For investors in Risk Sharing products, transparency is key. Credit Consensus Ratings speed up decision making, particularly where no public ratings exist and even when analysing undisclosed portfolios.

Complementing the information received from issuers, independent Credit Consensus Ratings put a bank’s credit data into context alongside that of their peers with real-world exposures. The data informs portfolio pricing, construction, substitutions and ongoing monitoring and alerting during the lifetime of a transaction. Consensus credit data covers large numbers of unrated names, adding extra clarity for disclosed and undisclosed portfolios.

This note uses Credit Consensus Ratings to compare a single bank’s view of a typical risk sharing portfolio with the broader bank peer group view of the same portfolios. It shows how this unique dataset can be used for industry trend tracking, portfolio analytics, and single name assessments.

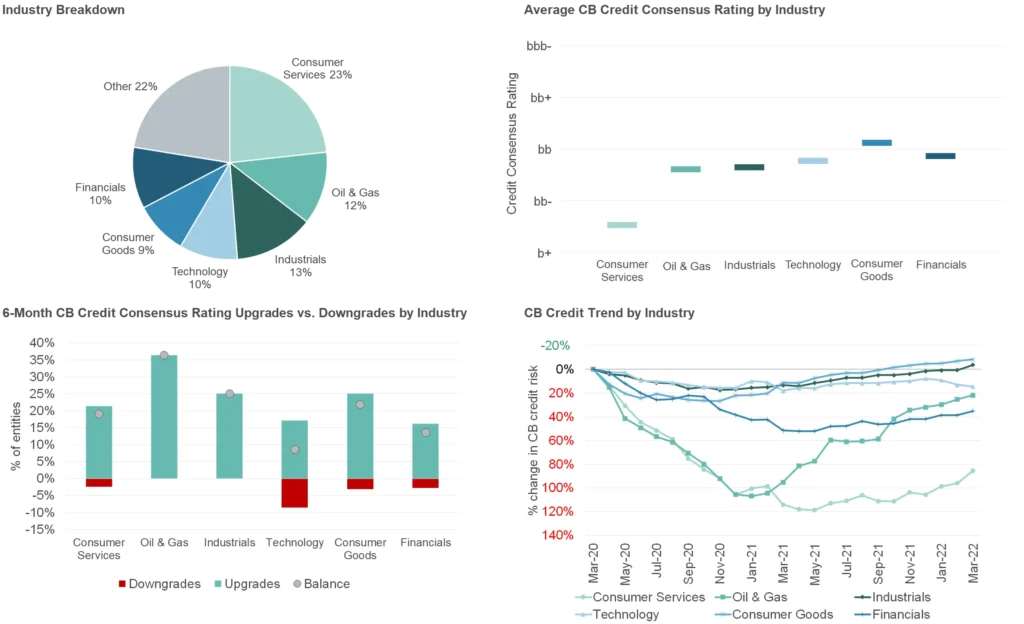

Figure 1 shows the industry and credit structure as well as credit trends for a disclosed risk sharing portfolio offered by Bank A. The first set of charts refer to the entire portfolio; the second set are for the Consumer Services portion. Similar analytics are possible for each industry.

Detailed consensus credit data is available on Bloomberg or via the CB Web App, covering many otherwise unrated companies. Contact Credit Benchmark to start a trial or to request a coverage check.

Figure 1: Disclosed Risk Sharing Portfolio – Structure and Credit Trend

Based on Bank A’s internal ratings, the majority (over 55%) of individual exposures are in the bb credit category. Across the peer group (excluding Bank A), the collective view is that only 35% of those same entities are in the same bb credit category.

Over the past two years, Bank A estimates that the credit quality of this portfolio has deteriorated by around 45% before recovering – about three times more than the rating deterioration for the same set of names estimated by the broader bank peer group.

