The final Basel III reforms are no longer a future regulatory shift. For many banks, its effects are already showing up in lending decisions, model governance reviews, and portfolio construction discussions that would have looked very different two years ago.

Implementation is unfolding unevenly, and the divergence between jurisdictions goes well beyond timing:

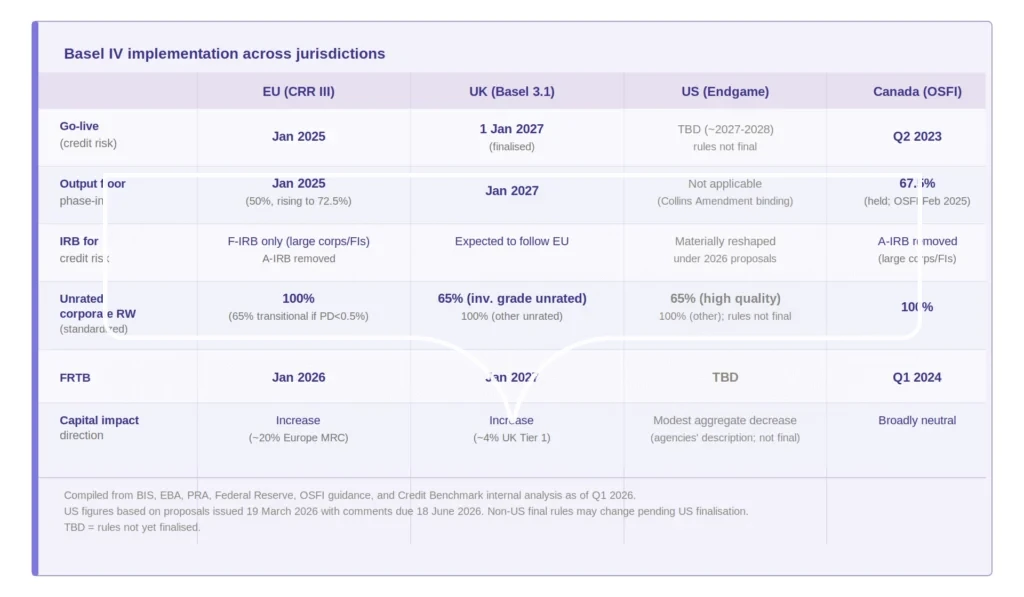

- Canada completed most requirements by early 2024.

- The EU went live with CRR III on January 1, 2025.

- The UK PRA finalized Basel 3.1 rules in January 2026, with implementation effective 1 January 2027.

- US agencies issued new capital proposals on 19 March 2026, with comments due 18 June 2026.

In the US, the 2026 proposals would materially reshape and simplify the capital framework for large banks, but the rules are not final and should not yet be considered settled.

The US and non-US frameworks are currently diverging in important respects, with the US framework still under proposal. European and UK banks face an output floor that constrains IRB benefits and increases capital requirements. US banks face the opposite: the agencies describe the March 2026 proposals as producing a modest aggregate decrease in capital requirements for large banks and a moderate decrease for smaller banks. Non-US final rules may still change pending what the US ultimately adopts.

The consequences cut across lending pricing, model validation, and portfolio construction, and they differ depending on where a bank’s exposures are booked.

How the Output Floor Reshapes Capital Allocation

The output floor is the mechanism by which Basel IV constrains the benefits of internal models at the portfolio level. It applies in the EU (live since January 2025), the UK (expected January 2027), and most non-US jurisdictions.

Under the current US proposals, the output floor as structured in the EU and UK framework does not apply in the same form. The Collins Amendment already makes standardized capital binding for US banks, and the 2026 proposals continue in that direction.

For EU and UK banks, two things matter most: the arithmetic of the floor itself, and how IRB constraints compound its impact on the exposures where internal models historically delivered the largest capital advantage.

The Capital Math Under the New Floor

Once fully phased in by 2030, the output floor prevents internally calculated capital requirements from falling below 72.5% of standardized levels. The phase-in starts at 50% in 2025 and escalates annually, capping the maximum capital benefit from internal models at 27.5% below the standardized approach.

The arithmetic hits hardest on portfolios that have historically benefited most from IRB precision.

