IG sectors move in lockstep, but correlation breaks down sharply across the quality divide.

Canada Credit Risk Outlook 2026

This Canada credit risk outlook 2026 examines default risk trends across Canadian Corporates and Financials, drawing on the Credit Benchmark consensus dataset – aggregated from the internal credit risk estimates of major global financial institutions – to assess how macroeconomic conditions and trade policy are reshaping the credit landscape.

Canada is expected to see faster growth in 2026, supported by scope for fiscal expansion and a relatively muted direct tariff impact. Rising oil and grain prices may provide a net positive impulse, but higher global inflation, elevated interest rates, and supply chain disruption remain significant headwinds. The ongoing conflict in the Middle East adds a further layer of uncertainty to global supply chains; however, for Canada, the net impact may be limited or even modestly positive, as disruption to global energy and commodity flows tends to support prices for Canadian oil and gas, forestry, and paper exports.

The Credit Benchmark 2026 default outlook projects deterioration across all G7 economies, but Canadian Corporates are expected to be the best relative performers. The following analysis explores this dynamic in detail – examining sector, province, and credit-quality dimensions – to identify where risks are concentrating and where resilience is emerging.

Canada Credit Risk Outlook 2026: Key Findings

The analysis identifies several key themes across sectors and provinces:

- The rising default risk trend is easing, but Corporates and Mining have shown the largest deterioration over the past two years, while Financials and Real Estate have been less affected.

- At the provincial level, Saskatchewan has deteriorated the most; Alberta the least.

- High Yield has deteriorated significantly faster than Investment Grade, with British Columbia the most pronounced example of this divergence.

- Consumer sectors and Basic Materials account for the largest risk increases over the past 12 months.

- Tariff impacts are concentrated in Retail, Transport, and Chemicals, predominantly in Ontario.

- Manitoba has the highest proportion of ‘a’ category obligors, while Quebec has the highest proportion of ‘b’ category; other provinces broadly mirror the national profile.

- The Credit Risk Indicator is biased slightly towards downgrades overall, with greater volatility in Financials than Corporates.

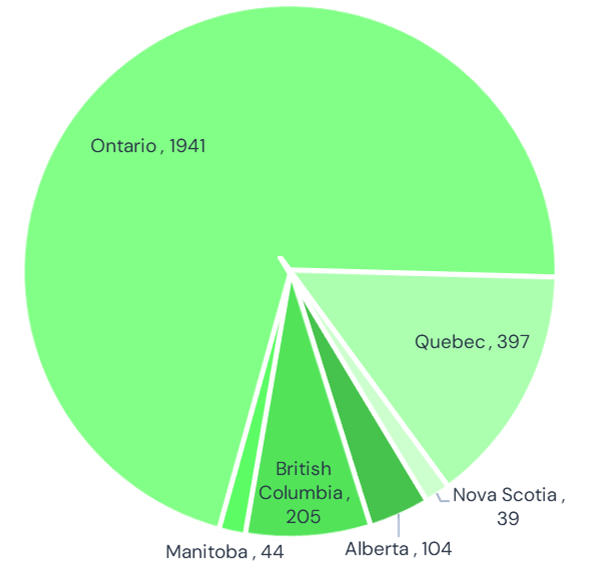

Canadian Credit Index: Provincial Composition

Corporates

Financials

- The proxy index covers a broad cross-section of Canadian obligors, though geographic concentration is notable.

- Coverage is higher for Corporates than Financials, reflecting a larger and more diverse obligor base.

- Ontario, Quebec, and British Columbia dominate the index in both segments.

*Includes obligors with default risk estimates from one contributing financial institution to maximise proxy index coverage. Single name consensus ratings are a subset of this since they require more than 1 bank estimate.

Provincial Credit Quality Distribution

- Consensus ratings reveal distinct provincial credit profiles, with meaningful variation in the distribution of credit quality.

- Most provinces have a credit profile broadly similar to the Canadian Corporate proxy index overall.

