Sovereign credit ratings have been buoyed up for years by the belief that no matter how much governments actually borrowed, they were committed to coming close to balanced budgets as soon as was prudently possible. That commitment may now be wavering. The anti-deficit rhetoric never meant that governments abandoned their responsibility for cooling and warming the economy. Rather, politicians decided to let supposedly apolitical central banks do that work. This reliance on official interest rates was good for sovereign ratings. With the monetary authorities in control, governments were expected to borrow less.

Of course, reality did not always live up to the rhetoric, even in good times. Between 2000 and 2007 the average ratio of gross government debt to GDP for the G7 countries increased in five of the seven largest economies, according to International Monetary Fund calculations. The commitment to balancing budgets was completely suspended in response to the 2008 financial crisis. Tax revenues fell but spending cuts were at most moderate. Deficits exploded for two or three years. The goal was to keep up demand, so normal growth could resume and deficits could fade away. It hasn’t worked as planned. Growth in most developed economies has been too anaemic to keep government debt from expanding faster than GDP. The IMF expects the average ratio of gross government debt to GDP in the G7 countries to have increased by nine percentage points between 2011 and 2016.

Some politicians now seem to be changing their instinctively negative view of persistent large fiscal deficits. Waverers include both U.S. presidential candidates, the new government in the UK, the established government in Japan and some of the weaker members of the euro zone. There are several reasons to be tempted, starting with the hope that more government spending will reverse the recent pattern of disappointing GDP growth and job creation. There is also the possibility to improve dilapidated infrastructure at extraordinarily low borrowing costs. In addition, the risk looks low. With commodity prices down and wages under apparently permanent downward pressure, the supposed great danger of deficit spending – dangerously high inflation – hardly seems like a serious threat.

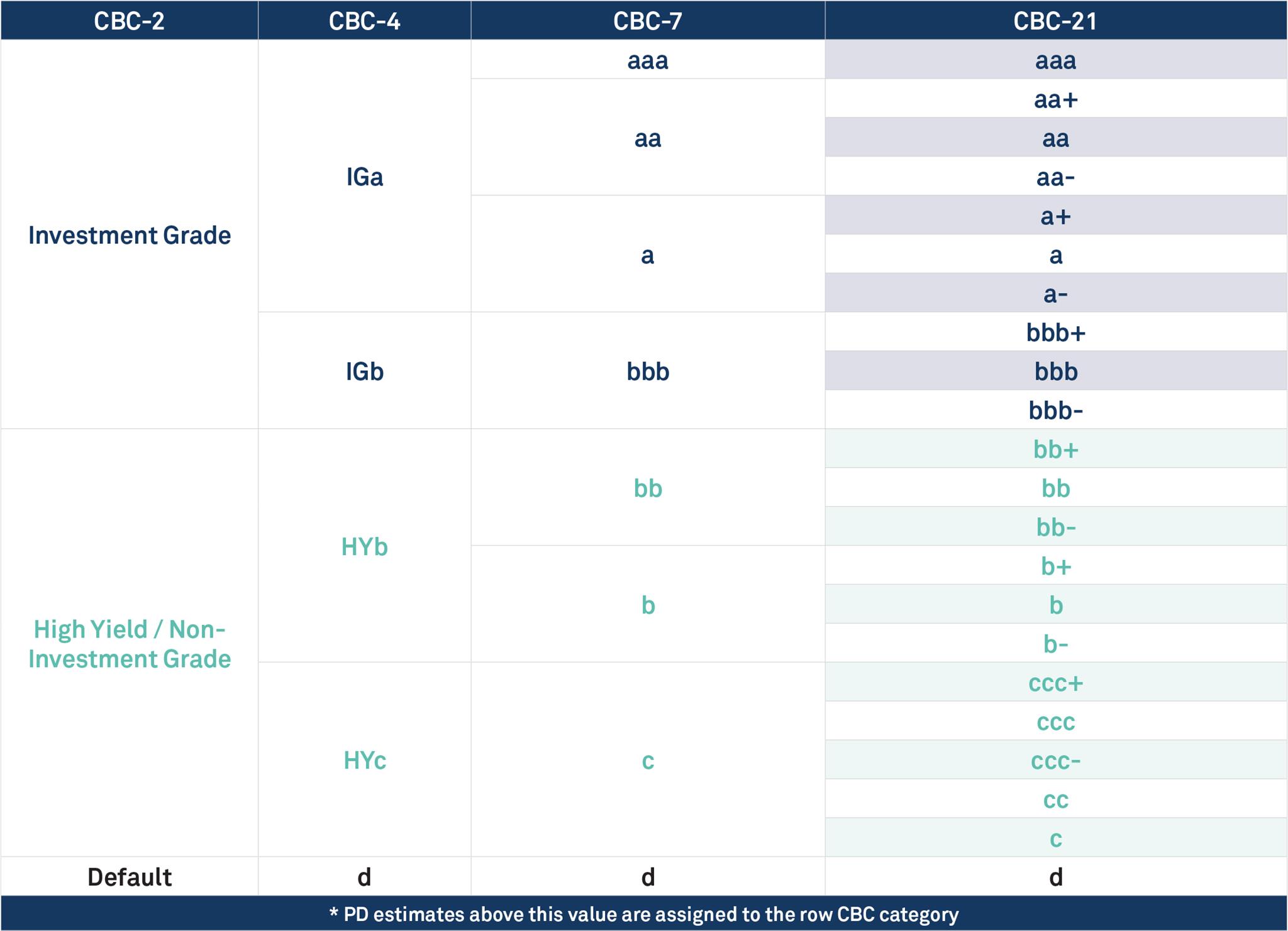

If aggressive deficit spending does come back into fashion, the credit community will have a problem. The CBC* for the G7 countries range from aaa to bbb. Those ratings look too high for entities which are determined to spend their way out of trouble. Ratings professionals will not be immune to politicians’ sober arguments for cheaply financed higher deficits, especially as there are many distinguished pro-deficit economists to provide intellectual support. And if it all works out, fine.

But there is a real risk that the extra spending will not end today’s near stagnation. No amount of stimulative spending may be able to overcome the continuing drags on developed economies – financial system weakness, slowing population growth and disinflationary pressures from poorer countries with cheap labour. Besides, no one can repeal a basic rule of credit: increasing debt goes with falling ratings.

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of [bbb+] is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

{kind=link}