We have just published credit data for September, with 11 contributor banks now providing crowd-sourced credit views CBCs* on more than 6,000 separate legal entities.

Sovereign coverage now includes Barbados, Jamaica, Panama and Albania. Other additions include the New York Metropolitan Museum of Art, Ralph Lauren, Kraft Heinz, and Netflix.

Over the month, 173 obligors improved their credit standing by at least one notch, but 285 deteriorated. 73 moved more than 1 notch. Compared with the previous month, the balance of transitions has shifted modestly from upgrades to downgrades: the August data showed that 215 improved, and 188 deteriorated, out of about 5,400 obligors.

Over the past two months, the combined totals show reduced credit risk for 318 obligors and increased credit risk for 378. The totals are close, but the overall bias is towards caution. This is in line with a more bearish stance on debt across the financial industry; for example, this week the Wall Street journal reported on large withdrawals from High Yield ETFs.

Probabilities of Default (PDs) increased in Technology, Utilities and Pharmaceuticals. They decreased in Consumer Services, Consumer Goods, Industrials and Funds.

A key metric that we are beginning to monitor is the rolling volatility of PD estimates over time, for each obligor. This gives early warning of changes in credit transition behaviour. If this metric is dropping, or below average, then PDs are less likely to change and transitions occur less frequently, with moves of more than one notch becoming less common.

Currently, the rolling volatility measures have been dropping across the majority of obligors. This suggests that transitions between credit categories are becoming less likely, which is consistent with the notch changes observed over the past month.

As this crowd-sourced time series grows, it is becoming possible to monitor this metric for different credit categories, countries and industries. We will be presenting more detail on this topic and its value for CECL and IFRS9 impairment calculations at the IACPM conference in Washington, D.C. this Friday, 4th November.

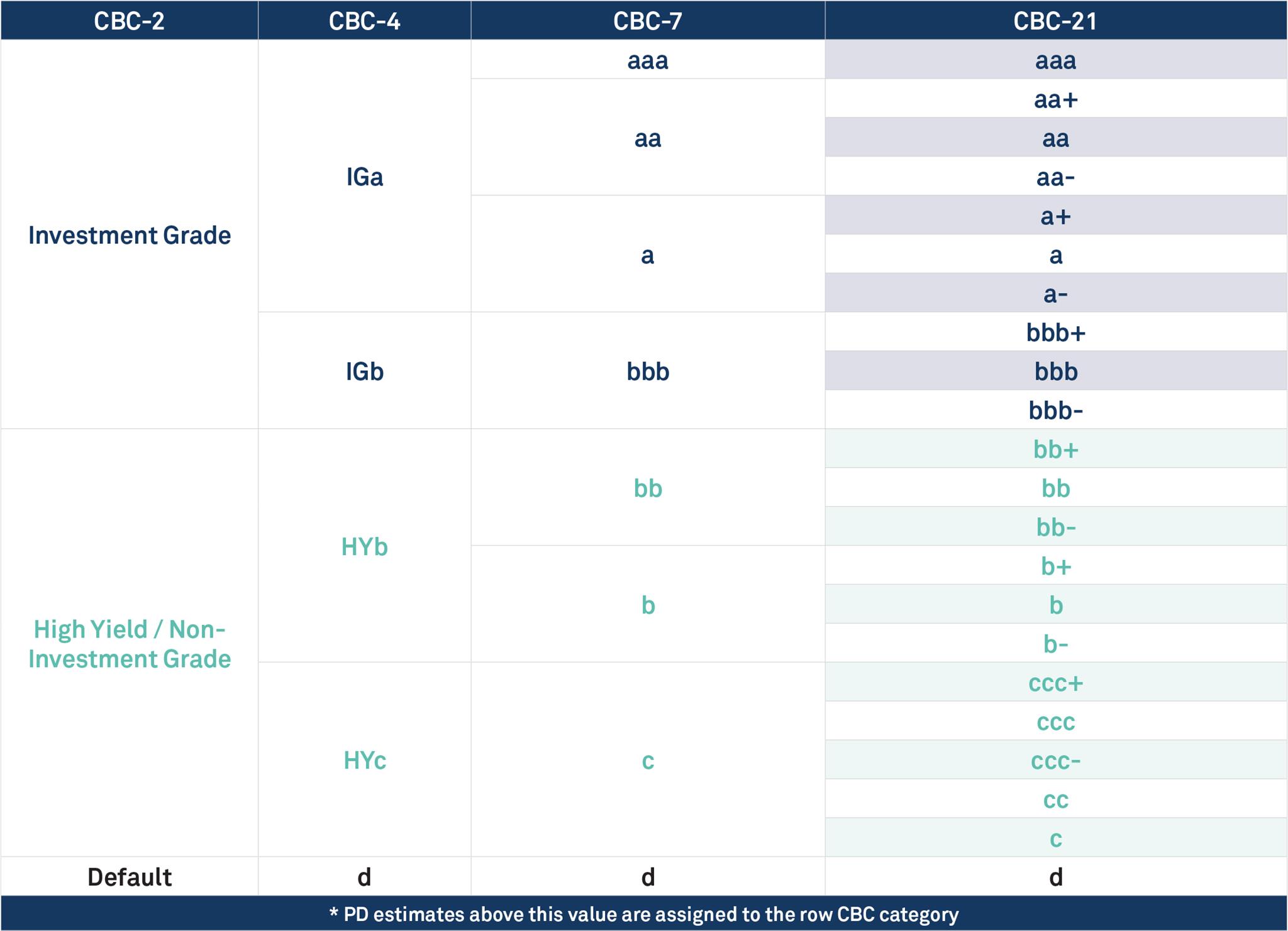

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of bbb+ is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

Image Source: IACPM Website.

{kind=link}