Introduction

For economies and stock markets, the past 12 months have been very volatile. US tariffs, Middle East conflict, and AI-driven disruption have combined to give investors a rocky ride. The default risk picture is also shifting. Credit spreads moved from close to an all-time low in January of 2.65 to a near-time high of 3.46 (a 30% increase in interest payments) before dropping back to 2.85 this month.

Meanwhile consensus credit views across 40+ major banks show that risk has been steadily increasing – across 120 Global indices, median default probability ticked up in 10 of the past 12 months.

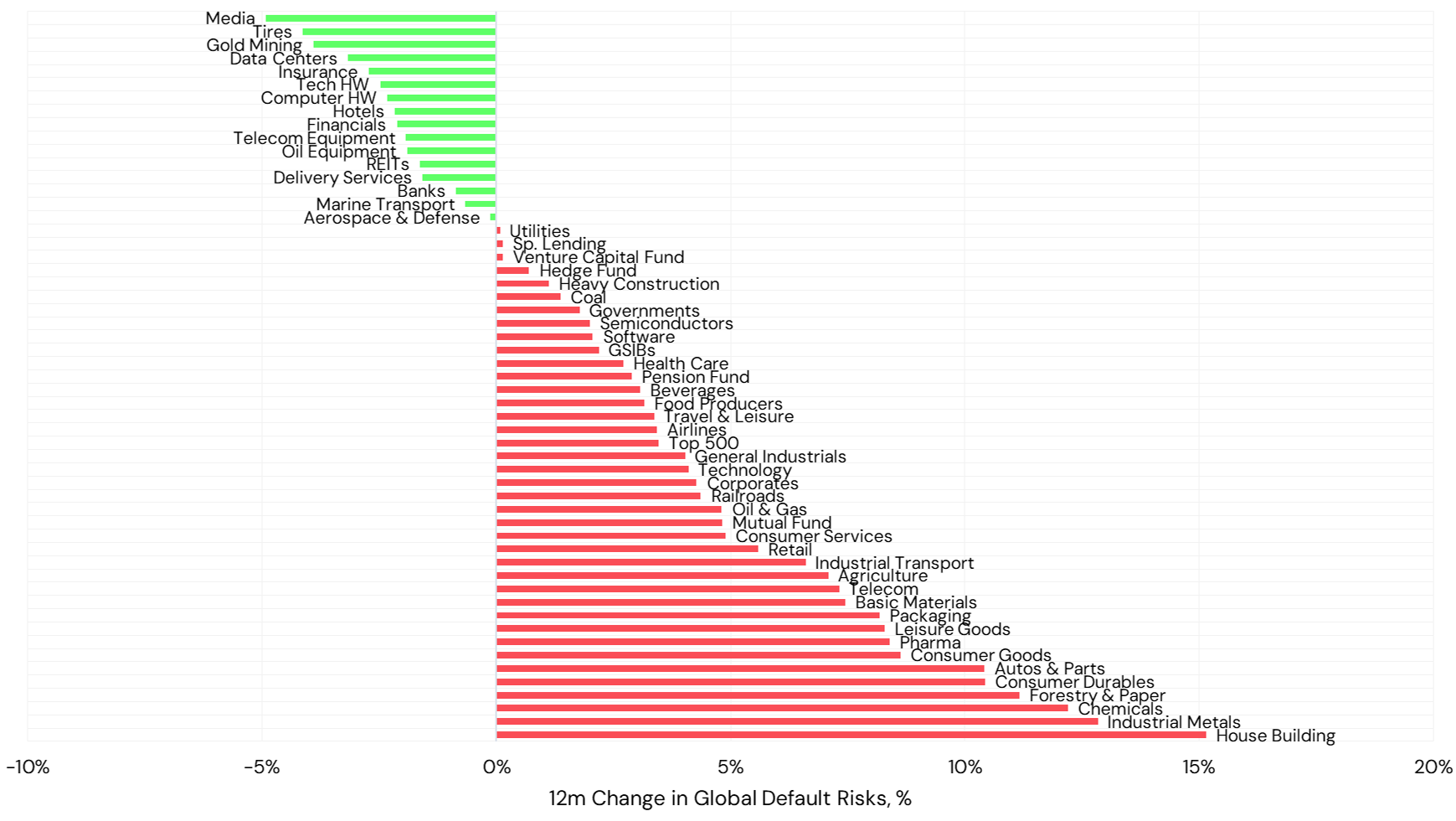

But there have been some major divergences. The chart below shows the 12m change in risk for key global industries and sectors:

