Actionable insights from the collective credit intelligence of the world’s leading financial institutions.

Introduction: A Consensus View of European Credit Risk

Understanding credit risk in Europe increasingly requires a different lens – one that goes beyond traditional indicators to incorporate more forward-looking signals. The perspectives of lenders and investors with direct exposure can offer a more immediate and nuanced view of changing credit conditions, capturing shifts that may not yet be visible in market prices or macroeconomic data.

Against this backdrop, Europe’s credit landscape is becoming more fragmented. Credit conditions are diverging across countries, sectors and individual borrowers, reflecting a mix of geopolitical tensions, tariffs, fiscal pressures, higher defence spending and structural shifts in trade and technology. These forces are creating a more uneven risk environment than traditional measures alone suggest.

This report examines where credit risk is building, where resilience is emerging, and what these shifts mean for lenders, investors, insurers and portfolio managers. The findings highlight why European exposure cannot be managed as a regional allocation, and why more timely, granular credit insight is becoming increasingly important for decision-making.

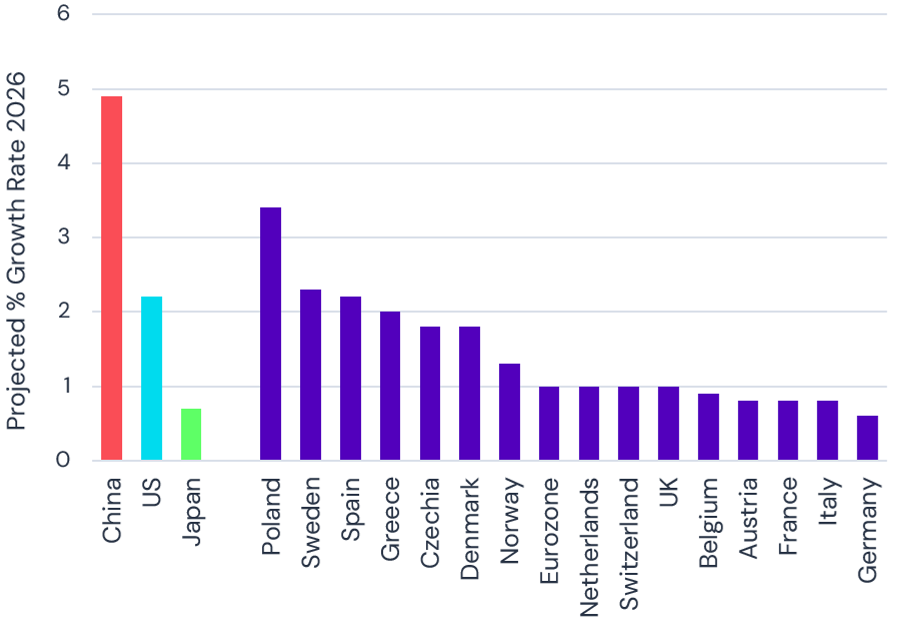

Europe faces a complex mix of tariffs, fiscal pressures, higher defence spending, energy costs and structural competitiveness challenges. These forces are affecting countries differently, resulting in diverging growth prospects, fiscal flexibility and corporate credit conditions. Credit Benchmark’s consensus credit intelligence provides a forward-looking perspective on where these differences are becoming most apparent.

Projected GDP growth by country, 2026

Source: Economist, 13 June 2026.