- Manitoba and Saskatchewan stand out for their high proportions of a-rated corporate obligors, though Saskatchewan also has the highest share of ‘c’ rated borrowers.

- Quebec and British Columbia have an above-average proportion of ‘b’ rated obligors.

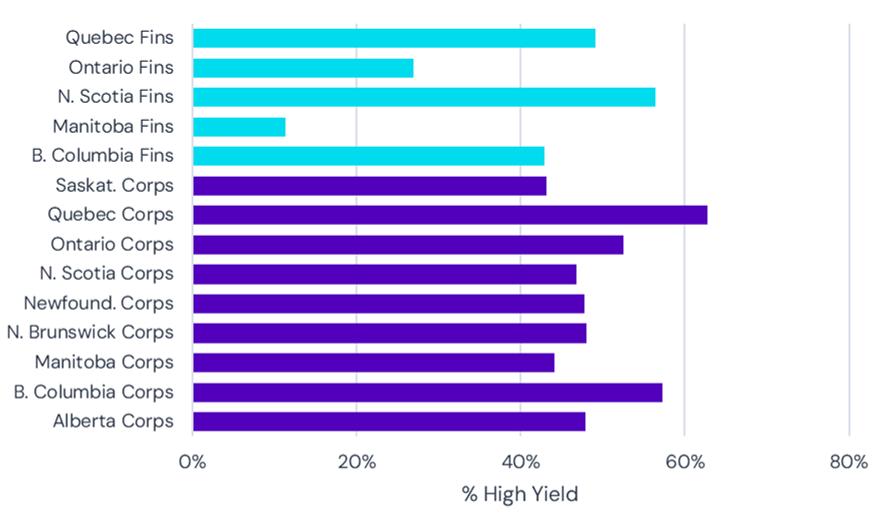

High Yield Exposure by Canadian Province

- High Yield exposure varies significantly across provinces, with notable divergence between Corporates and Financials.

- Financials generally have lower High Yield exposure, but Nova Scotia is a notable exception, with Financials HY exposure exceeding that of Corporates in several other provinces.

- Quebec and British Columbia have above-average High Yield exposure in both Corporates and Financials. Ontario is closer to the national average, particularly in Financials.

- Manitoba Financials have very low High Yield exposure, and the province ranks 2nd lowest for Corporates as well.

Largest Credit Deteriorations: 12-Month Movers

- The 25 obligors with the largest risk increase over the past 12 months reveal a clear tariff-driven pattern in both sector and geography.

- Ontario accounts for 9 of the top 25, consistent with its outsized exposure to trade-sensitive industries.

- Deterioration is concentrated in Consumer (including Retail), Industrial Engineering, and Transport.

- High Yield obligors account for 15 of the top 25, underscoring the disproportionate stress on lower-rated credits.

Credit Migration: Corporates vs Financials

- The Credit Risk Indicator (CRI) tracks net rating migration over time, providing a forward-looking measure of credit momentum that complements PD-based analysis.

- Unusually, Financials CRI has been more volatile than Corporates over the observed period, suggesting episodic rather than structural credit stress.

- The correlation between Corporates and Financials net downgrades is low, indicating that the drivers of credit migration in each segment are largely independent.

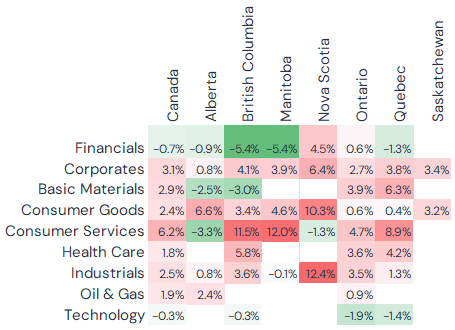

PD and Credit Migration: Provincial Scorecard

- Combining PD changes with cumulative CRI data provides a consistent picture of credit deterioration across provinces and credit quality segments.

- Default risk changes (PD) and cumulative net downgrades (CRI) are highly correlated over the past 12 months, reinforcing confidence in both signals.