Consider a bank whose IRB models risk-weight mid-market corporate exposures at 40-60%, based on granular PD and LGD estimates built over years of lending history. Those same exposures now attract a floor tied to the standardized 100% risk weight for unrated corporates.

Capital consumption on that book can effectively double without any change in the credit quality of a single borrower. This 100% weight, therefore, penalizes low-risk lending. Recognizing this, the EU’s CRR III includes a transitional provision that assigns a 65% risk weight to unrated corporates when a bank’s internal PD estimate is below 0.5%. However, the provision comes with constraints:

- It applies only where a bank can produce documented PD evidence from validated models, which most institutions cannot yet do at scale for unrated exposures.

- It is transitional, phasing out as the broader framework matures.

- The UK has introduced targeted measures for unrated corporates under its Basel 3.1 package, so the divergence is narrower than a simple ‘EU only’ framing would suggest..

EU banks that can produce validated external PD evidence hold a near-term capital efficiency advantage. That window is not permanent, and it narrows as the transition period runs down.

Where IRB Constraints Hit Hardest

Basel IV removes the A-IRB approach entirely for exposures to large corporates with revenue above €500 million, and for financial institutions. Banks must use Foundation IRB or the standardized approach instead for such exposure classes.

This change means banks that built detailed A-IRB models for their largest counterparties lose a layer of risk sensitivity they spent years developing. A-IRB allowed institutions to estimate PD, LGD, and EAD internally, capturing differences in collateral structures, seniority, and borrower characteristics that the Foundation IRB and standardized rules flatten out.

The combined pressure falls disproportionately on low-risk portfolios. High-quality, unrated corporates with strong credit histories typically produced much lower risk weights under IRB than under the standardized approach. When the output floor applies, the gap between model-based and standardized capital calculations narrows sharply. Higher-risk portfolios, where internal models already produced elevated risk weights, are comparatively unaffected.

Moving an exposure from a 100% standardized risk weight to 20% reduces required capital by roughly $2 million per $1 billion of exposure. Under Basel IV, the ability to generate those reductions through internal modeling is increasingly constrained in EU/UK jurisdictions, making model calibration a direct input to lending economics.

The Unrated Entity Problem Under Basel IV

100% Risk Weight and What It Means for Lending Portfolios

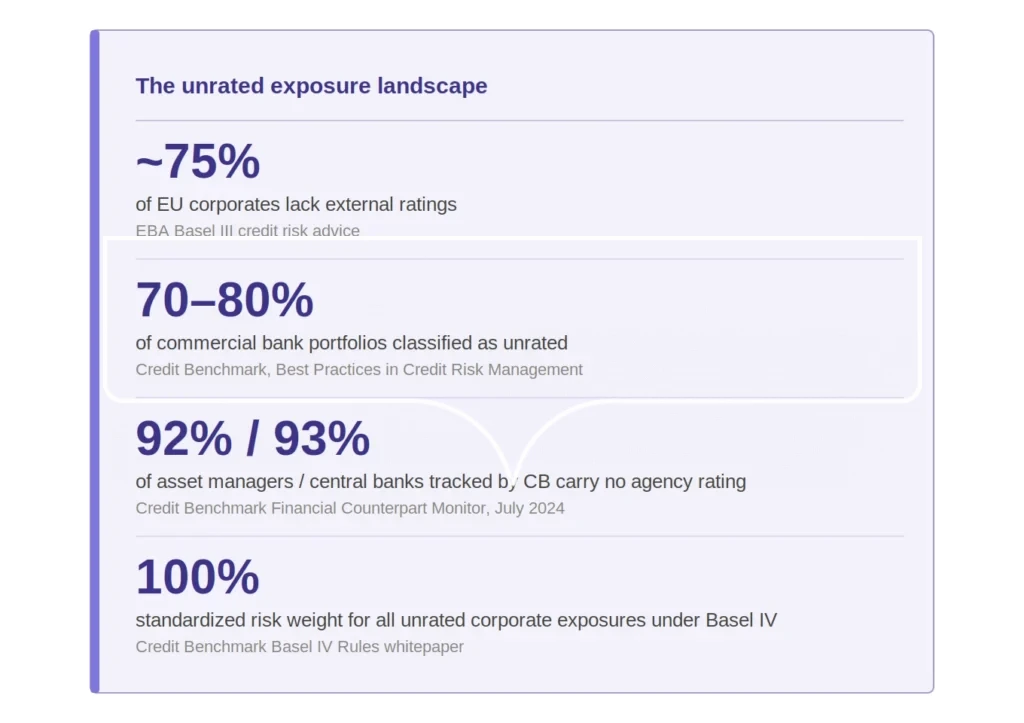

Under Basel IV’s standardized approach, unrated corporate exposures receive a flat 100% risk weight in most jurisdictions. A large international company with decades of operating history and no defaults gets the same regulatory treatment as a newly formed entity with no credit record.