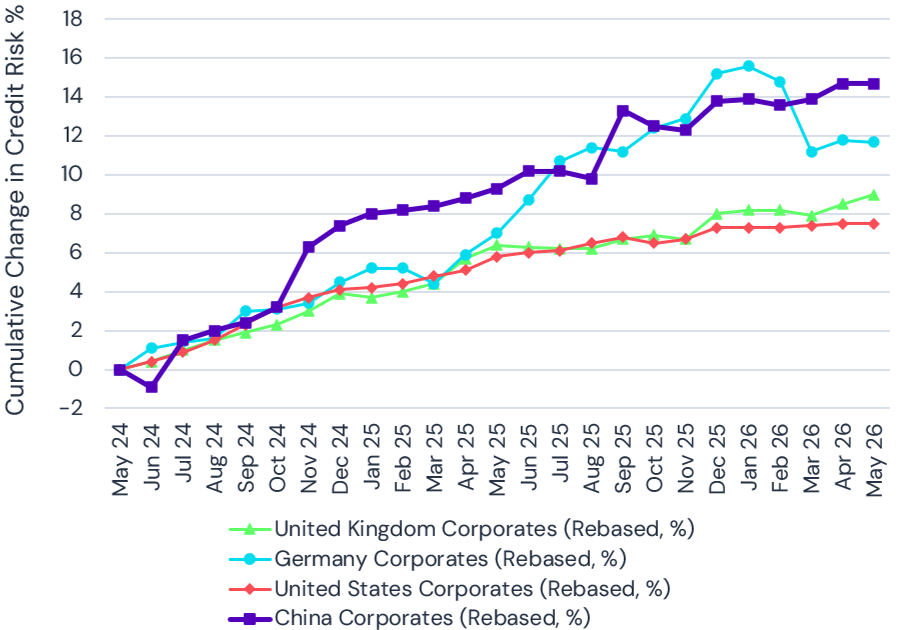

Cumulative change in corporate default risk: global majors

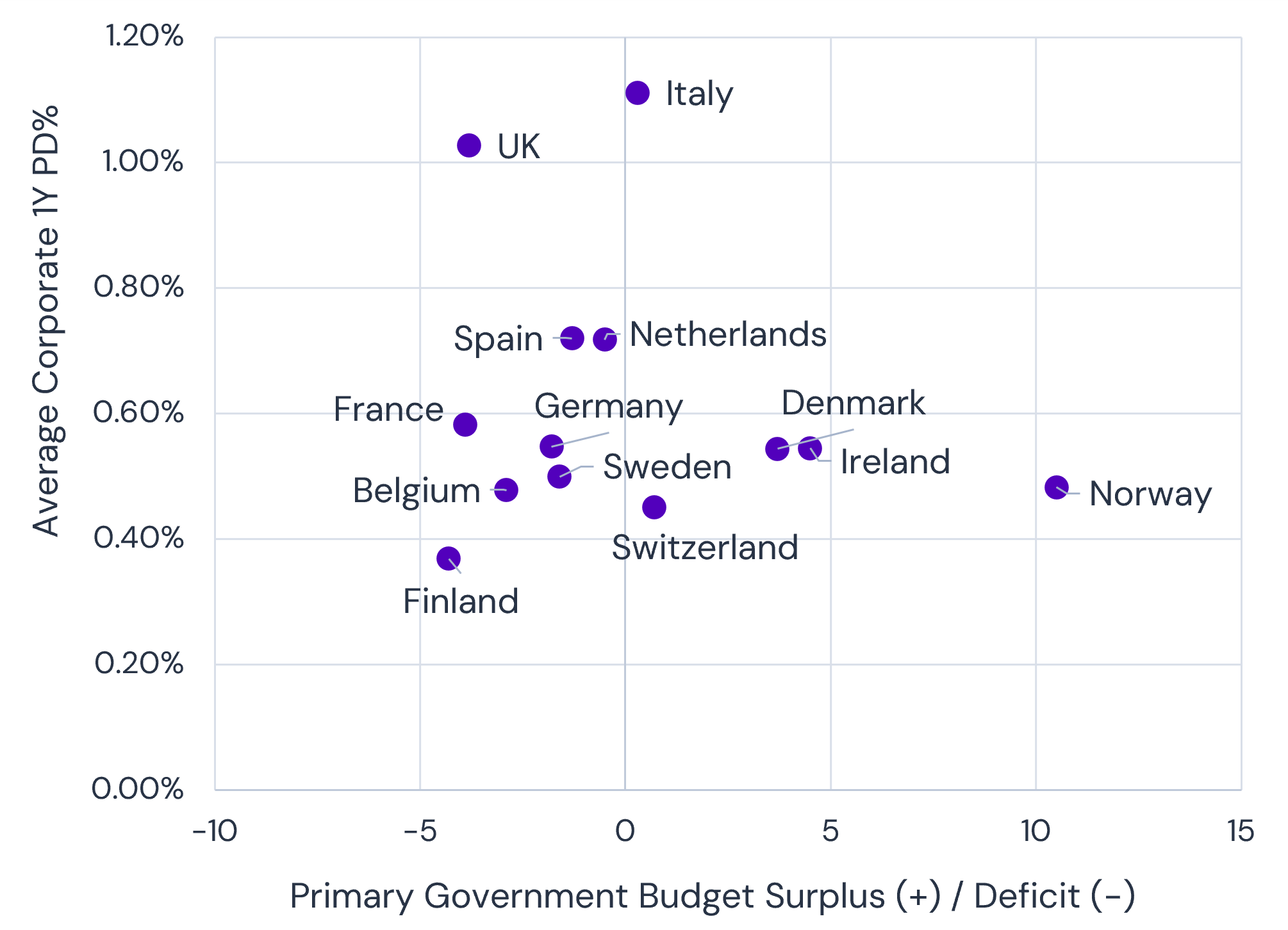

Corporate Default Risk vs Sovereign Deficits: Where Europe Has Fiscal Headroom

Credit Benchmark consensus data maps each European economy by corporate default risk against its primary fiscal balance, revealing where governments retain room to spend and which corporate sectors are most exposed in a downturn.

- Strong on both counts: Norway, Ireland, Denmark and Switzerland pair primary surpluses with resilient corporate balance sheets.

- Deficits but resilient: Finland, Belgium, Sweden, France and Germany run primary deficits, yet robust corporate sectors limit crowding-out risk.

- Most exposed: the UK combines high corporate default risk with a large primary deficit; Italy’s corporate risk is higher still, offset only by a narrow surplus.

- Watch long rates: primary balances exclude interest payments, so higher long-term yields could intensify the strain on economies such as Italy.

European corporate default risk vs primary fiscal balance

Each economy plotted by Credit Benchmark consensus corporate default risk against its primary fiscal balance. Sources: Credit Benchmark; TheGlobalEconomy.com.

Recent Trends in European Corporate Default Risk: Signs of Stabilisation

Credit Benchmark consensus data shows European corporate default risk has risen over the past two years, but the most recent months point to a possible turning point.

- Two-year rise: GDP-weighted corporate default risk is up around 10% over the past two years.

- Tariff peak: net downgrades (the Credit Risk Indicator, “CRI”) peaked with the April 2025 US tariff announcement.

- Turning point: the downtrend crossed into the improvement zone in Q4 2025 and has shown net upgrades for the past four months.

European corporate default risk and net rating changes (CRI)