- Financials have generally improved, except in Nova Scotia.

- Corporate HY has shown materially larger deterioration than IG in most provinces, except Manitoba.

- Alberta IG is the only Corporate segment to show improvement over this period, likely reflecting energy sector tailwinds.

- Nova Scotia stands out as the weakest province, with the largest deterioration across Corporate IG, HY, and Financials.

- British Columbia exhibits a major IG-to-HY divergence (2nd worst HY performer), yet is simultaneously the best Financials performer.

Correlation Between PD Change and Cumulative CRI - Past 12 Months

Canadian Default Risk Forecast: Tariff Impact

- Since April 2025, the tariff shock has driven a clear divergence between Corporates and Financials across provinces and sectors.

- Overall, Financials have improved by 0.7%, while Corporates have deteriorated by 3.1% – a gap that highlights the sector-specific nature of tariff exposure.

- Nova Scotia Financials are a notable exception, deteriorating by 4.5%.

- Corporates have deteriorated in every province, with Consumer industries the primary driver.

- Consumer Services shows particularly sharp deterioration in British Columbia, Manitoba, and Quebec.

- Technology showed slight improvement, and Basic Materials improved in Alberta and British Columbia, likely supported by commodity price strength.

- Nova Scotia Industrials are the single worst performer, deteriorating by 12.4%.

PD Trends: Corporates, Financials, Real Estate & Mining

- Tracking consensus probability of default (PD) trends over the past two years reveals a broad-based deterioration, though the pace appears to be easing across all segments.

- All major categories have deteriorated, with Corporates showing the largest increase in default risk.

- Mining follows a similar trajectory but with greater volatility, reflecting commodity price sensitivity.

- Financials have deteriorated the least, with Real Estate in the mid-range.

- All segments show signs of stabilising, with possible improvement ahead.

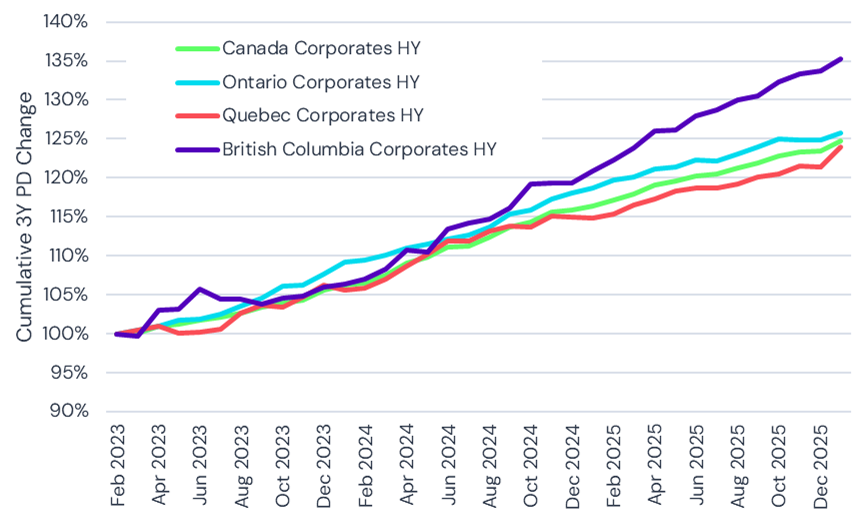

Canadian Provincial Credit Risk: Corporate PD Trends

- At the provincial level, corporate PD trends are tightly bunched among the major provinces, with British Columbia a clear outlier to the downside.

- Among the smaller provinces, Saskatchewan has deteriorated the most, followed by Manitoba and Nova Scotia. Alberta has held up relatively well, consistent with the energy sector tailwinds noted elsewhere in this report.

High Yield Corporate Risk: Provincial Divergence

- Focusing on the High Yield segment reveals the extent of credit stress among lower-rated corporates, where PD increases have been significantly more pronounced.

- Across the main provinces, High Yield Corporates have deteriorated by approximately 20% over the past two years, with trends that are very highly correlated.