The US proposal introduces a distinction: corporates assessed as “high quality” receive a 65% risk weight, while all others receive 100%. This is more granular than the BCBS standard but still far less risk-sensitive than internal models, and qualifying for the 65% bucket requires meeting specific criteria.

In Europe and the UK, where IRB banks must calculate capital using the standardized approach as a parallel comparison, the 100% unrated weight flows through the output floor calculation for every counterparty without an external rating. The floor binds most tightly on banks with large concentrations of high-quality unrated borrowers, where the gap between internal model estimates and standardized risk weights is widest.

Mid-market companies, private firms, fund structures, and foreign subsidiaries have little economic incentive to seek ratings because they do not access bond markets. Agencies face the same logic in reverse: expanding into private or mid-market entities yields lower revenue than servicing large public issuers, so coverage remains concentrated among publicly traded companies.

Banks cannot close this gap by encouraging borrowers to get rated. The unrated exposure is a permanent feature of most commercial lending books.

Why the Blanket Weight Misrepresents Actual Risk

A creditworthy unrated corporate with a bank-estimated PD of 20 basis points and one with a PD of 300 basis points attract identical standardized weights under the 100% flat charge. That distortion compounds through the output floor, making it more binding for banks with high-quality unrated portfolios than for those with riskier ones.

Credit Benchmark’s Credit Risk Index, which tracks nearly 3,000 private U.S. companies representing about $9 trillion in loans, recorded 4,053 downgrades and 2,872 upgrades over the past three years, with net downgrades in 30 of 36 months. Treating all unrated exposures identically is not only capital-inefficient but also blind to real credit migration at the moment that migration is accelerating.

The CRR III transitional 65% risk weight for unrated corporates with PDs below 0.5% exists because EU regulators recognized that a 100% weight is indefensible for demonstrably low-risk borrowers.

Banks can apply it only with documented PD estimates from validated models, which raises a substantive question: what constitutes sufficient evidence when a borrower has no public rating, no traded debt, and no CDS spread?

The problem is especially acute for European banks dealing with unrated fund counterparties.

Many funds carry very low PDs based on internal assessment but attract the full 100% standardized risk weight, forcing banks to reconcile doing business with these counterparties while absorbing a capital charge that bears no relationship to actual risk. External consensus PD data has direct capital relevance here: it provides the documented evidence that supports lower risk weights under the transitional provision.

Of 10,610 financial counterparties tracked by Credit Benchmark, 92% of asset managers, 93% of central banks, and 66% of North American banks are unrated. Sovereign wealth funds sit at 92% unrated. The problem reaches well beyond corporate lending into counterparty credit risk across derivatives books, fund finance structures, and securities lending relationships.

Model Validation Under Tightened Supervisory Expectations

TRIM previewed what model validation failure costs. Under Basel IV, the stakes are higher in EU/UK jurisdictions because the output floor directly links model accuracy to capital consumption, meaning a bank that loses the right to use its internal model forfeits whatever capital benefit the floor still permits.

The ECB’s Targeted Review of Internal Models (TRIM) demonstrates the result of model validation failure.

TRIM identified over 5,000 deficiencies across European banks, added approximately €275 billion in RWA, and produced a 70-basis-point average CET1 decline. Banks unable to justify their models reverted to standardized calculations with substantially higher capital requirements.

Under the output floor, the consequences of a similar reversion are amplified because the floor already narrows the benefit window.

In the US, internal models are scrapped for regulatory capital, but banks still rely on them for CECL provisioning and CCAR stress testing. The same subjective, risk-based models that regulators no longer trust for capital adequacy still determine provisioning levels and estimate losses under stress.

