Download the full report below.

“…may be the biggest disruption to real estate since the invention of the elevator.”

Rob Speyer, CEO of Tishman Speyer, Wall St. Journal, September 2019, talking about Co-working.

Co-working fills an obvious but challenging gap in the office property market – offering maximum flexibility to tenants by removing the duration risk of fixed term / fixed space leases. From its inception in 2005, exponential sector growth was driven by an increasingly buoyant office property market and a steady stream of start-ups that ensured minimal voids.

With a vaccine on the horizon, the global pandemic may become a non-issue; but has there been a permanent downshift in demand for city center office space? And if so, can the co-working model survive?

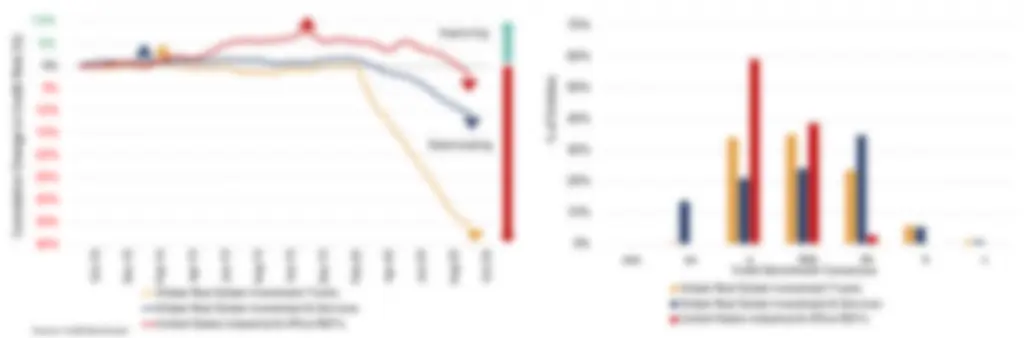

The sector was showing signs of saturation even before COVID, when heavily indebted WeWork pulled its planned $47bn IPO in September 2019, ending the year in the hands of Softbank with a more modest valuation of $5bn. CBRE noted a huge drop (75%) in flexible leasing demand in Q4 2019, mainly due to WeWork slamming on the brakes.

Consensus data shows a 30% – 40% increase in default probability over the past 6-8 months for companies with significant co-working exposure. This corresponds to single notch declines in credit quality on the traditional 21-category scale. For example, CRAs have downgraded WeWork – one of the few co-working firms assessed by agencies – from lower B to a range of CCC ratings; the credit consensus has followed a similar trend [please continue below to access full report].