12-month change in credit risk for global industries

Some Clear Global Takeaways:

- Financials – Banks, Insurance and Real Estate – have outperformed Corporates

- Precious metals with limited physical use have outperformed industrial-use metals

- Data Centers, which have seen exponential growing investments, have outperformed Semiconductors and Software

- Utilities, Equipment and other infrastructure – the “HALO” sectors are improving

- Hedge Funds have outperformed Mutual Funds

- Consumer sectors – durables, services, travel, retail – are all deteriorating in the face of rising inflation, job insecurity, and geopolitical disruption.

Looking Forward, What Can We Expect?

- The steady trend rise in global credit risk is likely to continue, but if inflation drives long rates higher then Insurance companies will continue to do well (due to lower liabilities) while other financials may be more mixed.

- Corporate HALO (High Assets Low Obsolescence) sectors are likely to continue to improve, especially infrastructure and equipment manufacturers and operators. If geopolitical tensions ease, then some of the hard-hit consumer sectors may see credit quality bounce back.

- The impact of the Middle East conflict could persist beyond any peace deal due to supply chain disruptions and infrastructure damage. But supply shifts bring gains for some; e.g. paper packaging could take market share from plastics if Gulf issues persist, and other fertilizer sources will benefit.

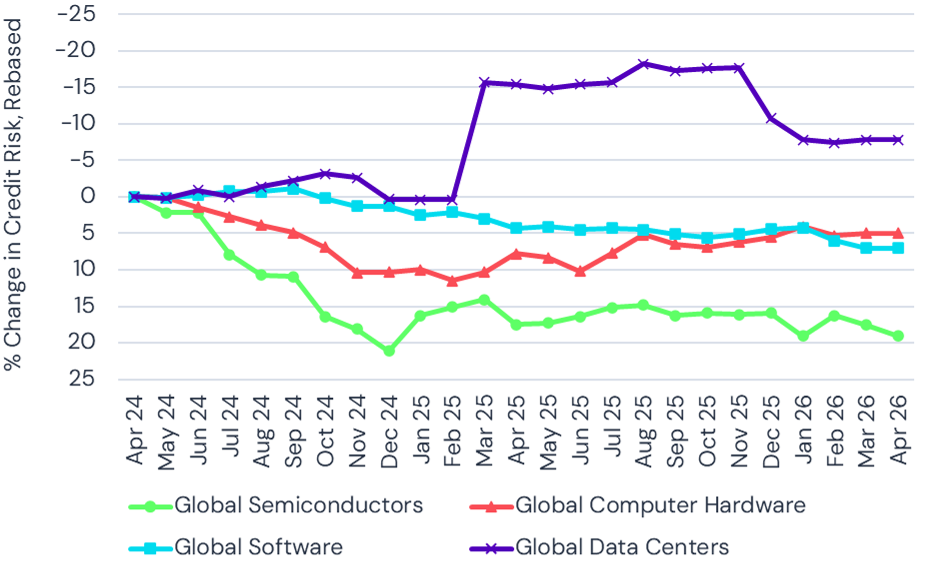

The charts below highlights one key potential reversal in coming months – the gap between AI-related borrowers and other tech sectors.

AI Data Centers vs. Global Tech: Credit Trend

AI Data Centers vs. Global Tech: Credit Level

In the past 6 months, energy- and water-hungry Data Centers show a credit deterioration of nearly 10%, much larger the Software and Semiconductor moves over the same period. The broader tech Hardware index shows a slight improvement. Data Centers include a high (40%) proportion of non-investment grade firms, although Software has a significant exposure (around 30%) in the even higher risk ‘b’ category. This helps to explain some of the material investment outflows from Private credit funds due to an average 25% exposure to Technology, mainly in AI-disrupted Software. But the Data Center boom is not immune to credit concerns.

Credit Benchmark provides ongoing consensus credit data, analytics, and research. For more detailed analysis and custom data extracts, please contact your Credit Benchmark representative or visit creditbenchmark.com.