The European Central Bank intends to cut the pace of quantitative easing from €80bn to €60bn from this month. This has hit some of Europe’s peripheral bond markets: the spread of benchmark Italian government bonds yields versus Bunds rose above 2% this week, the highest in more than three years. The ECB now owns more than 10% of the €210bn outstanding Italian government debt.

However, the CBC* has improved over the past month.

The Italian political environment remains challenging and concerns about “Italexit” have been increasing, with the populist anti-EU Five Star Movement leading the opinion polls. However, elections are not due until 2018 and are more likely to result in a hung Parliament; for the moment a fragile coalition is in place after the failed “Reform” referendum in November led to Renzi’s resignation in December.

Negative views on Italian debt are understandable. Real GDP growth over the past 15 years is close to zero, and 2017 interest payments will consume 5.5% of GDP, the second highest in the Eurozone after Greece. However, the largest buyers of Italian government debt (other than the ECB) are domestic banks. UniCredit’s successful €13 billion rights issue in February has helped rebuild confidence in the financial sector with hope that the intractable problem of non-performing loans will be addressed.

Stronger growth indicators across Eurozone are also having a positive impact in Italy: the March IHSMarkit Purchasing Managers’ Index was a healthy 56.2, up from 55.4.

Since November 2016, bank-sourced views of Italian Sovereign credit risk have been increasingly positive. The CBC for Italy improved by a full notch last month. With the prospect of continued coalition governments as a hedge against “Italexit”, a stronger financial sector and an improving Eurozone growth outlook, Italy’s direct lenders seem to be taking an increasingly optimistic view.

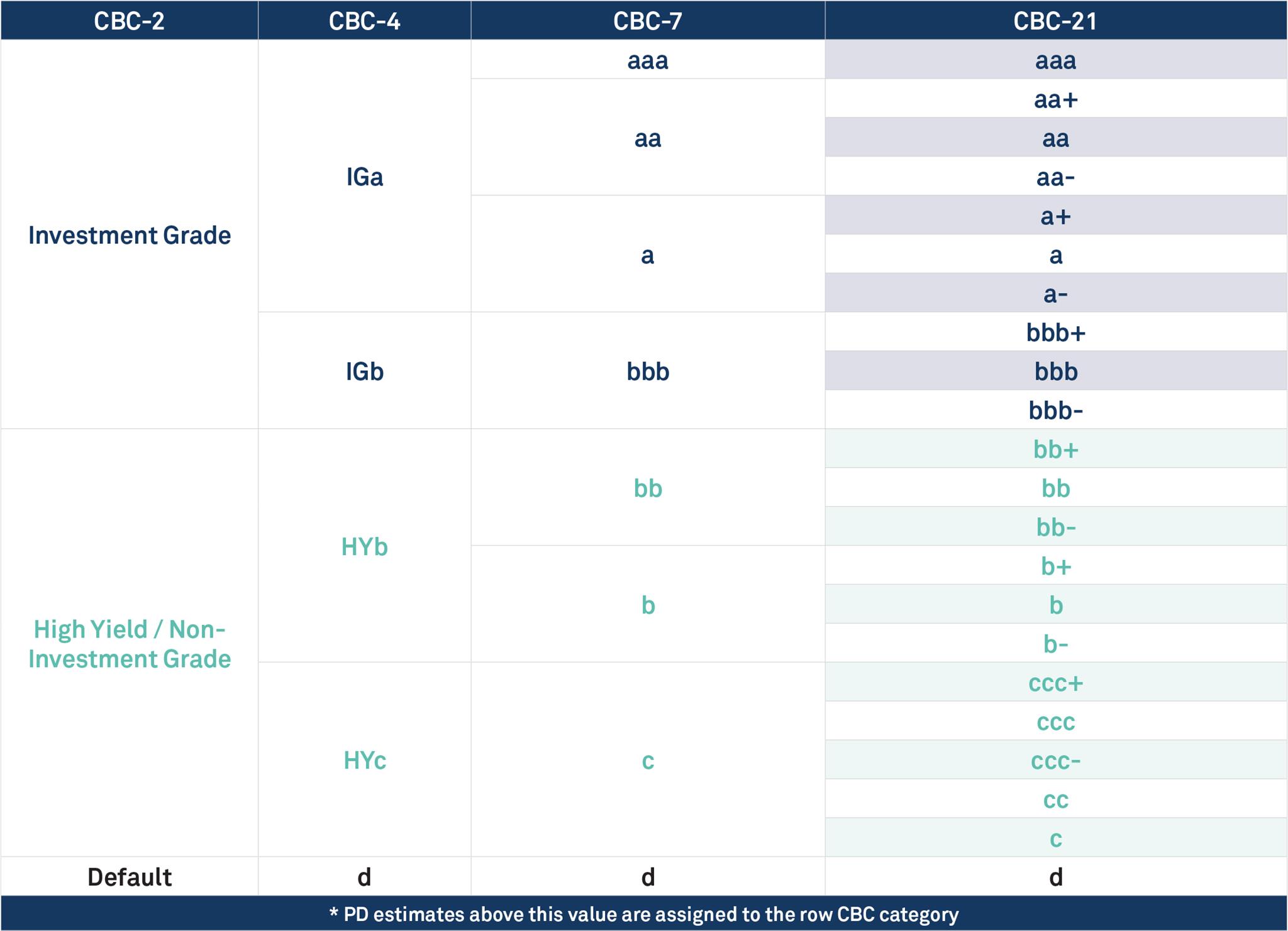

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of bbb+ is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

Disclaimer: Credit Benchmark does not solicit any action based upon this report, which is not to be construed as an invitation to buy or sell any security or financial instrument. This report is not intended to provide personal investment advice and it does not take into account the investment objectives, financial situation and the particular needs of a particular person who may read this report.

Image Source: ECB Website

{kind=link}