Argentina emerged from default last year and its economic indicators are beginning to improve. The economy is still in recession but appears to be finding a base, and inflation, while high (estimated at 17%) is falling. The agriculture sector is now only 10% of GDP, but is growing; and Construction and Real Estate are booming in Buenos Aires with growing Chinese investment.

In addition to attracting overseas investment, there has also been a wave of cash repatriation. It is estimated that Argentinians hold about $400bn in offshore accounts, and the Government is taking steps, including a tax amnesty, to encourage that to return.

Since emerging from default, the country has seen $50bn of capital inflow (mainly new investment) and has a modest immediate funding requirement of $30bn this year. The Treasury recently issued $7bn in US Dollar bonds and are issuing $0.7bn in inflation-linked Peso bonds this week. Argentina is likely to re-enter the JP Morgan Chase Emerging Market Bond index next month, and could also return to the MSCI Emerging-Market Equity Index later this year.

President Macri is benefiting from the divisions within the opposition PJ party. He is promising “reform without austerity” while grappling with the huge state sector (one-third of the workforce are Government employees). But aside from the rhetoric, deficit reduction will involve job losses and pension cuts; many Argentinians who lived through the 1990s will have a sense of déjà vu. But for now, the voters seem to be giving Macri the benefit of the doubt.

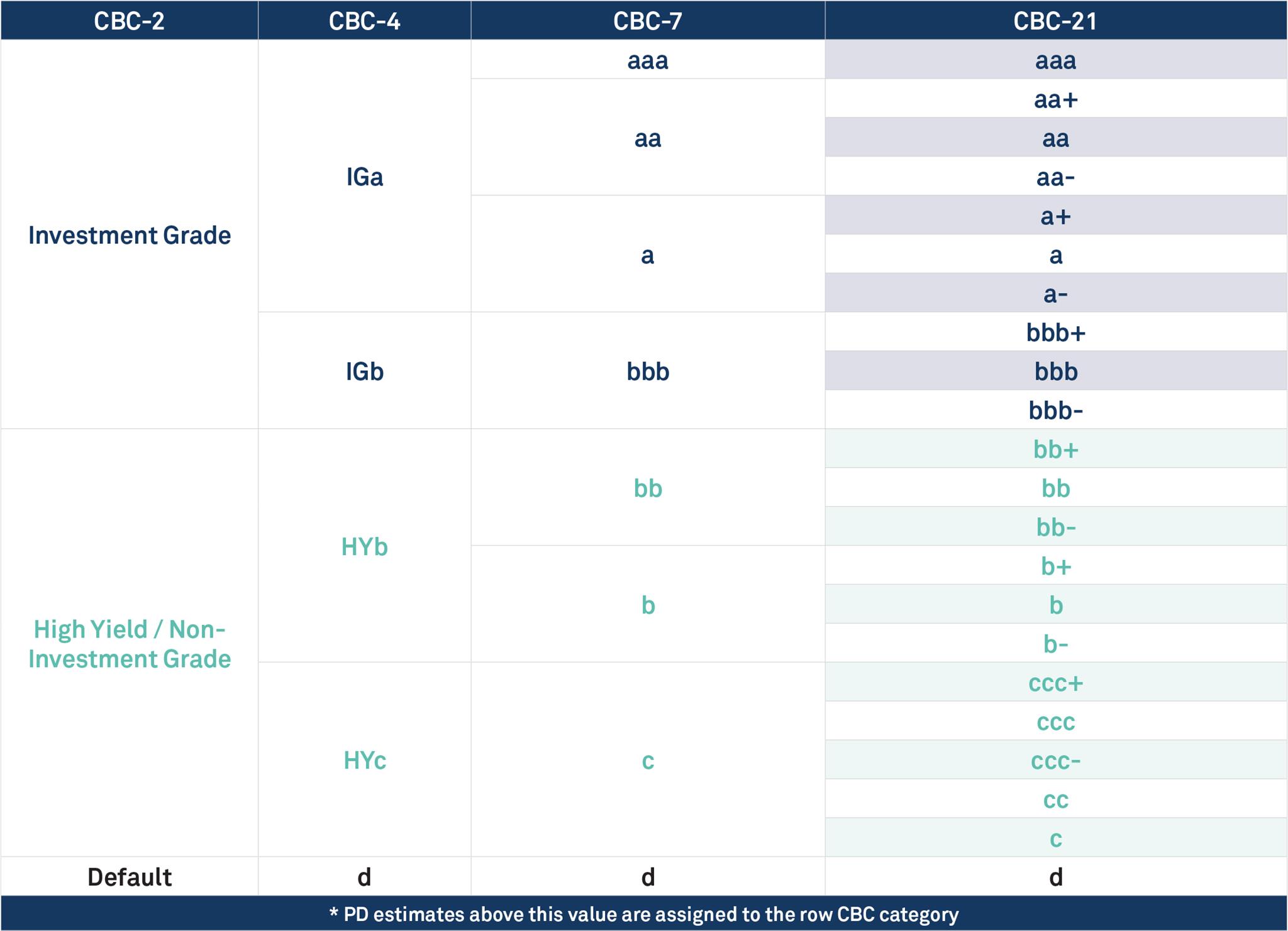

As the chart below shows, banks are optimistic. Since coming out of default, the CBC* for Argentina has been steady, but credit risk has been steadily dropping within that category. It is now very close to a full notch improvement. Two of the main rating agencies have assigned it the equivalent of B- with a stable outlook and the other is already at B, with a stable outlook.

If Macri can continue to convince foreign investors that the reform programme is serious and that he can bring the electorate with him, then further credit improvements are possible this year.

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of bbb+ is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

{kind=link}

Disclaimer: Credit Benchmark does not solicit any action based upon this report, which is not to be construed as an invitation to buy or sell any security or financial instrument. This report is not intended to provide personal investment advice and it does not take into account the investment objectives, financial situation and the particular needs of a particular person who may read this report.