationships across banks. Their pooled, anonymized view provides the external check that agencies and markets can’t.

Consensus data doesn’t replace internal models or credit analysts. In fact, each source has strengths and limitations, which is why leading institutions increasingly use them together. The point of describing them separately was to show that each one fails in a different place, which is exactly why it’s a credit risk management best practice to use all three together:

- An internal model is the foundation. It’s the only source that can be controlled; it covers every borrower in the book, and regulators require financial institutions to own it.

- Agencies and market prices refine it for large, public, actively traded borrowers, giving a ready-made external check.

- Consensus data covers private, unrated borrowers, providing an external reference.

Credit Benchmark is a proven consensus data provider with years of experience covering the entities that rating agencies and internal models lack visibility on. It uses the internal credit views of a network of contributing banks and other financial institutions to produce anonymized consensus figures (PD, credit categories, and rating migration) for the specific borrowers those institutions actually lend to.

The dataset spans more than 125,000 borrowers, roughly 90% of which carry no traditional agency rating, which are exactly the entities agencies and markets miss. And because the underlying views come from institutions with real lending exposure independent of the issuer-pays model, it avoids the issuer-pays conflict. Plus, because it’s pooled from many contributors, no single institution’s view drives the number.

On quality, Credit Benchmark’s own data show performance comparable to the major agencies. Between July 2015 and June 2025, its consensus ratings averaged a one-year Gini of 0.88 against 0.91 for S&P Global Ratings, across a universe roughly five times broader, indicating comparable quality with materially greater coverage.

Credit Benchmark doesn’t replace your internal models or the rating agencies; it’s the third source, built specifically to cover the segment the other two were never designed to reach, which is exactly how State Street and Canadian Derivatives Clearing Corporation (CDCC) use it.

Case Study: State Street’s Front-Office

State Street’s Front-Office Risk team wanted to see how their internal ratings compared with the broader market, and struggled to justify rating changes to Enterprise Risk Management, especially for newer exposures with no external reference point. Consensus data gave them that missing benchmark, making it easier to challenge internal ratings and open risk-based conversations across the bank.

As Eliott Bryson puts it, “No one else does what you do. Credit Benchmark data makes my job easier.”

Case Study: The Canadian Derivatives Clearing Corporation (CDCC)

The CDCC faces the same problem at a greater scale. As a central counterparty, it must continuously assess the creditworthiness of more than 30 clearing members, many of them private entities or subsidiaries without a public rating, while balancing fair market access against sound risk monitoring. Consensus data strengthens its assessment of those members, with the most value coming precisely from the private, unrated entities that traditional agencies don’t cover.

As Vladimir Levtsun, Acting Director of Financial Resilience Risk, notes:

“Credit Benchmark’s data has contributed to directly strengthening our ability to manage counterparty risk and enhance internal reporting, leading to more confident, proactive risk decisions.”

For most institutions, the practical starting point is a coverage check, which includes identifying which counterparties in the book currently have no external credit signal at all, and therefore which ratings, limits, and provisions are running today without an outside reference behind them.

Book a demo to see how consensus PD data can close the gap in your portfolio, validate your PD assumptions and strengthen capital efficiency.