Consumer Services is the largest single industrial category. Within Consumer Services, Bank A estimate that the proportion in bb is just under 50%, compared with an estimated 35% according to the bank peer group. And as with the overall portfolio, Bank A estimates that that this disclosed portfolio would have deteriorated by three times more than the average bank credit estimates for the same set of exposures.

Figure 2 compares Bank A credit risks and trends for the main industries.

Figure 2: Risk Sharing Portfolio Credit Trends for Main Industries, Bank A Estimates

Bank A estimates that Consumer Goods are the highest quality industry with an average credit risk (based on average default probability) corresponding to the bb category. Most of the other industries are just below this at the upper end of the bb- category, but Consumer Services is in the b+ category.

Over the past 6-months, 35% of the Oil & Gas names in this portfolio were upgraded and there were no downgrades. Consumer Services, Consumer Goods and Industrials all show upgrades in the 20% – 25% range, with minimal downgrades. Downgrades were more prevalent in Technology but still outweighed by upgrades.

Over the past two years, the Oil & Gas industry has shown the most striking turnaround in credit risk, which more than doubled in 2020 before a dramatic recovery in 2021 which has continued this year. Consumer Services saw a similar decline but a very limited recovery.

This illustrates how individual banks can use consensus credit data to:

- Compare their own portfolio risk estimates with those of their peer group, on a like-for-like name basis. This shows any biases or tendencies to over- or under-react to changes in the credit environment. This in turn can inform pricing, so that Bank A can consciously adjust exposures to sectors where it believes the differences are justified, and make adjust models where the differences are unexpected.

- Use peer group data to identify pricing anomalies across high and low risk sectors, and track credit trends based on upgrades vs. downgrades and average PD time series to predict potential turning points.

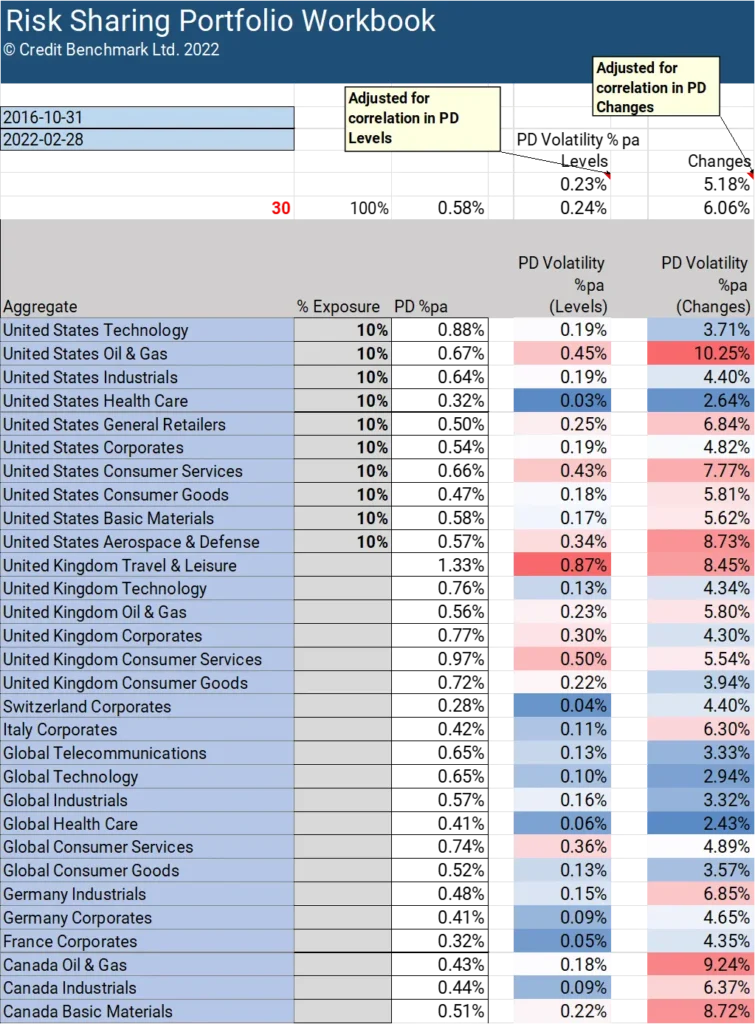

The same data and similar approaches can be used for undisclosed portfolios. Consensus credit data supports more than 800 aggregates across a range of geographies and sectors – including Corporates, Financials and Funds at the region, country, industry and sector level. These aggregates can be used to support a correlation-based approach to structured credit pricing and risk sharing.

