To download the May 2020 Retail Aggregate PDF, click here.

Default Risk for US Retailers Up 6% in Last Month

- The probability of default for US retailers has increased 6% in the last month.

- Credit Benchmark Consensus (CBC) for US retailers has declined over last year from bbb- to its current position of bb+.

- Approximately 91% of firms in UK aggregate and 80% of firms in US aggregate have CBC of bbb or lower.

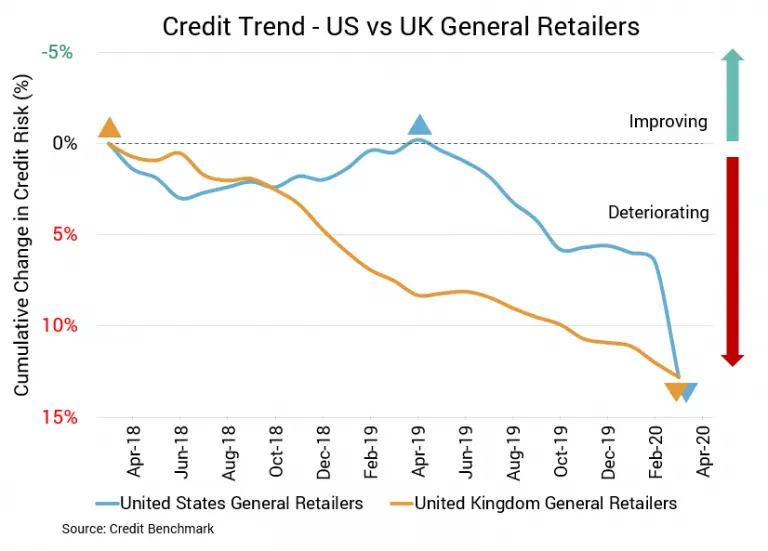

US General Retail Firms

Credit quality for US general retail firms has plummeted 6% over the last month and 12.3% across the past year. The average probability of default for the sector is now 52.2 basis points. The current CBC for this aggregate is bb+, down from bbb- at this time last year. With the most recent update, about 80% of firms in this aggregate have a CBC of bbb or lower.

UK General Retail Firms

Credit quality for UK general retail firms has also been deteriorating. The month-over-month decline was 0.8% and the year-over-year decline was 5%. Average probability of default is now 71 basis points, compared to 70.4 basis points the prior month and 67.6 basis points at the same point last year. The CBC for this aggregate has held in the bb+ range over the last year, but it is edging closer to a category downgrade if the average probability of default ticks higher than 78 basis points. With the most recent update, about 91% of firms in this aggregate have score of bbb or lower.

About Credit Benchmark Monthly Retail Aggregate

This monthly index reflects the aggregate credit risk for US and UK General Retailers. It illustrates the average probability of default for companies in the sector to achieve a comprehensive view of how sector risk will be impacted by trends in the retail industry. A rising probability of default indicates worsening credit risk; a decreasing probability of default indicates improving credit risk. The Credit Benchmark Consensus (CBC) Rating is a 21-category scale explicitly linked to probability of default estimates sourced from major financial institutions. The letter grades range from aaa to d.

Credit Benchmark brings together internal credit risk views from 40+ of the world’s leading financial institutions. The contributions are anonymized, aggregated, and published in the form of entity-level consensus ratings and aggregate analytics to provide an independent, real-world perspective of risk. Consensus ratings are available for 50,000+ financials, corporate, funds, and sovereign entities globally across emerging and developed markets, and 75% of the entities covered are otherwise unrated.