Model validation and external benchmarking remain essential in the US for the frameworks that actually drive capital outcomes, even though they no longer feed into regulatory capital calculation

What SR 11–7 and TRIM Expect From External Benchmarking

SR 11-7 supervisory guidance from the Federal Reserve sets expectations for model risk management across three areas:

- Evaluation of conceptual soundness

- Ongoing monitoring with benchmarking against independent external data

- Analysis of model outcomes against actual results.

For EU and UK banks, with the output floor capping maximum IRB benefit at 27.5%, PD calibration accuracy becomes a capital efficiency question. Institutions that demonstrate alignment between internal estimates and credible external benchmarks retain a greater share of the remaining IRB benefit. Those who cannot face capital add-ons, model approval delays, or forced reversion to standardized calculations.

For US banks, the SR 11-7 benchmarking expectation applies to CECL and CCAR models. Peer comparison, outlier identification, and the ability to show that internal risk estimates are appropriately calibrated relative to market views deliver value regardless of whether those models feed regulatory capital calculations.

The ECB’s targeted review process and BCBS 239 risk data standards reinforce the same expectation in practice. Examiners probe whether internal PD estimates are benchmarked against external references, and specifically whether those references are independent of issuer-paid rating models.

The Low-Default Portfolio Challenge

Low-default portfolios, covering large corporates, banks, funds, NBFIs, project finance, and specialty insurers, are structurally the hardest to validate. Defaults are rare enough that internal backtesting produces wide confidence intervals and inconclusive results. A well-calibrated model can look identical to a poorly calibrated one simply because the data cannot discriminate between them.

Basel IV’s removal of A-IRB for large corporates and financial institutions compounds this. The models most affected are applied to entities where defaults are rarest and validation evidence is thinnest.

External benchmarking addresses this directly. If a bank’s internal PD estimates for a low-default segment align with the aggregated credit views of 40+ peer institutions, each operating under its own validated Basel framework, supervisors gain an independent reference point confirming calibration is neither too optimistic nor too conservative.

That evidence prevents conservative overlays, constrained model usage, and capital inflation through supervisory add-ons.

As Credit Benchmark’s 2026 Credit Risk Trends analysis observed: “Where internal data runs out, comparable external evidence increasingly determines whether outcomes are informed or blunt.”

A major UK bank demonstrated this when implementing an IFRS 9 validation framework using consensus term structures. Independent, representative data made it significantly easier to justify model adjustments to both internal committees and external regulators. A 2024 study in the Review of Accounting Studies independently confirmed that consensus data improves default prediction accuracy compared to traditional agency ratings.

IRB Nexus, developed by Credit Benchmark in partnership with Oliver Wyman, addresses the low-default problem directly.

It aggregates credit evaluations, ratings, and historical defaults from 40+ contributing banks, providing access to more than 10 million risk estimates annually across segments where internal historical analytics falls short. Cem Dedeaga, Partner at Oliver Wyman, described it as potentially transformative “for banks looking to significantly bolster the historical credit analytics data feeding their capital models.”

Jurisdictional Divergence as an Operational Risk

Each jurisdiction is applying the BCBS framework according to its own supervisory priorities, transitional provisions, and political constraints. The US proposal has gone further than adaptation, producing a structurally different capital regime that is likely to reduce requirements for US banks while EU and UK banks face increases.

The UK has postponed Basel 3.1 partly to observe how the US proceeds. Key elements of the UK credit risk framework remain unresolved. Differences with the EU, such as the treatment of the alpha factor under SA-CCR and the absence of an infrastructure support factor, are likely to widen as each jurisdiction finalizes independently.

The operational consequences are immediate. Banks with entities across London, Frankfurt, and New York must run multiple RWA calculations in parallel. The same exposure receives different risk weights depending on where it is booked. One source of granular exposure data must power UK Pillar 1 reporting, EU CRR III templates, and US reporting schedules simultaneously.

This divergence creates competitive asymmetry. US banks operating under lower capital requirements gain lending capacity and market share advantages. EU and UK banks, facing higher requirements, need more granular risk data to optimize capital efficiency across their multi-jurisdictional operations.

How Banks Are Closing the Validation and Coverage Gaps

Basel IV creates two related problems that vary by jurisdiction but converge on the same need. In Europe and the UK, internal models are constrained by the output floor, while the standardized approach assigns risk-insensitive capital charges to unrated borrowers. In the US, internal models are eliminated for regulatory capital but remain essential for CECL provisioning and CCAR stress testing.