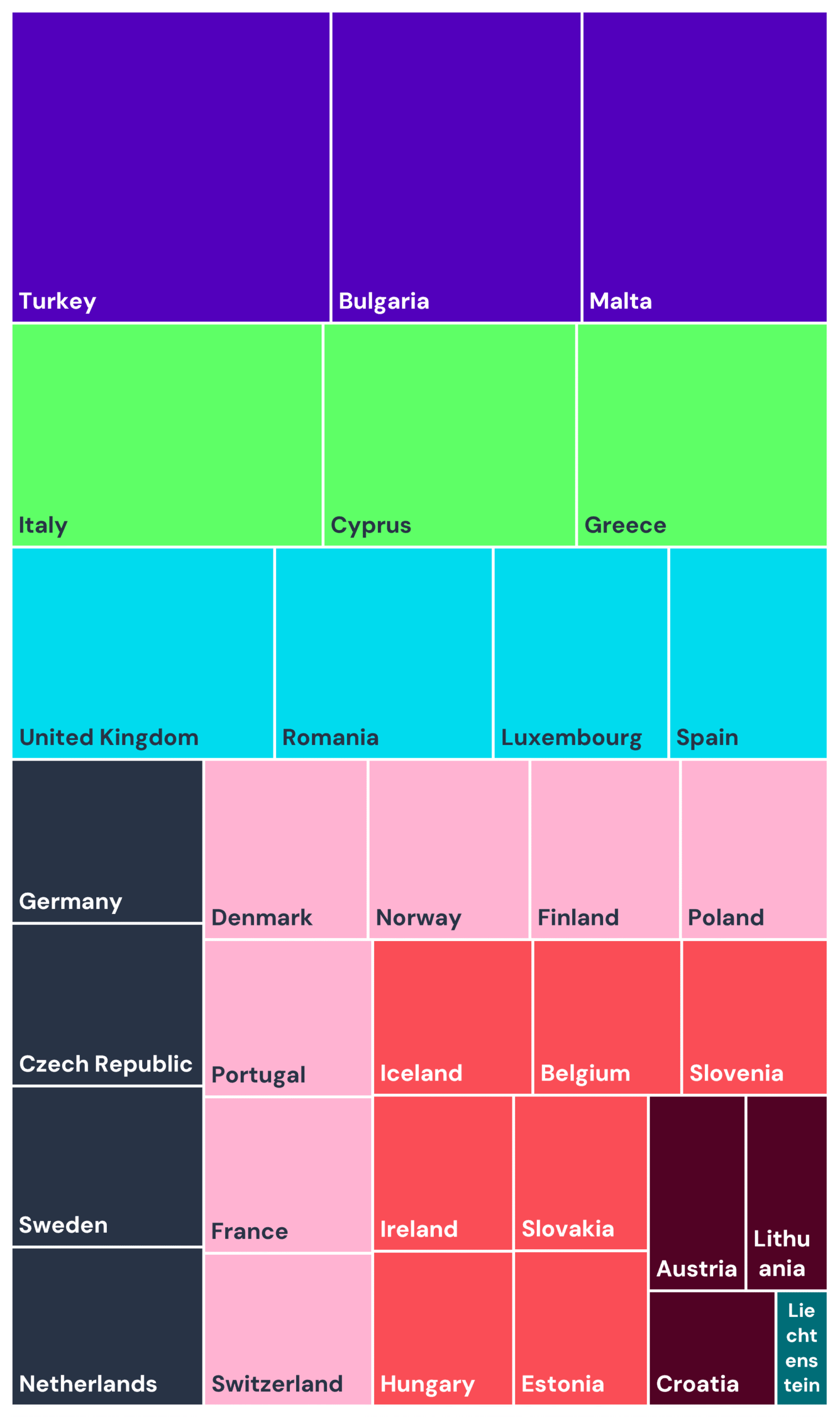

Mapping European Corporate Credit Risk: Where Default Risk Is Highest and Lowest

Across the wider European universe, Credit Benchmark consensus data reveals a wide spread in average corporate default risk from one country to the next.

- Highest risk: Turkey, Bulgaria and Malta.

- Next tier: Italy, Cyprus and Greece, closely followed by the UK and Romania.

- Mid-distribution: Germany, the Netherlands, Luxembourg, Spain, Sweden and the Czech Republic.

- Lowest risk: a cluster of Eastern European states (Slovenia, Slovakia, Estonia, Croatia, Hungary and Lithuania), plus Ireland, Iceland, Austria, Belgium and Liechtenstein.

- Read with care: the map reflects average borrower PDs, so it also captures lenders’ risk appetite — in some countries banks focus lending on lower-risk obligors.

European corporate credit-risk map: average default risk by country

Major European Corporates: Default Risk Trends by Country

Among the major economies, Credit Benchmark consensus data shows sharply different corporate trajectories over the past two years.

- France: corporate default risk rose 16% in the 18 months to November 2025, then recovered dramatically.

- UK vs Germany: closely aligned, but recently the UK has continued to deteriorate while Germany has shown a modest improvement.

- Italy: deteriorated nearly 8% up to Q3 2025, with a modest recovery since.

