The FTSE100 has gained around 10% since the Brexit vote. This is driven in part by Sterling weakness, which has brought an immediate currency translation benefit to the numerous overseas earners in the index. Recent company results have highlighted volume winners such as Burberry, who have seen overseas buyers taking advantage of the weaker pound; and cost casualties such as easyJet, whose fuel bill has spiked.

The broader economic outlook for major UK companies is still unclear. Since the vote, UK economic data appears to be benign, with robust retail sales while inflation and unemployment remain subdued. But with the actual UK departure date at least two years away, the full economic impact of Brexit will take much more time to unfold. In the meantime, currency effects – positive and negative – will continue to work their way through the supply chain, while the UK corporate sector will have to live with an extended period of uncertainty.

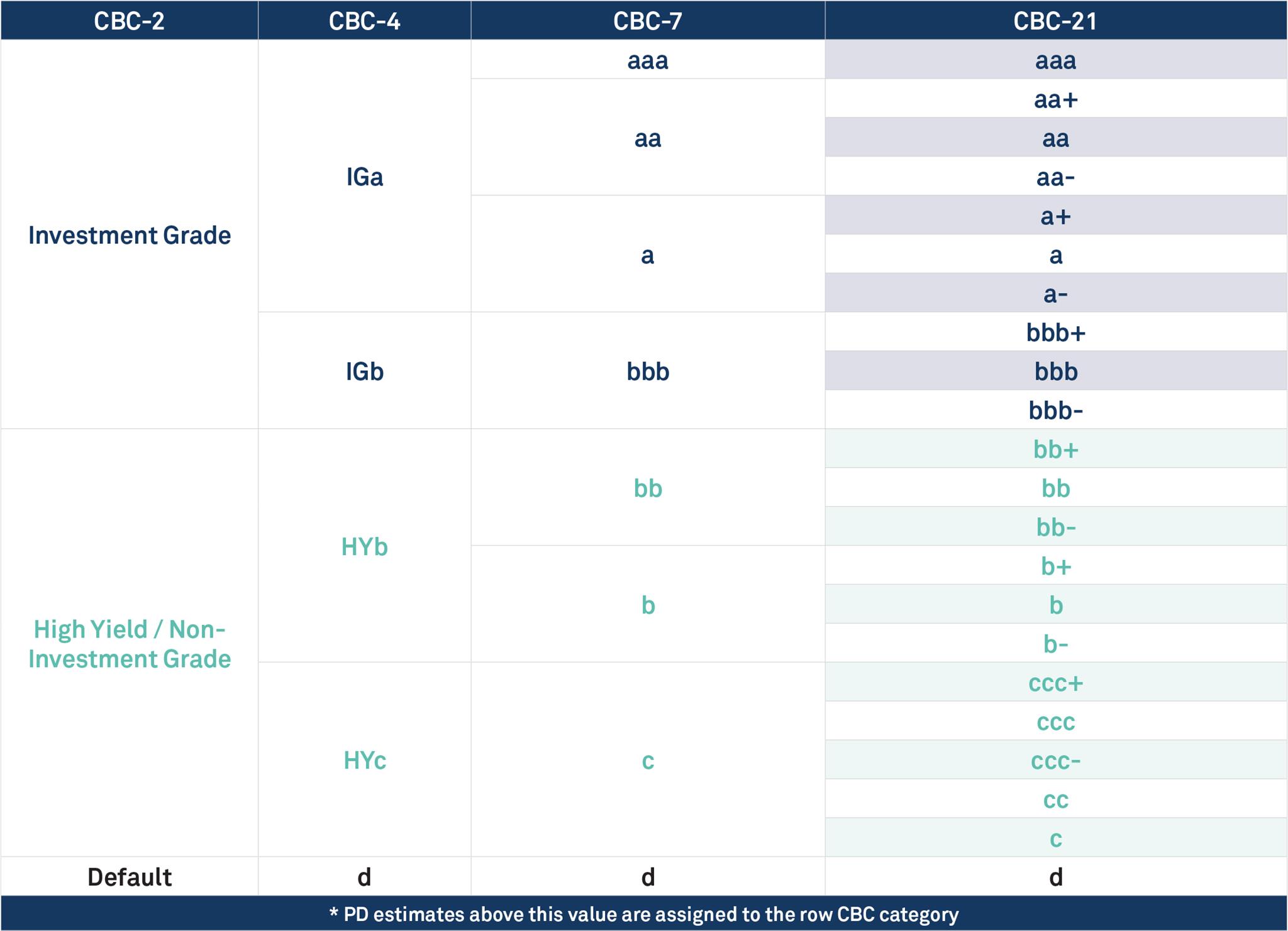

Credit Benchmark data shows that the average credit risk of 72 of the FTSE100 constituents has increased in the 6 months from April to September. The average CBC* for these companies was on the threshold of bbb/bbb-; it is now close to the middle of the bbb-range. This increase is significantly higher than the general trend in global corporate credit risk.

Measured by the consensus Probability of Default, the largest deterioration in credit risk has been in Basic Materials (+40%), Health Care (+39%), Industrials (+19%) and Consumer Goods (+19%).

This change is broad-based – seven of the ten industry groups show an increase in credit risk. Technology and Utilities are unchanged, with only Telecommunications showing a drop (-6%).

This suggests that the consensus view across major banks is that the default risk of the largest listed UK companies has increased since April. These same banks turned cautious on the UK Government in March, so it is likely that these moves mainly reflect Brexit-driven uncertainties. As negotiations proceed, this metric will provide regular updates on the likely winners and losers in the post-Brexit world.

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of bbb+ is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

{kind=link}