In both cases, banks need external credit evidence that goes beyond their own lending history.

Consensus Credit Data as External Validation Infrastructure

Forty or more global banks, nearly half G-SIBs, submit anonymized internal credit assessments to a common pool. Every contributing institution operates under a Basel IRB framework validated by its own primary regulator, whether the Fed, the ECB, the PRA, or OSFI. The result is a benchmark built on the lending judgments of supervised institutions with capital at risk on the same borrowers being assessed.

Under Basel IV, this structure has direct regulatory relevance. The CRR III transitional provision allows a 65% risk weight for unrated corporates where a bank holds documented PD evidence below 0.5%. Consensus PD data meets that requirement because it is external, independent, and produced by institutions subject to the same supervisory expectations as the bank relying on it.

For SR 11-7 benchmarking, this significantly supports regulatory compliance. Instead of comparing internal estimates against a single external model, banks benchmark against an aggregated peer view. When supervisors ask whether a PD estimate on a mid-market borrower is reasonable, a bank can show alignment with, or document its divergence from, the collective view of lenders exposed to the same entity.

In the US, where regulatory capital no longer depends on IRB, this benchmarking supports the CECL and CCAR models that do drive real capital outcomes.

Beyond regulatory use cases, consensus data supports the analytics that portfolio teams use daily:

- Credit migration monitoring and early warning signals that flag deterioration 6-8 months before agency downgrades

- Correlation analysis across sectors and geographies

- Transition matrices for stress testing

- Rating boundary risk identification

As data budgets shift toward portfolio management teams who need to demonstrate risk-adjusted returns under tighter capital constraints, these operational applications often carry more immediate commercial value than regulatory compliance alone.

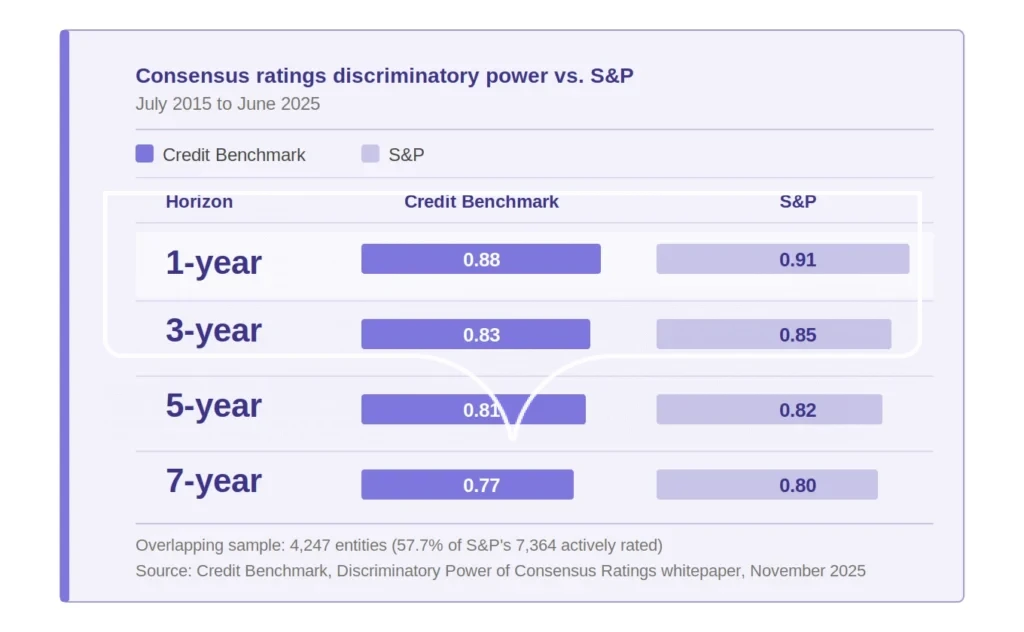

Even better, discriminatory power evidence confirms this approach does not sacrifice accuracy for coverage. Over a 10-year period from July 2015 to June 2025, Credit Benchmark’s consensus ratings were tested against actual defaults across 4,247 entities that both Credit Benchmark and S&P actively rated.