Corporate default-risk trends: France, UK, Germany and Italy

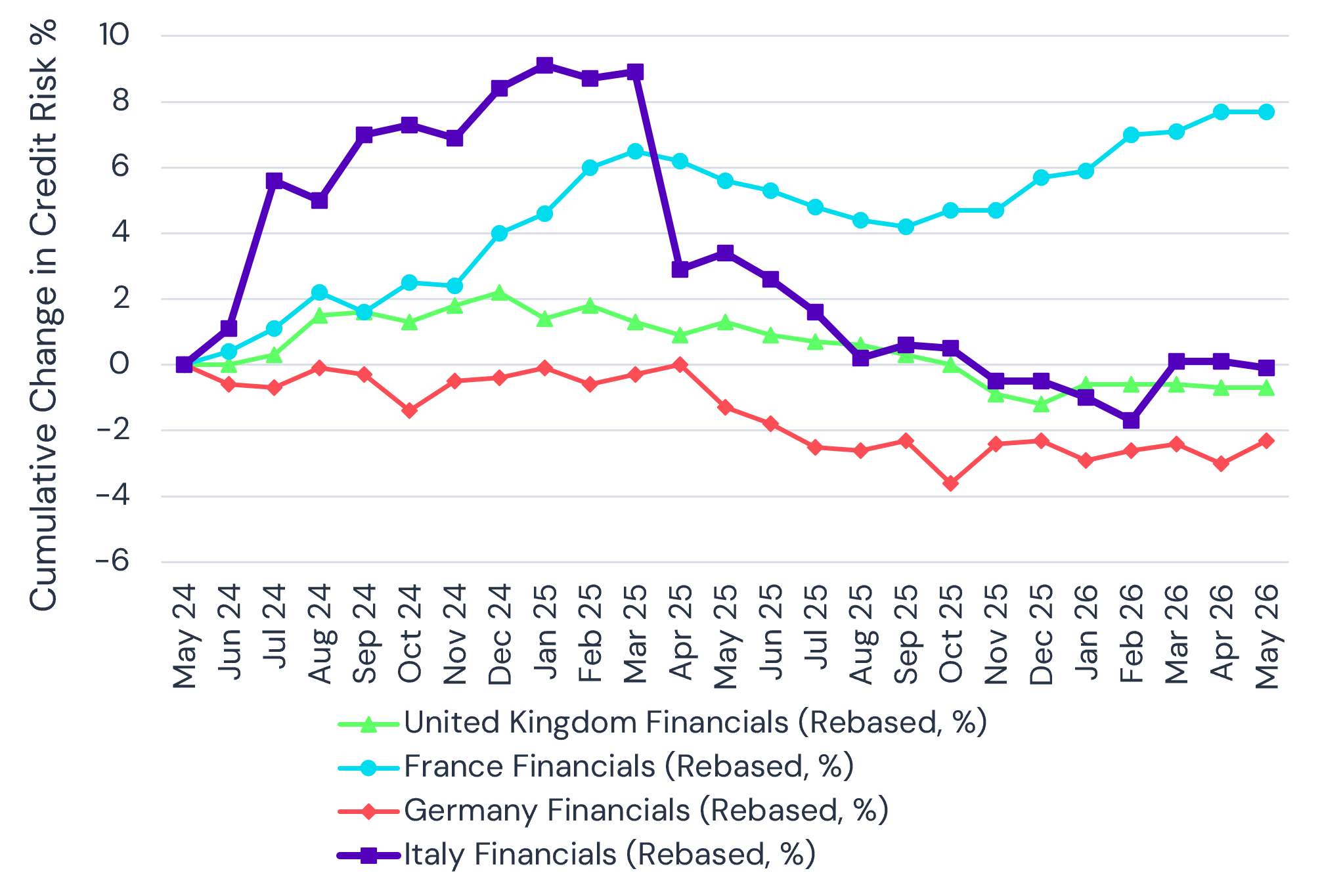

Major European Financials: Default Risk Trends by Country

Credit Benchmark consensus data for the financial sector shows a similar pattern of divergence across the major economies.

- France: financials stand out with an 8% trend deterioration over two years.

- UK and Germany: closely aligned throughout the period.

- Italy: a dramatic shift from deterioration to improvement in early 2025, with a modest but consistent improvement since.

Financial-sector default-risk trends: France, UK, Germany and Italy

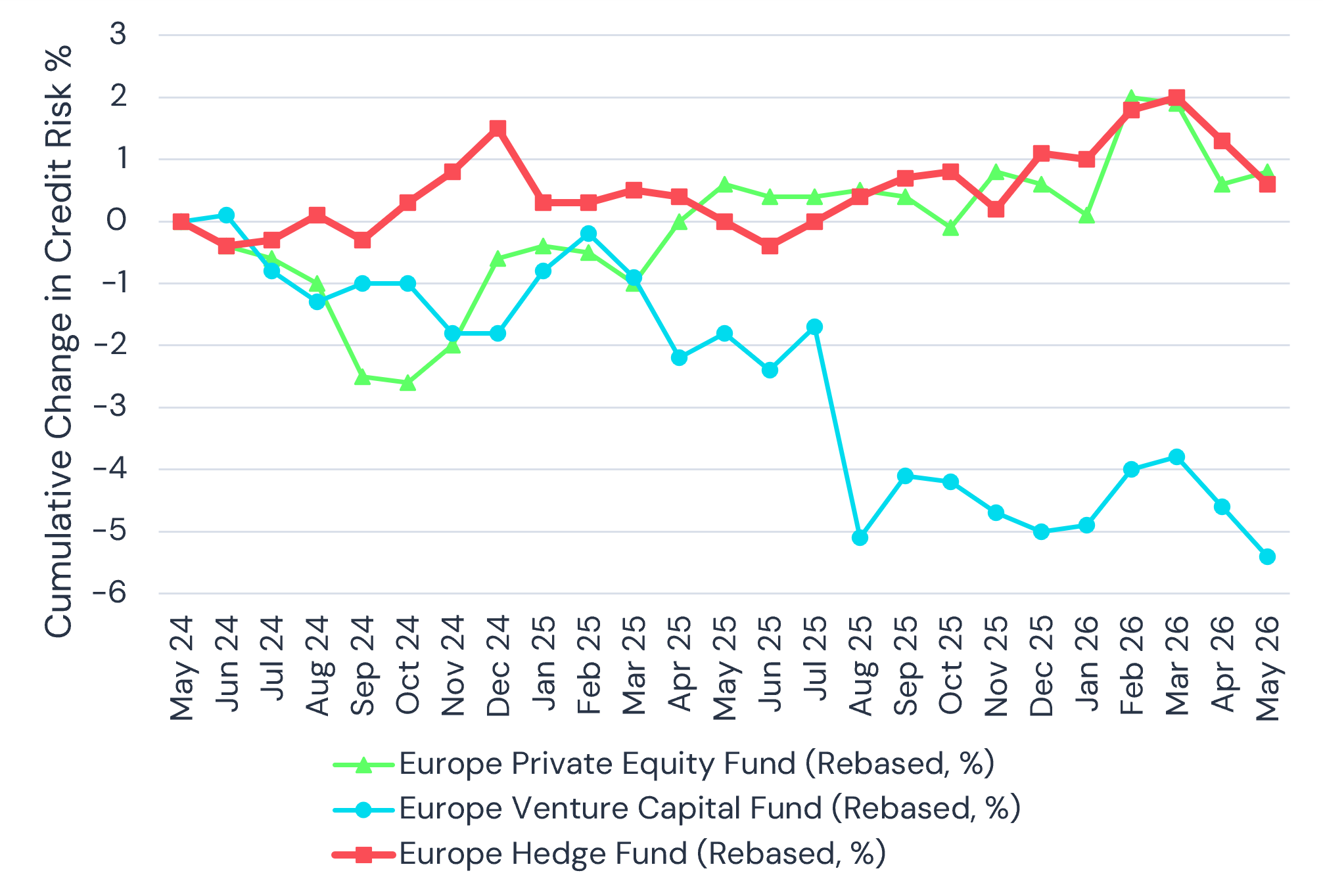

European Private Funds: Default Risk Across Private Equity, Venture Capital and Hedge Funds

With some high-profile US private credit funds recently suspending withdrawals, Credit Benchmark consensus data offers a timely read on European fund risk.