- British Columbia is the clear outlier, with deterioration exceeding 35% – roughly double the national pace.

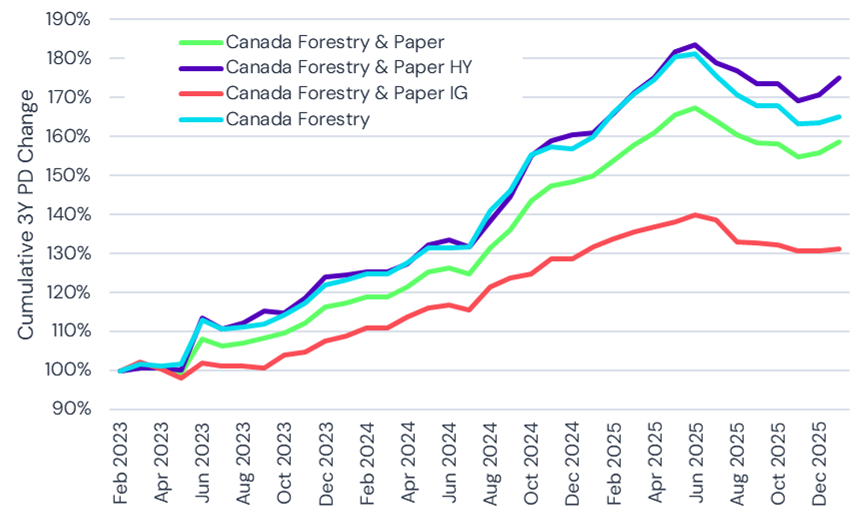

Canada Forestry: Early Tariff Pricing in Credit

- Forestry is a key sector for assessing tariff sensitivity, as US lumber tariffs predate the broader trade conflict and provide an early indicator of how trade barriers feed through to credit risk.

- All sub-sectors were already deteriorating before the main tariff announcement, with some partial recovery through to end 2025.

- Overall, Forestry has deteriorated by 65%, with Forestry & Paper slightly less affected at 60%.

- High Yield deterioration has been particularly severe, reaching nearly 80%, with less post-tariff recovery than the Investment Grade segment.

Canada Food Sector: Credit Risk Resilience

- The Food sector presents a more nuanced picture, with a relatively muted tariff impact and an unusual inversion between Investment Grade and High Yield trends.

- The overall tariff impact has been muted, with some improvement visible since April 2025.

- Unusually, Food Products IG has deteriorated the most at 25%, while Food Products HY has deteriorated the least at 16% and has shown the strongest post-April recovery.

- Food Producers show little IG-to-HY divergence, with both segments deteriorating by approximately 20%.

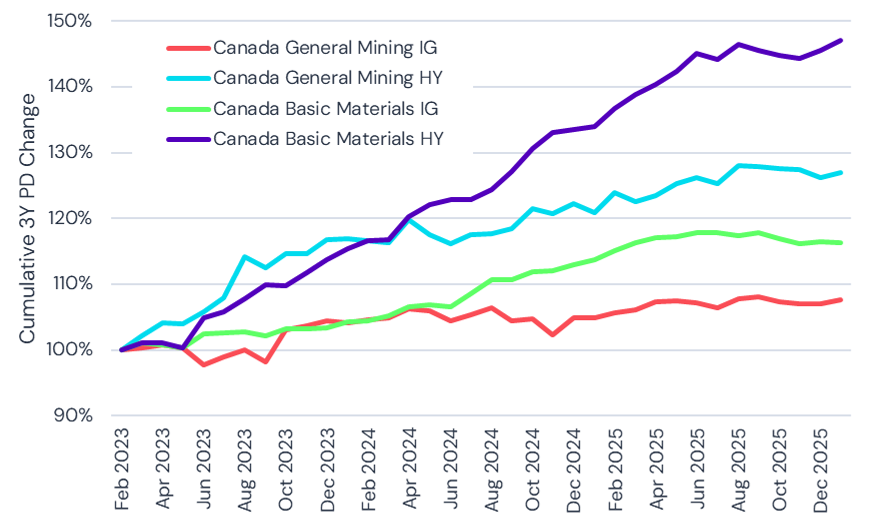

Mining & Basic Materials: IG–HY Risk Dispersion

- Basic Materials and Mining exhibit the widest dispersion in credit outcomes of any sector grouping, driven by stark differences between the Investment Grade and High Yield segments.