When results were analyzed, Credit Benchmark’s one-year Gini ratio was 0.88, compared with S&P’s 0.91. The gap remains similarly narrow at three years (0.83 vs. 0.85), five years (0.81 vs. 0.82), and seven years (0.77 vs. 0.80). The Credit Risk Index correlates strongly with observed S&P default rates.

Explore the full depth of credit risk intelligence that underpins this benchmarking infrastructure.

This means that consensus data’s broad coverage delivers comparable accuracy across a population of borrowers that is five times larger than that covered by rating agencies. Independent research confirms this.

A 2024 Review of Accounting Studies paper independently confirmed that consensus data improves default prediction accuracy relative to traditional agency ratings. Risk.net named Credit Benchmark Credit Data Provider of the Year in 2025, and the Bank of England used its data when evaluating unrated companies for the COVID Corporate Financing Facility.

Implementation Realism and Case Evidence

Canada implemented Basel IV early, making Canadian institutions useful reference points for how consensus data works within a live regulatory framework. In February 2025, OSFI announced the Canadian output floor would remain at 67.5% until further notice, with at least two years’ notice required before any further increases resume.

The Canadian Derivatives Clearing Corporation (CDCC) clears exchange-traded derivatives in Canada. Most of its 30+ clearing members carry no external agency rating. CDCC uses Credit Benchmark’s credit risk monitoring tools to monitor these members continuously and adjust margin requirements before problems emerge.

Vladimir Levtsun, Acting Director of Financial Resilience Risk at CDCC: “Credit Benchmark’s data has contributed to directly strengthening our ability to manage counterparty risk and enhance internal reporting, leading to more confident, proactive risk decisions.”

A major US bank with approximately $150 billion in assets has used consensus data since 2017 to recalibrate internal PD and LGD estimates and prepare for Shared National Credit examinations, where regulators assess whether internal credit ratings hold up against external evidence.

Most implementations are completed within 60 to 90 days, delivered via API, Bloomberg Terminal, Excel add-in, Snowflake, or AWS. For Bloomberg users, 70,000 entities are available directly within existing Terminal workflows.

An automated mapping engine handles LEI, TIN, and DUNS reconciliation, removing the manual entity matching that typically slows data integrations.

What This Means for Capital Planning in 2026 and Beyond

The output floor rises from 55% in 2026 to 65% in 2028, then to 72.5% in 2030. The capital pressure EU and UK banks are managing today is not the peak. For most IRB banks in those jurisdictions, the 2026 to 2028 window is where the floor begins to bind broadly across portfolio segments.

Meanwhile, the US is moving in a different direction. Agencies describe the March 2026 proposals as producing a modest aggregate decrease in capital requirements, though the rules are not final. US banks are expected to gain a competitive advantage.

Lower requirements position US banks to expand lending and capture market share, while European and UK banks face binding constraints. The US proposal’s favorable treatment of securitization with risk mitigants is also likely to drive increased CLO and structured finance activity.

Private credit is projected to expand from $1.7 trillion to $3.5 trillion, and bank exposure to nonbank financial institutions reached $2.1 trillion in Q3 2024. These are largely unrated borrowers where the standardized approach applies the bluntest capital treatment. Without scalable external credit intelligence on these counterparties, banks allocate capital to regulatory floors rather than actual risk.

As Michael Crumpler noted in a 2025 GARP podcast, “Credit risk was rising globally before the trade war started.” Credit Benchmark’s data confirms the pattern, with net downgrades in 30 of the past 36 months across nearly 3,000 private U.S. companies.

Globally, capital optimization is giving way to risk defensibility across jurisdictions. In the US, this shift began years ago with the Collins Amendment, which established binding, standardized capital floors, and Basel IV continues along the same trajectory.

Europe and the UK are also making the shift now as the output floor phases in. Institutions that strengthen the evidence behind their risk estimates before the transition period ends and the full output floor takes effect will be best positioned to adapt to the new environment.

Credit Benchmark’s Role in This New Future

Credit Benchmark provides consensus credit data on more than 120,000 entities, around 90% of which are unrated, aggregated from 40+ global banks. For institutions navigating Basel IV, this data provides an external reference for validating PD estimates, supports the evidence required for lower risk weights under frameworks like CRR III, and delivers the peer benchmarking, early warning signals, and credit migration analytics that drive capital planning and risk governance across all jurisdictions.

Credit Benchmark data is also valuable for portfolio management, including extensive correlation and transition matrices.