- Market backdrop: suspended withdrawals at major US private credit funds have driven BDC rating changes and sharpened investor focus on fund liquidity and solvency.

- Scope: the data covers Private Equity, Venture Capital and Hedge Funds in Europe, including some private credit funds.

- Trends: Private Equity and Hedge Funds show little change, while Venture Capital funds show a modest but steady improvement over the past two years.

Default-risk trends for European private funds (PE, VC, hedge funds)

European Industry Credit Risk: Default Trends Across Key Sectors

Credit Benchmark consensus data, indexed and GDP-weighted across Europe, highlights diverging two-year default-risk trends among key industries.

- Industrials: deteriorated 5% up to Q3 2025, with a modest recovery since.

- Technology: down nearly 8% over two years, splitting globally into winners and losers.

- Real Estate: risk peaked in early 2025 and has partly recovered.

- Consumer divergence: Consumer Services are broadly stable, but Consumer Goods have deteriorated by nearly 9%, partly reflecting US tariff risk.

GDP-weighted default-risk trends by industry

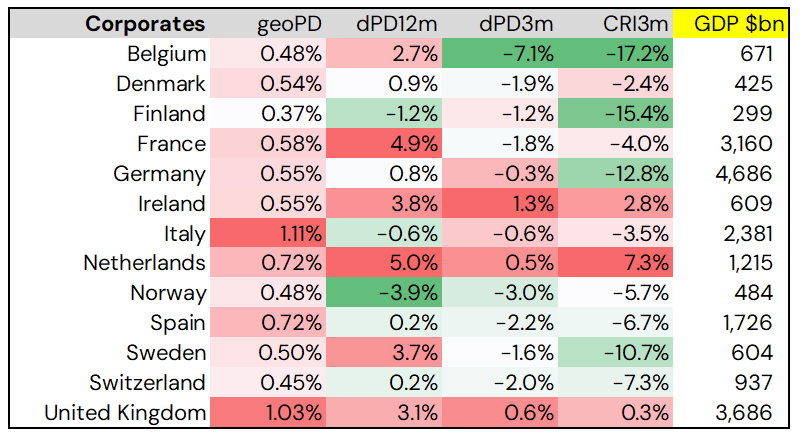

Western European Corporate Credit Trends by Country

Credit Benchmark consensus data shows major Western European corporate indices diverging sharply, with several countries already reversing course.

- 12-month deterioration: Belgium, France, Ireland, the Netherlands, Sweden and the UK all show 12-month PD deterioration.

- Recent reversals: Belgium, France and Sweden have reversed these trends in recent months.

- Forward signal: net downgrades (CRI) point to further decline in the Netherlands, but scope for improvement in Belgium, Finland, Germany, Sweden and Switzerland.

Western European corporate default risk by country

Investment Grade vs High Yield: Western European Corporate Credit Quality

Splitting the universe into Investment Grade and High Yield, Credit Benchmark consensus data again reveals highly divergent patterns across Western Europe.

- High Yield stress: Ireland and the Netherlands show both 12-month and 3-month HY PD deterioration.

- IG with upside: France, Germany and Sweden lead IG deterioration over 12 months, but net downgrades signal strong scope for improvement in all three; with Spain, German HY corporates also show a recent shift to upgrades.

- Consistent improver: Switzerland shows broadly consistent improvement across both IG and HY, especially in recent months.

Investment Grade corporate default risk by country

High Yield corporate default risk by country

Source: Credit Benchmark consensus data — geoPD, 12-month and 3-month PD change, and net rating change (CRI).