- The range is substantial: General Mining IG has deteriorated by less than 10%, while Basic Materials HY has deteriorated by close to 50%.

- Most sub-segments have been stabilising since mid-2025, with the notable exception of Basic Materials HY, which continues to deteriorate.

Consumer Credit Stress: Tariffs and No Recovery

- Consumer-facing sectors have been among the hardest hit, with limited signs of recovery since the tariff announcements.

- Consumer sectors have deteriorated by 20–30% over the past two years, with Consumer Goods performing worse than Consumer Services.

- Despite a relatively narrow range of outcomes, there has been no clear recovery after April 2025, unlike most other sectors examined in this report.

- Household and Home-related sub-sectors have been the worst hit, while Food & Beverage has been least affected and may be beginning to show early signs of improvement.

Canada Credit Risk by Province: Best & Worst Performers

- Ranking the best and worst performers by province over the past 12 months confirms the concentration of risk in trade-exposed sectors.

- Ontario dominates both the top and bottom of the distribution, reflecting both its size and its heavy exposure to manufacturing and trade-sensitive industries.

- Retail, Transport, Chemicals, and Industrials have been the worst hit across the board.

- High Yield obligors have suffered disproportionately relative to Investment Grade in the deteriorating sectors.

- On the positive side, Technology, Real Estate, Insurance, and Travel & Leisure have shown the most improvement.

Canada’s IG–HY Credit Fault Line

- The correlation matrix below maps the co-movement of PD trends across IG and HY segments by sector over the past 36 months.

- The Investment Grade block (upper left) shows the highest average correlation between sectors.

- The High Yield block (lower right) shows lower average correlations between sectors.

- Off-diagonal blocks show the lowest average correlations.

- A few sectors (Mining, Pharma) show high correlation between their IG and HY indices.

- For most sectors, the IG and HY segments show low or even negative correlation.

* Excel workbooks are available for correlation, volatility and portfolio analytics.

Credit Rating Migration: 2025 Transition Matrices

Corporates

Financials

- The 2025 transition matrices capture the migration patterns between consensus rating categories for Corporates and Financials, providing insight into the direction and magnitude of credit movement.

- Corporates show a high proportion of upgrades from c to b category.

- Corporates are slightly biased towards Fallen Angels*, while Financials migration is more balanced between upgrades and downgrades.

- Both obligor types are concentrated in single-category movements, with Financials showing more limited overall migration activity.

* Fallen Angels: migrations from Investment Grade to High Yield

Outlook and Next Steps

The consensus data paints a clear picture: Canadian credit risk is rising, but the pace of deterioration is easing and the outlook is more nuanced than headline figures suggest. Corporates – particularly in trade-exposed sectors such as Consumer, Retail, and Industrials – bear the brunt of tariff-driven stress, while Financials have been comparatively resilient. At the provincial level, Ontario’s dominance of both the best and worst performers reflects its outsized exposure to manufacturing and trade, while British Columbia’s sharp High Yield deterioration warrants close monitoring.

Looking ahead, the stabilisation visible across several segments suggests that the worst may be behind for many sectors – though pockets of risk remain, notably in Basic Materials HY and the broader Consumer space. Energy-linked provinces such as Alberta continue to benefit from commodity tailwinds, providing a counterbalance to the tariff headwinds felt elsewhere.

Credit Benchmark provides ongoing consensus credit data, analytics, and research covering Canadian and global obligors. For more detailed analysis, custom data extracts, or access to the underlying Excel workbooks for correlation, volatility, and portfolio analytics, please contact your Credit Benchmark representative or visit creditbenchmark.com.