Figure 3 shows a typical example.

Figure 3: Quantifying Credit Risk Diversification via Consensus Aggregates

Using the Credit Benchmark geography and industry schema, risk sharing investors and banks can compare portfolio pricing down to the sector and even sub-sector level of granularity without disclosing individual names.

Credit risk correlations between sectors can be estimated over the past 5+ years to set exposure limits and single name concentrations; the volatility of the overall portfolio with and without the impact of correlations can be calculated to show the diversification benefits of portfolio decisions.

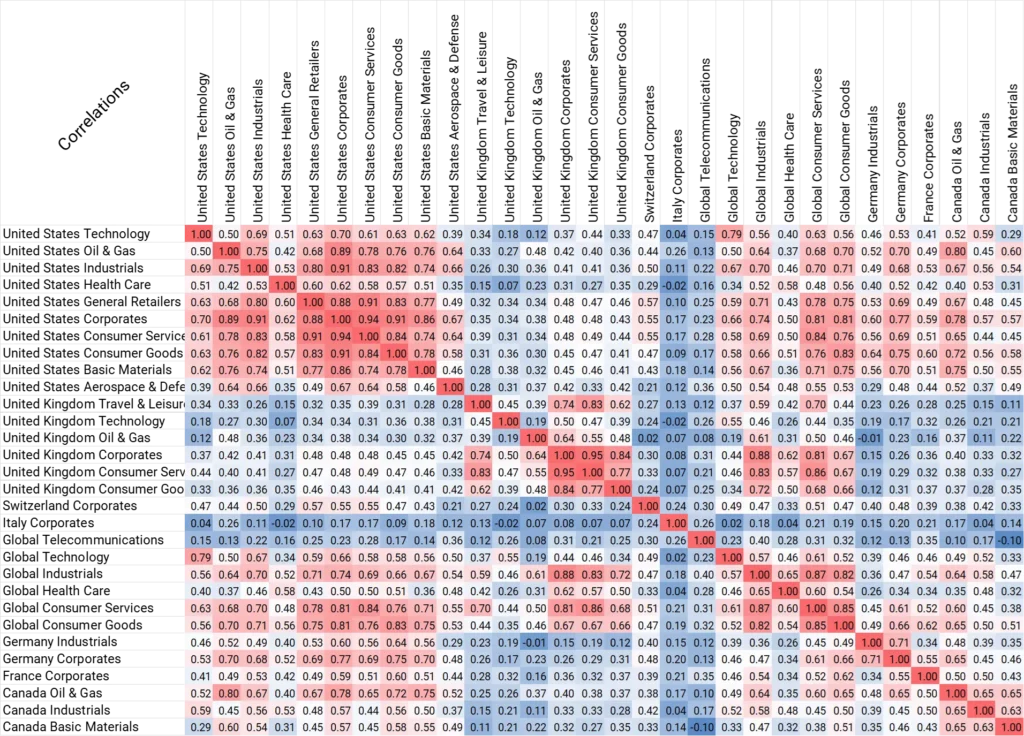

Figure 4 shows the correlations between changes in average PDs for these aggregates over the past few years.

Figure 4: Correlations Between Selected Aggregates, Based on Changes in Average PDs

This shows, for example that monthly changes in PDs are very highly correlated (+0.91) across US Corporates and US Industrials; while Italian Corporates show low correlations with all other aggregates in this set.