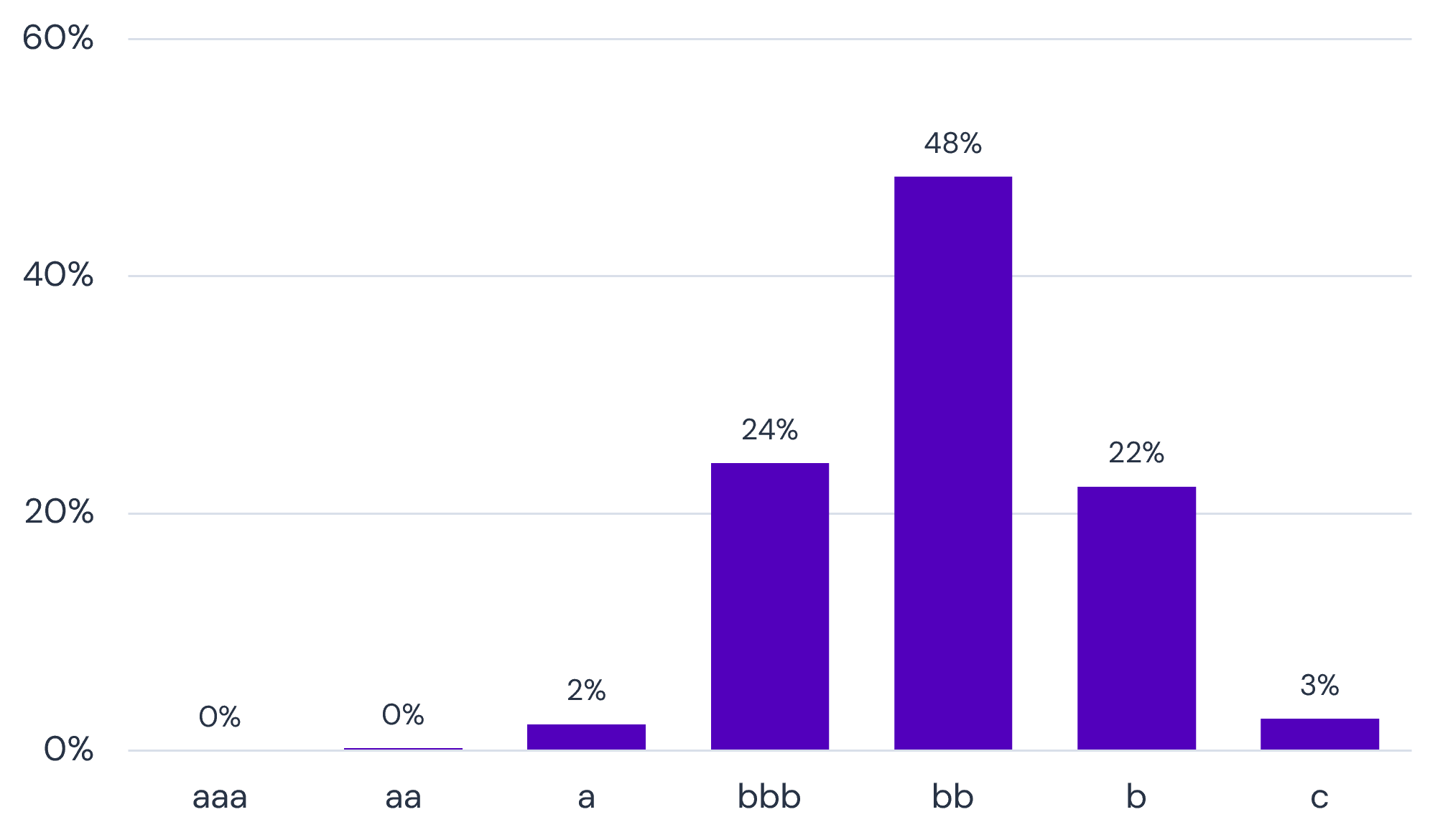

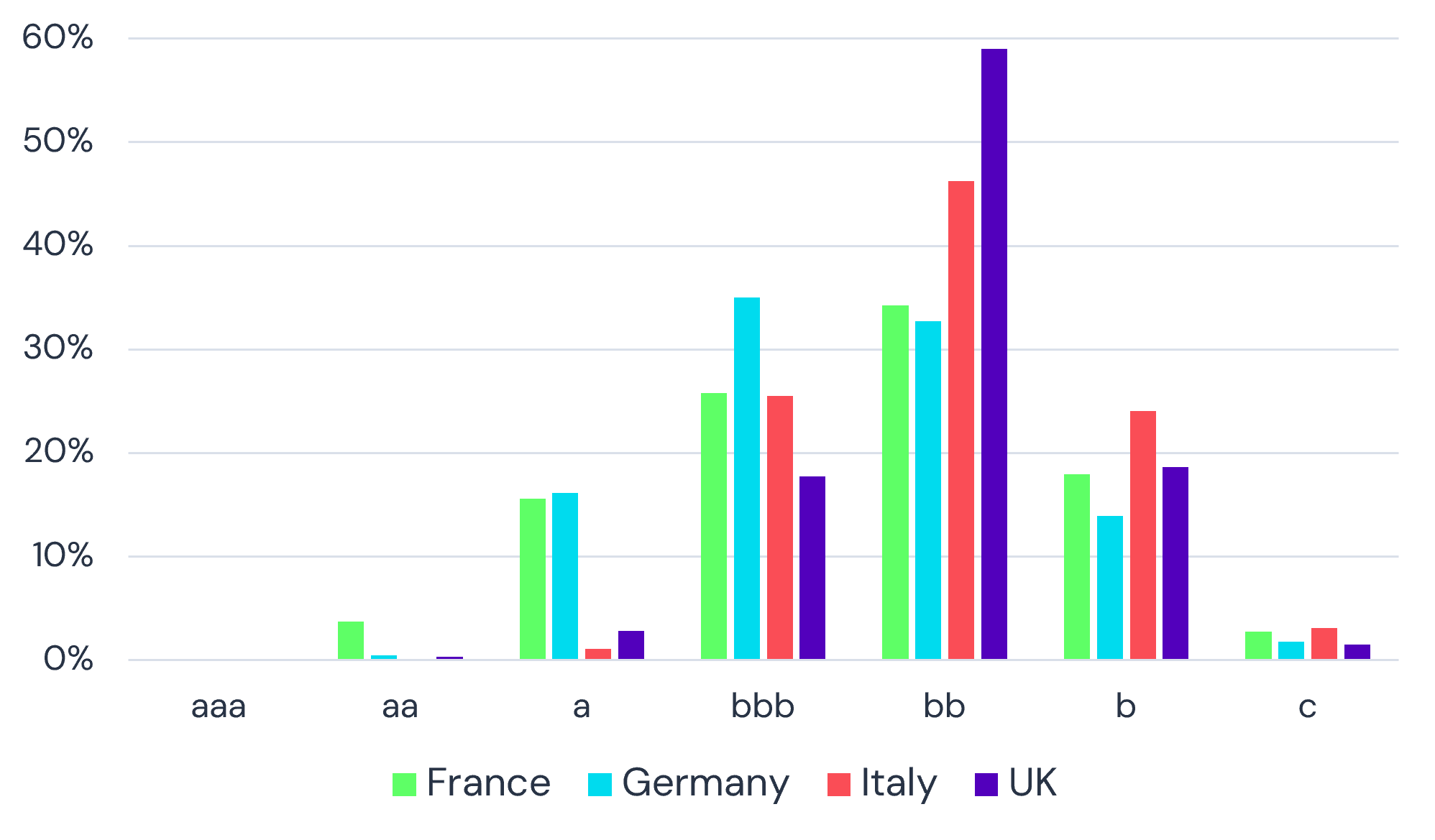

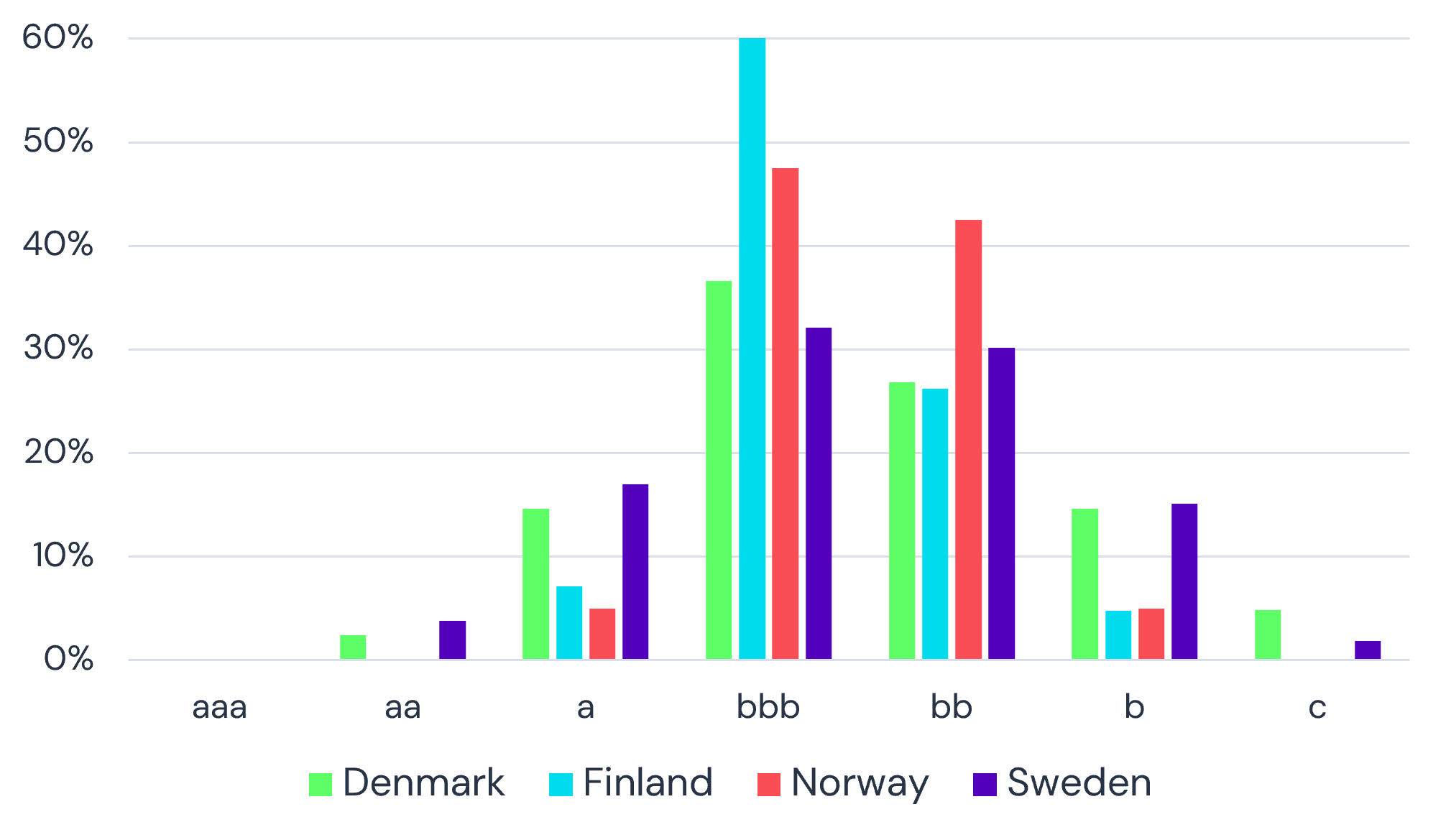

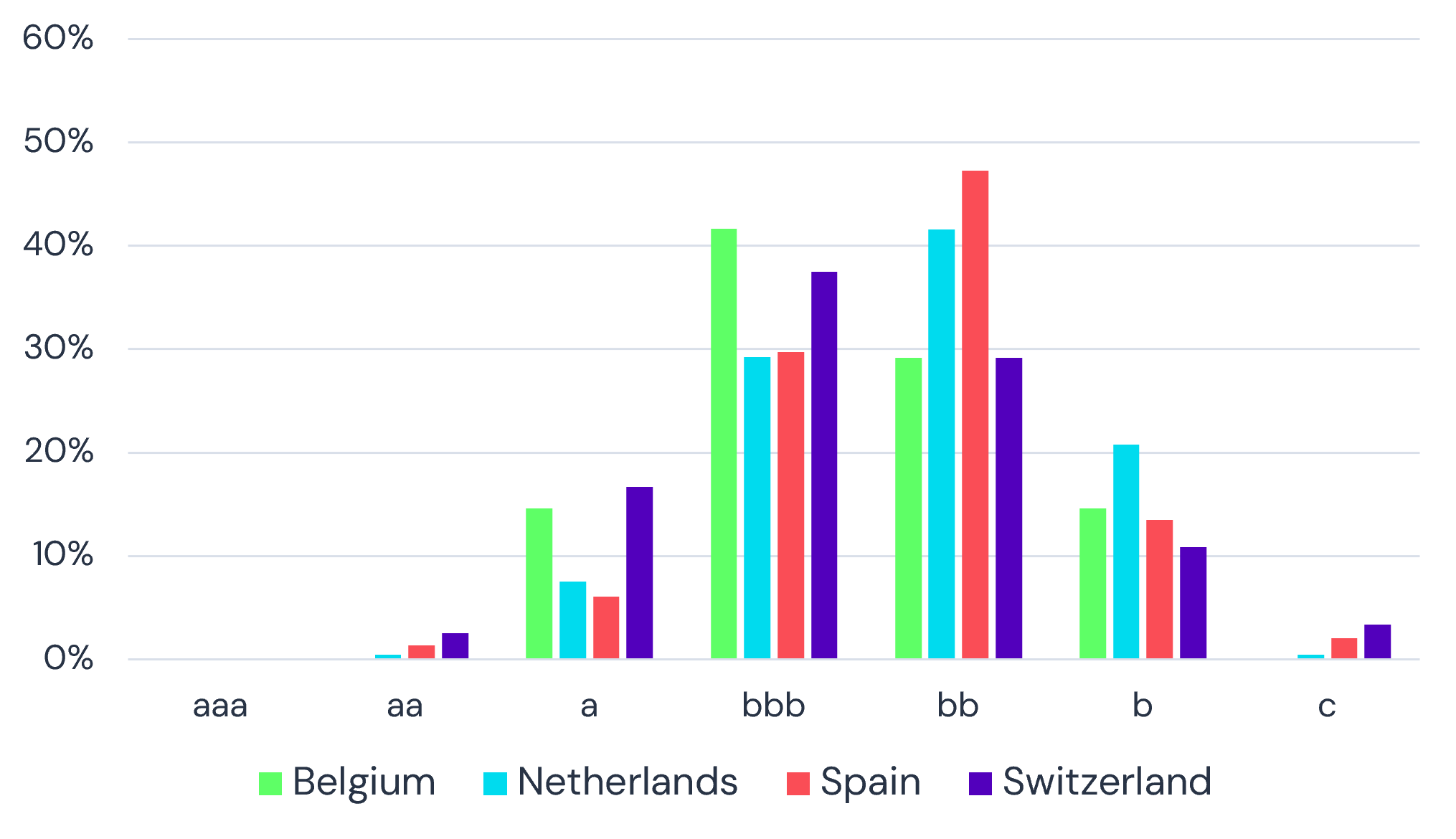

Credit Quality Profiles of Western European Corporates

Credit Benchmark consensus data shows that most Western European corporates sit in the High Yield range, with notable differences between countries.

- Mostly High Yield: 48% of European corporates are in the bb category and 25% in b or c.

- UK skew: the UK stands out with 60% in bb and less than 20% in bbb.

- Nordic strength: the Nordics are the highest-quality group, with over 50% of Finland and Norway in bbb and low b/c exposure.

- The rest: the remainder of Western Europe is mixed, with bbb shares at or above average.

All corporates (combined)

Major economies (66% of W. Europe GDP)

Nordic countries (9% of W. Europe GDP)

Rest of Western Europe (25% of W. Europe GDP)

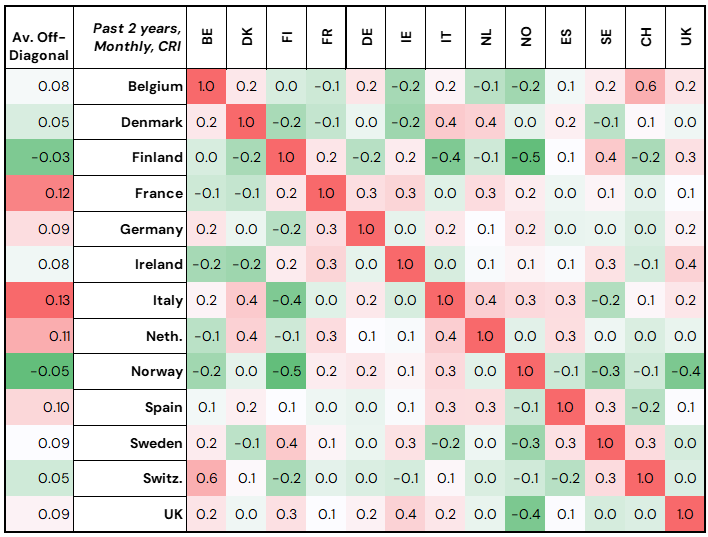

Credit Risk Correlations Across European Corporates

Credit Benchmark consensus data shows that correlations between monthly default-risk changes are unusually low across Europe, pointing to strong portfolio diversity.

- Low correlations: monthly PD-change correlations over two years are low versus historical norms, implying diverse credit exposures.

- Notable pairs: Finland and Norway are strongly negatively correlated; the highest correlation is a moderate 0.57, between Switzerland and Belgium.

- Eurozone insight: despite a shared currency and interest rate, member countries’ credit drivers are not closely aligned.

Cross-country correlations of monthly default-risk changes

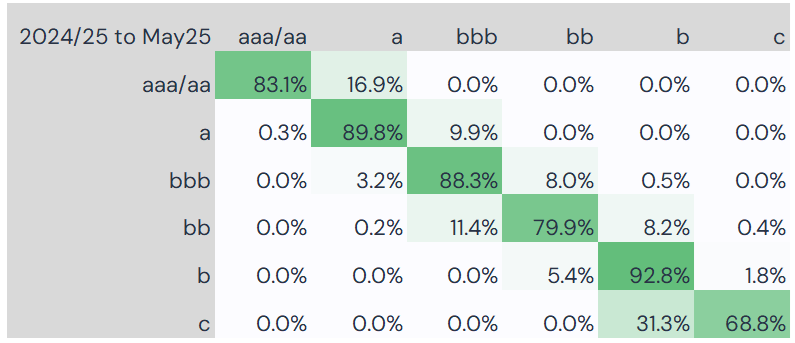

Credit Rating Transitions Across European Corporates

Credit Benchmark consensus transition matrices for the major economies show broad stability between the latest 12 months and the prior year, with an emerging tilt toward upgrades.

- Stable overall: aggregated transition matrices show high consistency year-on-year.

- Fewer downgrades: downgrade frequencies eased slightly, especially bb to b — though the b to c rate rose from 1.8% to 3%.

- More upgrades: the b to bb upgrade frequency jumped from 5.4% to 12.7%.

Corporate rating-transition matrix: latest 12 months vs prior year

Full transition matrices available from Credit Benchmark. Source: Credit Benchmark consensus data.

Conclusion: Beyond Ratings and Market Signals

The defining characteristic of today’s European credit market is not simply higher or lower risk—it is increasing divergence. Countries, sectors and industries are responding differently to tariffs, fiscal pressures, geopolitical developments and structural economic change. While European corporate default risk has risen over the past two years, recent consensus data points to a potential turning point, with improving credit momentum emerging in parts of the market even as other areas continue to weaken.

For risk managers and investors, broad regional assumptions are becoming less useful. Understanding where resilience is strengthening, where vulnerabilities are emerging and where credit conditions are changing first will increasingly drive better underwriting, portfolio construction and capital allocation decisions.

Credit Benchmark’s consensus credit intelligence provides a differentiated view of these evolving dynamics, combining forward-looking assessments from leading global financial institutions with the flexibility to analyse credit risk by country, sector, industry or portfolio. As Europe’s credit cycle continues to evolve, this more granular perspective can help institutions identify emerging risks and opportunities earlier, supporting more informed underwriting, portfolio management and capital allocation decisions.

Download PDF

Please complete your details to download the PDF of this report: